By Mark and Joe

Special to the Financial Independence Hub

The opportunity for Canadians to save and invest tax-free over decades could be considered one of the greatest wonders of our modern financial world. This begs an important question:

If you start early enough – Can you retire using just your TFSA?

We believe so and in today’s post we’ll show you how!

Can you retire using just your TFSA? Why the TFSA is a gift for all Canadians!

Our Canadian government introduced TFSAs in 2009 as a way to encourage people to save money. Looking back, it was one of the best incentives ever created for Canadian savers …

Our Canada Revenue Agency has a HUGE library of TFSA links and resources to check out but we’ll help you cut to the chase along answering that leading question above:

Can you retire using just your TFSA?

Why the TFSA is just so good

Since the TFSA was introduced, adult Canadians have had a tremendous opportunity to save and grow their wealth tax-free like never before. While the TFSA is similar to a Registered Retirement Savings Plan (RRSP) there are some notable differences.

As with an RRSP, the TFSA is intended to help Canadians save money and plan for future expenses. The contributions you make to your TFSA are with after-tax dollars and withdrawals are tax-free. You can carry forward any unused contributions from year to year. There is no lifetime contribution limit.

For savvy investors who open and use a self-directed TFSA for their investments, these investors can realize significant gains within this account. This means one of the best things about the TFSA is that there is no tax on investment income, including capital gains!

How good is that?!

Here is a summary of many great TFSA benefits:

- Capital gains and other investment income earned inside a TFSA are not taxed.

- Withdrawals from the account are tax-free.

- Neither income earned within a TFSA nor withdrawals from it affect eligibility for federal income-tested benefits and credits (such as Old Age Security (OAS)). This is very important!!

- Anything you withdraw from your TFSA can be re-contributed in the following year, in addition to that year’s contribution limit, although we don’t recommend that. More in a bit.

- While you cannot contribute directly as you could with an RRSP, you can give your spouse or common-law partner money to put into their TFSA.

- TFSA assets could be transferable to the TFSA of a spouse or common-law partner upon death. This makes the TFSA an outstanding estate management account – leaving TFSA assets “until the end” can be very tax-smart.

Since you paid tax on the money you put into your TFSA, you won’t have to pay anything when you take money out. This feature combined with the ability to compound money, tax-free, over decades, can make the TFSA one of the best ways to build wealth for retirement.

RRSP vs. TFSA – which one is better?

There is no shortage of blog posts that highlight this debate and one of our favourites is from My Own Advisor. You can check out his post here.

Without stealing too much of his thunder, the RRSP vs. TFSA debate essentially comes down to this: managing the RRSP-generated refund.

Let’s dive deeper with a quick example.

Contributions to the RRSP are excellent because the contribution you make today lowers your taxable income – and you may get a tax refund because of it – a pretty nice formula. The problem is, some Canadians might spend the RRSP-generated refund from their contribution. You’ll see why this is a major problem.

Consider working in the higher 40% tax bracket whereby RRSP contributions to lower your taxable income make great sense:

- If you put $300 per month into the RRSP for the year, that’s a nice $3,600 contribution.

- You’ll get a $1,440 refund (40% of $3,600).

When your $1,440 RRSP-generated refund comes in, and now you decide to spend it on a new iPhone, just know that your RRSP refund is effectively borrowed government money. Yup, a long-term loan from the government they are going to come back for. If you always spend your refund you are undermining the effectiveness of RRSPs because you are giving up your government loan that would otherwise be used for tax-deferred growth. A refund associated with your RRSP contribution should not be considered a financial windfall but the present value of future tax payment you must make.

If you typically spend the RRSP-generated refund in our example then we think some Canadians are FAR better off prioritizing your TFSA over your RRSP because of the known benefits of that present-day contribution.

TFSAs offer tax-free growth for any income earner

At some point, the money that comes out of your RRSP (or Registered Retirement Income Fund (RRIF)) will be taxed.

With TFSAs, the government has eliminated the guesswork about taxation. Because the TFSA is like the RRSP, but in reverse (you don’t get any tax break on the TFSA contribution), TFSA withdrawals are tax-free.

For far more details including answering dozens of questions about this account, read on about our comprehensive TFSA post below:

If you haven’t contributed much towards your retirement and/or you can’t possibly save enough with so many competing financial priorities – that’s OK – striving to max out your TFSA contributions each year, every year, is still very valuable and admirable goal. In fact, focusing diligently on just maxing out your TFSA (and ignoring the RRSP account entirely) will still serve your retirement plan well.

Regardless of your income, any Canadian who is 18 years of age or older with a valid social insurance number (SIN) can open a TFSA. All you need to do is reach out to a financial institution, credit union or insurance company that offers TFSAs and open an account.

Whether you set up your automatic savings plan to your TFSA weekly, monthly, or other – striving to make the maximum contributions to this account can be a significant wealth-building tool as part of the Four Keys to Investing Success.

Let’s use a case study to demonstrate just how good this account can be for you too – and why you can retire just using your TFSA!

Can you retire using just your TFSA – A Case Study

The big question in his article is – given enough time (ie. if you start young enough), can someone retire using only their TFSA? The answer may surprise you, at least it surprised us!

To help accurately model this scenario to account for government benefits, inflation, taxes, tax credits, and optimized withdrawal schedules, we dove into the software that we are using to manage our own early retirement plans.

Here are the assumptions we made:

- A young couple that recently finished post-secondary studies.

- Both 23 years old making $50k/year (increasing with inflation annually).

- Already have $6k each in their TFSAs which are 100% equities (returning 6.5%) that are maxed out every year (increasing with inflation).

- When they retire, the portfolio is adjusted to 60% equities and 40% fixed income (returning 4.9%).

- They qualify for average CPP and since they have lived in Canada their whole lives, maximum OAS.

- To maximize their CPP, they decide to take CPP at age 70 for the 42% boost.

- Since the housing market is out of reach, they decide to rent.

- 2% average annual inflation.

This young couple resembles a lot of young people freshly graduating from University. In this case, between scholarships and working part-time, they managed to stay debt-free and even managed to put a few dollars in their TFSA.

With no other savings besides maxing out their TFSAs every year (and investing wisely), is it possible to retire by age 60 or 65? Let’s take a look!

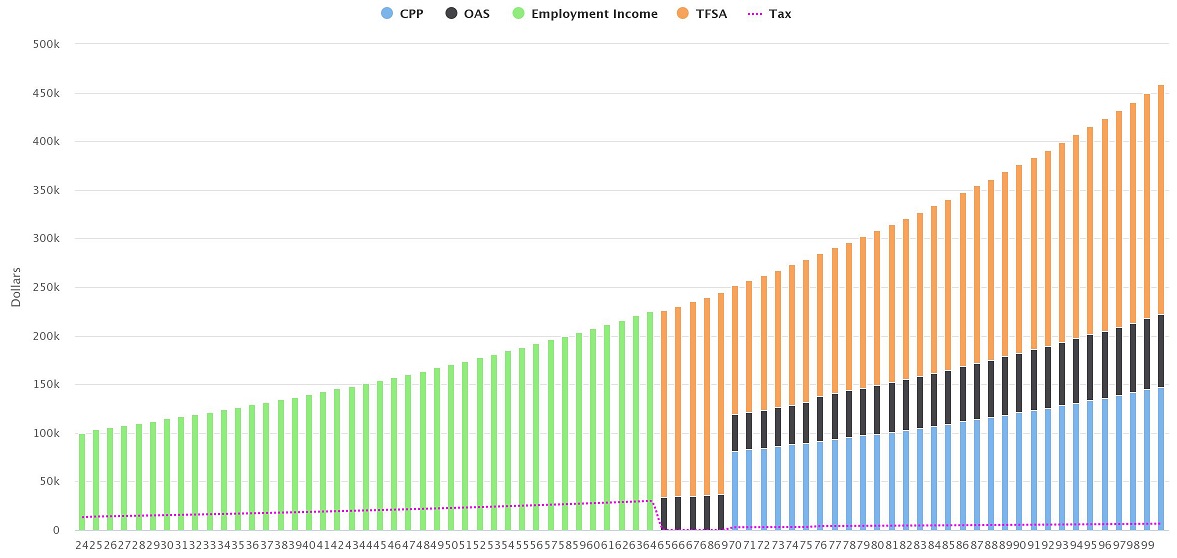

Let’s take a look at retirement at age 65 to give the couple as much time as possible to let that TFSA compound.

- How much do they need in retirement? Before we get into the retirement income, saving $12k/year in today’s dollars in their TFSAs means that they are living off about $67k/year after-tax. Assuming that they maintain this lifestyle, it means that a comfortable retirement would be in the same range.

- How much can they spend in retirement? At age 65, using our projections software, the most they can spend annually after-tax (in today’s dollars) throughout retirement is …. drum roll please …. $98k/year!

- How much are their TFSAs worth at age 65? A little over $3M (in future dollars assuming 2% inflation applies to TFSA contributions)! Even without inflation for any TFSA contributions, you have well over $2M!

What surprised us about this result is that not only is using solely their TFSAs enough to retire, they will have more money to spend in retirement than during their working years! Of course, that is providing that markets perform as assumed above.

Here are their income sources from age 24 to 100:

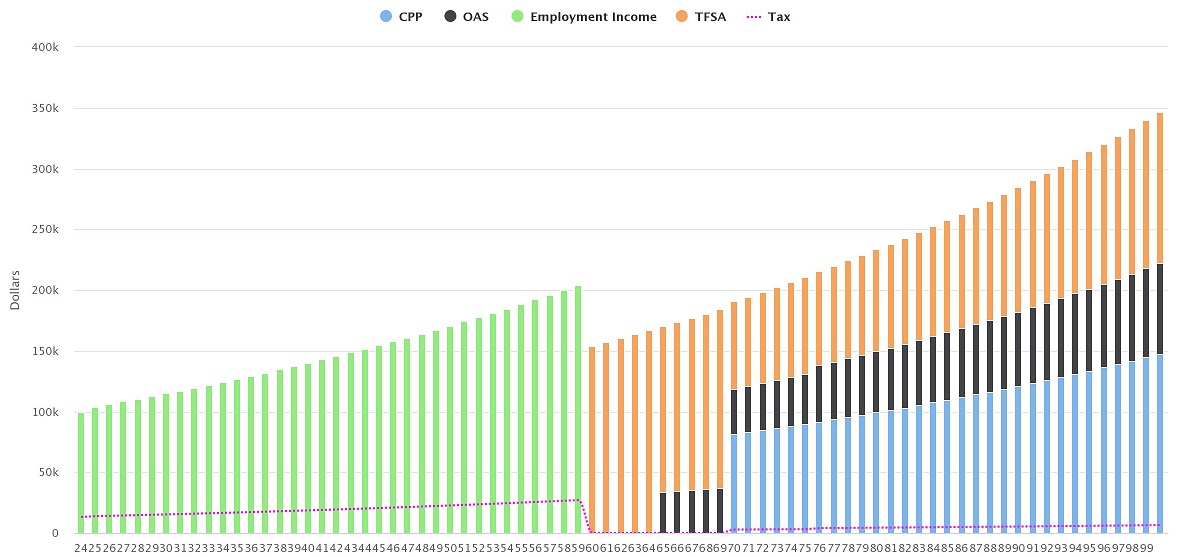

The next question is – if they have “too much money” retiring at age 65, can they retire a little earlier?

Yes, they sure can! Let’s back up retirement to age 60.

- How much can they spend in retirement if they retire at age 60? Again using our projections software, the most they can spend annually after-tax (in today’s dollars) throughout retirement is $74k/year after-tax! This is enough to fund their lifestyle and a small buffer!

Bonus – As TFSA withdrawals are not taxable (or income tested), between ages 65 and 70, this couple will be eligible for Guaranteed Income Supplement (GIS)! While GIS is not modelled here, you can read more about retirement on lower-income using GIS here.

Can you retire using just your TFSA summary

At Cashflows & Portfolios, we’re not suggesting to use the TFSA over the RRSP exclusively. I mean, both accounts have great merits so you use both if you can!

We have contributed to our RRSPs AND TFSAs for years, but as we get older, the TFSA definitely takes the priority and we believe it should for any income level.

Here is a great summary table of why for any income earner, TFSAs can help you build wealth for retirement too:

| TFSAs – Withdrawals are not considered taxable income. Income-tested benefits and income tax credits such as the GST Credit, Old Age Security (OAS) and the Guaranteed Income Supplement (GIS) aren’t affected by any TFSA withdrawals. Withdrawals don’t reduce these benefits. | RRSPs – Withdrawals are considered taxable income. RRSP withdrawals could reduce amounts you receive from income-tested benefits and income tax credits such as the GST Credit, OAS and GIS. RRSP withdrawals could reduce your post-retirement government benefits. |

As always take some time to look at your financial situation and try and figure out what works best for you. Ask us any questions along the way!

Remember, nobody cares more about your financial future than you.

Need any support with your retirement income projections?

Knowing how to save and invest wisely, to help you get the most out of your portfolio, is something we can help with. We’ve been there!

In addition to that asset accumulation work, if you need some help solving your retirement decumulation puzzle (i.e., how to efficiently withdraw from your retirement accounts), or figuring out if you have enough saved to spend for your retirement income plans, we’re here to help answer those questions and more as well!

If you are interested in obtaining private projections for your financial scenario, read more about our retirement projections service.

A reminder to those who have recently joined our readership and new fans of the site – our site is growing thanks to you!! As an example, a big thanks to Rob Carrick for mentioning our site and services in The Globe and Mail. From Rob:

“TODAY’S FINANCIAL TOOL

Cashflow$ & Portfolios is the name of a website built to help people learn how to reach their long-term financial goals with budget and long-term investing. Brought to you by a pair of veteran personal finance bloggers.”

Yup, that’s us! We appreciate every comment and email and every client interaction.

Stay tuned for more case studies and great articles over time.

Cashflows & Portfolios is a free resource providing a beginning-to-end guide for Do-It-Yourself investors. The journey begins with how to budget and generate cash flow; how best to invest that cash flow; onto using the nest egg to fund the next phase of life – retirement. The site is owned and managed by Mark and Joe, established personal finance bloggers in Canada. This blog first ran on Oct 28, 2021 and is republished with permission.