By Alyssa Furtado, RateHub.ca

By Alyssa Furtado, RateHub.ca

Special to the Financial Independence Hub

A whopping 86 per cent of Canadians say one of their top reasons when choosing a new credit card is earning rewards points or cash back, this according to a recent survey done by Ratehub.ca. 42% of those surveyed said they’ve never searched or compared credit cards to ensure they’re getting the maximum return.

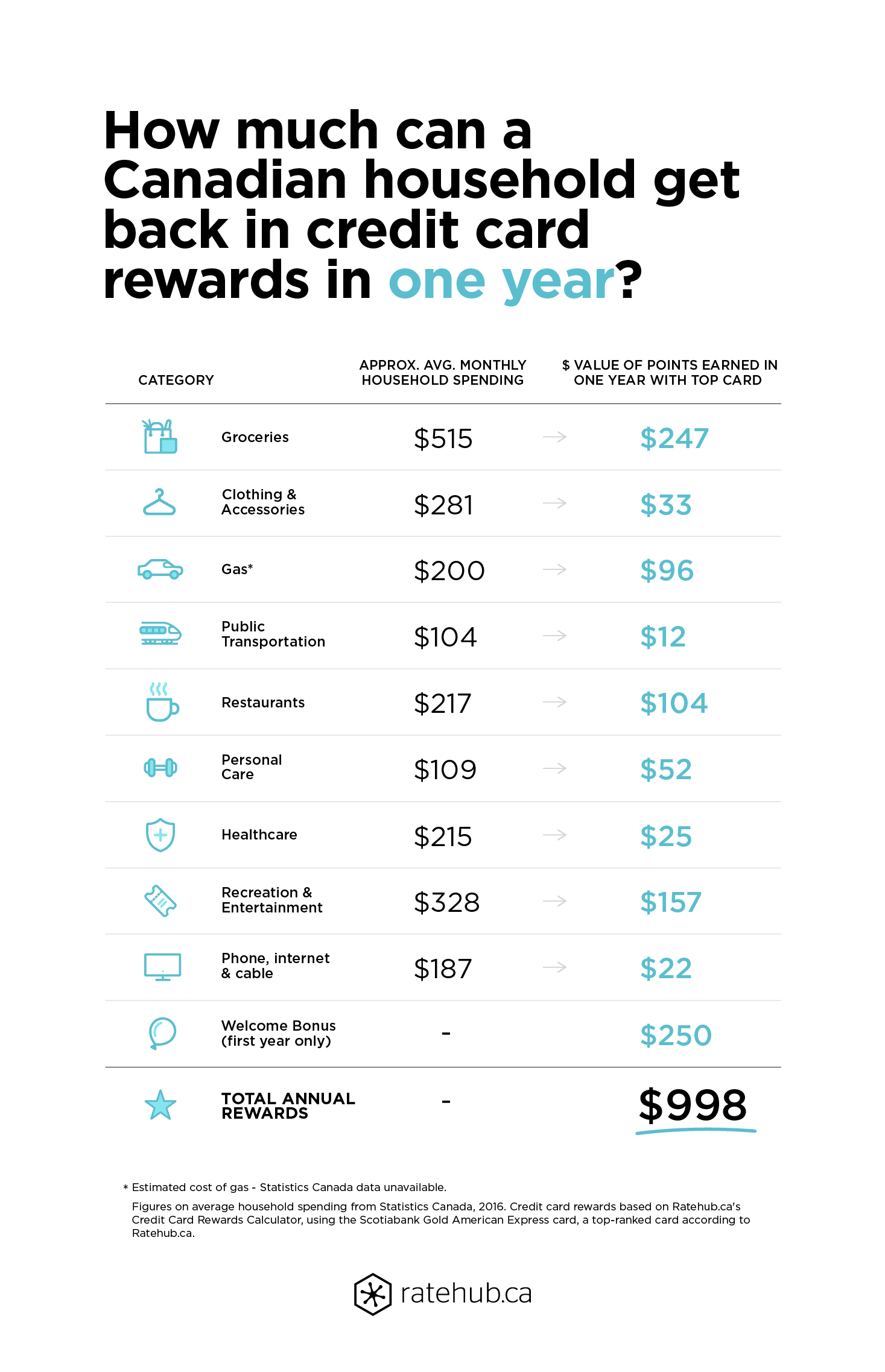

Based on spending averages from Statistics Canada, that means Canadians could be giving up almost $1,000 rewards by not using one of the best credit cards available.

How is that possible? Well, when you look at some of the best credit cards in Canada, they offer up to 5% in cash back or rewards for certain categories. In addition, many cards offer a big sign-up bonus that could be worth anywhere from $250 to $500, so it’s not hard to see how some people are missing out.

Choosing a new credit card

With 29 per cent of those surveyed saying that the card they use most has been in their wallet for more than 10 years and another 50 per cent saying they would never pay an annual fee, perhaps it’s psychology that’s holding them back from making a change?

Credit cards have changed dramatically over the years. With increased competition comes better product available to the public. Instead of sticking to the same card you’ve been using for years, it’s worth checking to see what’s available. Even if you hate annual fees, the bonuses and rewards you can earn will almost often offset that cost so it’s not actually costing you anything.

When picking a new card, you want to consider your shopping habits first. If you spend a lot on groceries and gas, then look for a card that has higher multipliers in those categories. There’s also no point in using a travel rewards credit card if you don’t like to travel. If that’s the case, a cash-back card is likely a better fit for you. Use a credit card comparison site such as Ratehub.ca to find out what the best credit card is for you based on your spending.

Don’t focus on the annual fee

It’s totally understandable that you don’t want to pay an annual fee for your credit card, but the benefits offered are usually worth much more. Although a sign up bonus only happens once, you get an average of about $250 in rewards for the higher-end cards, which is enough to cover two years’ worth of fees. In addition, many credit cards offer the first year free, so you can try out their card for a year at no cost to you.

Think about that $1,000 — or $998 to be specific — that you’re giving up every year. That’s enough to cover a flight to Europe or a lot of eating out. Of course, you could be practical with that savings and invest it in your RRSP or pay down your mortgage.

Don’t forget, most credit cards with an annual fee also come with additional benefits such as travel insurance, auto rental collision/loss damage insurance, extended warranty, and much more which is easily worth a few hundred dollars per year.

Final thought

Credit cards can be a useful tool, but only if you use them responsibly. It doesn’t matter how many rewards you’re earning if you’re not paying the full balance, on-time every month: the interest payments just aren’t worth it. That being said, you also don’t want to give up free rewards, so spend wisely.

Alyssa Furtado is a passionate entrepreneur, financial expert, digital marketer and educator, and founder of Ratehub.ca, a website that compares mortgage rates, credit cards, high-interest savings accounts, chequing accounts, and insurance with the goal to empower Canadians to search smarter and save money.

Alyssa Furtado is a passionate entrepreneur, financial expert, digital marketer and educator, and founder of Ratehub.ca, a website that compares mortgage rates, credit cards, high-interest savings accounts, chequing accounts, and insurance with the goal to empower Canadians to search smarter and save money.