Hub Blogs contains fresh contributions written by Financial Independence Hub staff or contributors that have not appeared elsewhere first, or have been modified or customized for the Hub by the original blogger. In contrast, Top Blogs shows links to the best external financial blogs around the world.

Dodge costly financial forecasting pitfalls that derail your Financial Independence plans. Canadian retirees need these proven strategies now.

By Dan Coconate

Special to Financial Independence Hub

Planning for Financial Independence requires careful financial forecasting, but many Canadians approaching or already in their golden years make costly errors that jeopardize their financial security.

Understanding common mistakes to avoid in long-term financial forecasts helps protect your hard-earned wealth and maintain the lifestyle you’ve worked decades to achieve.

Ignoring Inflation’s Compounding Impact

Many retirees don’t realize how much inflation can reduce their buying power over time. For example, with just a 2% annual inflation rate, $100,000 today will only be worth about $67,000 in 20 years. In Canada, this is even more concerning as healthcare and housing costs are rising faster than average inflation.

Quick Tips:

Factor 2-4% annual inflation into all projections

Account for healthcare inflation potentially outpacing general rates

Consider variable inflation rates across different expense categories

Overlooking Healthcare Cost Escalation

Provincial health coverage doesn’t eliminate all medical expenses. Dental work, prescription drugs, vision care, and long-term care facilities often involve major costs that many forecasts overlook. These expenses tend to increase with age, potentially leading to budget shortfalls just when you’re least able to return to work, making financial planning essential.

Underestimating Longevity Risk

Life expectancy in Canada continues to rise, with many individuals now living well into their 90s and beyond. This shows the importance of careful financial planning, especially since early retirement may not be sufficient if you live 30 or more years without employment income.

Women, in particular, face unique longevity challenges, often outliving their male partners and needing to manage finances independently for extended periods. Planning is essential to ensure financial stability throughout these longer retirement years.

Using Static Return Assumptions

Market volatility creates sequence-of-returns risk, where poor early performance devastates long-term outcomes despite average returns meeting projections.

A portfolio losing 20% in year one of Financial Independence faces dramatically different outcomes than one gaining 20% initially, even with identical long-term averages.

Managing Market Volatility

Consider dollar-cost averaging withdrawals and maintaining 2-3 years of expenses in conservative investments to weather market downturns without selling equities at depressed prices. Continue Reading…

Flexibility without stock-picking: Sector ETFs offer diversified access to industries like tech, health care, and energy, without the need to select individual companies.

Diversification and precision: Broad ETFs provide market-wide exposure, while sector ETFs let you overweight specific industries based on your market view.

Tactical or strategic: Use sector ETFs for short-term tactical calls or long-term structural tilts (e.g., overweighting defensive sectors for cash flow).

Image courtesy BMO ETFs

By Michelle Allen, BMO ETFs

(Sponsor Blog)

There are many strategies investors can use in their portfolios. One of the most popular strategies is making tactical tilts with sector ETFs.

Sector ETFs – like the new BMO SPDR Select Sector Index range – allow investors to focus on the parts of the market they believe will outperform, such as health care, financials, technology, or industrials.

These ETFs make it simple to increase exposure when certain sectors are expected to perform strongly or dial it back to buffer portfolios when economic conditions change, and are available in both unhedged1 and hedged-to-CAD2 versions.

In this article, we explore how sector behaviours shift across different economic environments, and how tactical tilts using sector ETFs can help investors pursue outperformance.

What is tactical investing?

Tactical investing refers to the process of adjusting portfolio allocations in response to market conditions or economic signals.

While a long-term investor might stick to a static asset allocation, tactical investors“tilt” or increase their exposure toward sectors or asset classes that they believe are poised to outperform over shorter time frames.

Sector ETFs are ideal tools for tactical investing. They allow investors to quickly and easily overweight specific sectors without the need to pick individual stocks. At the same time, they can also be used to create more balanced portfolios as they can be used to diversify portfolios that are concentrated in certain industries.

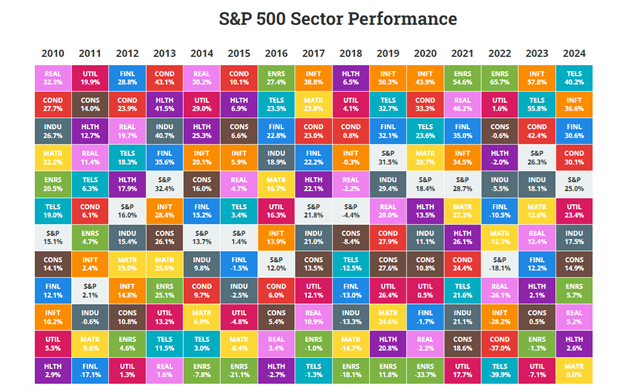

Sector performance can change dramatically each year

Sector performance often mirrors the dynamics seen across different asset classes and individual stocks: the top performers tend to change from year to year as shown in the table below3.

Over the past five years, we’ve seen sectors like information technology, consumer discretionary, and communication services lead the market in 2020 and 2021, only to become some of the worst performers in 2022. That year saw a massive rotation into energy, a sector that had significantly lagged in 2020.

Chart 1 – S&P 500 Sector Performance

Table 1 – S&P 500 Average Sector Returns

Source: Novel Investor (as at March 31, 2025)

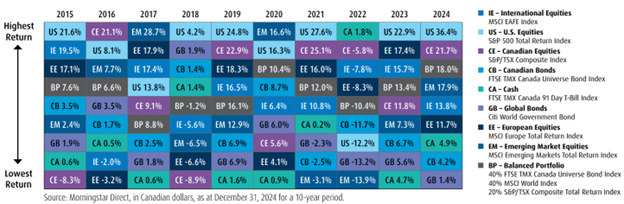

Chart 2 – Asset Class Returns

Index and sector returns do not reflect transactions costs or the deduction of other fees and expenses and it is not possible to invest directly in an Index. Past performance is not indicative of future results.

What drives these rotations? One of the key concepts is the economic cycle, which typically moves through four broad phases:

Recession: A period of economic contraction marked by falling gross domestic product and weak demand.

Recovery: Growth begins to rebound as consumer and business confidence, and spending, return.

Expansion: Economic activity strengthens, employment rises, and output reaches new highs.

Slowdown: Growth decelerates, signaling a potential shift back toward recession.

S&P 500 sector performance during phases

Understanding how sectors behave during different phases of the economic cycle is key to making informed tactical tilts. Here’s a snapshot of average S&P 500 sector performance across the four main stages of the U.S. business cycle (based on historical data from 1960-2019)4: Continue Reading…

John De Goey, a financial advisor and portfolio manager with Designed Securities, and long-time commentator on the financial services industry, was a keynote speaker at The Money Show recently held at the Metro Toronto Convention Centre.

Author of the book ‘Bullshift – How optimism bias threatens your finances’ (Dundurn Press, Toronto, 2023) and host of the popular podcast Make Better Wealth Decisions, De Goey delivered a presentation called Bullshift and Misguided Beliefs.

‘Bullshift,’ the term De Goey has coined, refers to his view about how the financial services industry makes people feel bullish in order to do the industry’s bidding. To make his point, he noted full-page ads appearing in such publications as The Globe and Mail; one of them ran under the headline ‘Be bullish.’

As for misguided beliefs, De Goey says there is ample evidence that Canadian mutual fund registrants believe things which are patently untrue. To illustrate the latter, he referred to Brandolini’s Law.

Alberto Brandolini was an Italian programmer who developed the term in 2013 and his rule goes like this: The amount of energy required to refute BS is an order of magnitude bigger than what was needed to produce it in the first place. Or, put another way, it compares the considerable effort needed to debunk misinformation to the relative ease in creating that misinformation.

American writer and humourist Mark Twain had a take on this at a much earlier time, and De Goey cited that. Said Twain: “It’s easier to fool people than to convince them that they have been fooled.” The point beyond all this, said De Goey, is that people must unlearn what they think they already know. No easy task.

His presentation at The Money Show covered a number of topics including:

The difference between misinformation (an honest mistake) and disinformation (saying something that is deliberately false), and how to unlearn the latter and think for yourself.

How behavioural economics and social psychology affect your investing decisions.

How the industry uses motivated reasoning and tribalism as opposed to critical thinking and evidence.

Why 90% of our financial decisions are based on emotions, not logical thinking.

Why governments and financial advisors like optimism over realism.

De Goey, always a student of history, observed that the market is 30% more expensive now than it was in 1929 just before the stock-market crash that led to the Great Depression. He mentioned the Smoot-Hawley tariffs of 1930 and their catastrophic impact on the U.S. economy, not to mention worldwide economy, and compared this to today’s on-and-off tariffs coming out of the Trump White House. He also noted recent credit downgrades and their effect on the U.S., and, of course, the very real pain of the tariffs which he believes will be much worse in the fourth quarter of 2025. What’s more, De Goey says this will be accompanied by higher inflation.

Bear market looming?

De Goey said the current bull market is “taking its final bow” and the bear market is “waiting in the wings.” In fact, he warned that gains made over the past six years could be entirely wiped out in the next four years if the historical regression to the mean for CAPE occurs. For those who are retired or nearing retirement, this would be devastating news indeed.

One of De Goey’s pet peeves – ‘optimism bias’ – refers to a) people thinking the good times will continue despite blatant warning signs, and b) the very human sentiment that bad things happen but only to other people. Not true, says De Goey. The trouble, he says, is that optimism can sometimes put you in trouble.

Normally, a presentation about money, economics and investing doesn’t get into wisdom imparted by such luminaries as Mark Twain, but De Goey didn’t stop there. He also took a page from Carl Sagan, notably, his 1997 book ‘The Demon-Haunted World. Said Sagan: “If we’ve been bamboozled long enough, we tend to reject any evidence of the bamboozle. We’re no longer interested in finding out the truth. The bamboozle has captured us. It’s simply too painful to acknowledge, even to ourselves, that we’ve been taken. Once you give a charlatan power over you, you almost never get it back.” Continue Reading…

Retirement income management and Required Minimum Distributions (RMDs) can be complex topics for many Americans. This article presents effective strategies to help readers navigate these financial challenges. Drawing on insights from financial experts, the following tips offer practical approaches to optimize retirement income and manage RMDs efficiently.

Purchase Annuity for Guaranteed Retirement Income

Leverage Qualified Charitable Distributions for RMDs

Optimize Asset Location for Tax-Efficient RMDs

Consider Annuities for Steady Retirement Income

Use Trusts to Manage RMDs Strategically

Convert to Roth During Market Downturns

Implement Bucket Approach with Beneficiary Designations

Start Home-Based Business to Offset RMDs

Purchase Annuity for Guaranteed Retirement Income

It is important to always consider broader planning needs, but one strategy that can be useful for generating retirement income and managing required minimum distributions (RMDs) is purchasing an annuity. This annuity would be purchased within an IRA and would create a level stream of guaranteed income for the rest of one’s retirement. This will not only satisfy one’s RMDs, but it can also lower taxes by stretching income across many years. In particular, it could help avoid large, irregular distributions that might push one into higher tax brackets. — Aaron Brask, Retirement planner, Aaron Brask Capital LLC

Leverage Qualified Charitable Distributions for RMDs

The obvious choice is to find a part-time job that aligns with your passion. This way, you can generate income and get paid to enjoy your favorite hobby. For example, if you love golfing, getting a part-time job at a golf course may give you discounts or even free games.

As far as managing RMDs, the amount that you must distribute is not determined by your income. It is based on the value of your Traditional IRA at the end of the year and the IRS Uniform Lifetime Table or Joint Life and Last Survivor Table.

This doesn’t include Roth IRAs. There are no RMDs in these accounts.

The best way to manage the increase in income, which can lower benefits such as Social Security or Medicare Part B (which are based on annual income), is to leverage Qualified Charitable Distributions (QCDs) for those who are philanthropic or give to a 501(c)(3) religious institution such as tithing.

When you reach the age to take RMDs, you can directly give to your favorite charity without incurring the tax implication or the increase in income that comes with RMD distributions. In 2025, you can donate up to US$108,000.

This will eliminate the RMD from being counted in your gross income and, at the same time, qualify for satisfying your annual distribution requirement.

I think this is useful because their favorite cause still receives donations, they satisfy their RMD, and they don’t have to pay the taxes up to that amount.

After 15+ years managing corporate finances and helping businesses with cash flow optimization, I’ve seen how asset location strategy can be a game-changer for Required Minimum Distribution (RMD) management. The approach involves strategically placing different types of investments across taxable, tax-deferred, and tax-free accounts to minimize the tax impact when RMDs hit.

I worked with a client in the software technology space who had accumulated significant wealth through stock options and 401(k) contributions. We repositioned his bond holdings and REITs into his traditional IRA while moving growth stocks to his Roth accounts. When his RMDs started, he was pulling from bond interest and dividend income rather than forcing the sale of appreciating assets.

The key insight from my Financial Planning and Analysis (FP&A) background is treating this like portfolio optimization: you’re maximizing after-tax income rather than pre-tax returns. His RMD tax bill dropped by 18% because we were distributing lower-growth, income-generating assets instead of his high-performing tech stocks.

This works especially well for anyone with diverse investment types across multiple account structures. The planning needs to start at least 5-7 years before RMDs begin, but the tax savings compound significantly over time. — Michael J. Spitz, Principal, SPITZ CPA

Consider Annuities for Steady Retirement Income

Although annuities are often a source of debate and critique, they are still a functional and conservative way to generate income in retirement. If set up early enough, the steady income can often account for Required Minimum Distributions (RMDs) across all Individual Retirement Account (IRA) assets since the withdrawal rates are higher than the often quoted 4-4.5%. — Pedro Silva, Financial Advisor, Apex Investment Group, LLC

Use Trusts to Manage RMDs Strategically

After 25 years of helping clients navigate estate planning and witnessing countless families deal with Required Minimum Distribution (RMD) challenges, I’ve discovered the most effective strategy: creating an offshore Asset Protection Trust that feeds into a domestic charitable remainder trust for your RMDs. While this may sound complex, it’s incredibly powerful for the right situation.

Here’s how it works: I had a client with US$2.3 million in retirement accounts who was facing substantial RMDs that would push him into the highest tax brackets. We transferred a portion of his Individual Retirement Account (IRA) into a charitable remainder trust, which allowed him to take his RMDs as annuity payments over 20 years at a much lower effective tax rate. The added benefit? The remainder goes to charity, providing him with immediate tax deductions that offset other income. Continue Reading…

If you plan to relocate in your golden years, consider these thoughtful upgrades to increase your home’s value before reselling your property.

Image courtesy of Adobe Stock/Lightfield Studios

By Dan Coconate

Special to Financial Independence Hub

For many homeowners, the approach of retirement brings a pivotal opportunity to unlock the substantial equity built up in their property over decades.

Selling your home can be a powerful strategic move, converting your largest asset into a significant financial windfall that can serve as the foundation for your retirement years. This capital can provide the Financial Independence needed to cover living expenses, pursue passions, and ensure peace of mind.

However, maximizing this return isn’t a passive process that begins with a phone call. The key to “fetching the max amount” lies in diligent preparation before you engage with real estate agents. Proactively investing in your property’s appeal can dramatically increase its market value and reduce its time on the market. This preparatory phase isn’t necessarily about undertaking massive, expensive renovations, but rather focusing on strategic improvements that offer the highest return on investment.

Consider improvements from a buyer’s perspective. Simple, cost-effective updates like applying a fresh coat of neutral paint, modernizing light fixtures, or updating cabinet hardware can transform a space from dated to desirable.

Enhancing curb appeal with fresh landscaping, a power-washed exterior, and a welcoming entryway creates a powerful first impression and is just one way to increase your home value before reselling. Furthermore, addressing the small but noticeable deferred maintenance — such as a leaky faucet, a sticky door, or cracked tile — demonstrates that the home has been well-cared-for. By tackling these tasks beforehand, you present agents with a polished, move-in-ready product, empowering them to suggest a higher, more competitive listing price from the outset and ultimately putting more money back in your wallet for the next chapter of your life.

Revamp your Curb Appeal

Tidying up the garden, repainting the front door, and adding outdoor lighting can make your property more inviting. Many buyers will see your home’s exterior first, so making this area clean and organized will leave a great impression. Trim bushes, plant flowers, and pressure wash the driveway for a polished look.

Refresh your Paint

A fresh coat of paint is a low-cost way to make your home look brighter and more modern. Stick to neutral tones like beige, white, or light gray to make rooms feel larger and allow potential buyers to imagine their own decor in the space. Also, consider adding accent walls in the bathroom and bedrooms.

Upgrade the Kitchen

Many homeowners will frequently use their kitchen, so make sure yours looks and operates its best. No need for a complete overhaul here; simple updates like replacing outdated cabinet hardware, adding a stylish backsplash, or upgrading old appliances can catch the attention of future buyers.

Modernize Bathrooms

Along with the kitchen, upgrading your bathrooms will make your home feel more modern to future buyers. Swapping out an old vanity, updating the showerhead, and installing new fixtures can improve the layout of your home and improve lingering issues with your plumbing systems. Consider upgrading the tile work or even adding a double sink for an added touch of luxury. Continue Reading…

By Dan Coconate

By Dan Coconate