Hub Blogs contains fresh contributions written by Financial Independence Hub staff or contributors that have not appeared elsewhere first, or have been modified or customized for the Hub by the original blogger. In contrast, Top Blogs shows links to the best external financial blogs around the world.

With economic uncertainty looming, taking control of your household finances is more important than ever. Preparing for potential downturns doesn’t mean drastic lifestyle changes: it means implementing smart, practical strategies that safeguard your financial well-being. By making a few savvy adjustments, you can create a solid buffer that shields your household from the effects of a recession while keeping your long-term financial goals on track.

Launch a Side Business

Starting a side business can be a powerful way to add extra income and recession-proof your finances. Whether you’re leveraging a hobby, tapping into a specialized skill set, or exploring new opportunities, a small business can provide a flexible, low-risk way to diversify your income. Consider ventures that align with your interests, such as freelancing, consulting, or offering home services, which tend to remain in demand even during tough times. By starting small and focusing on industries that offer consistent value, you can gradually build a side income that provides financial stability when it’s most needed.

Pay Down your Debt

Paying down debt is one of the most effective ways to strengthen your financial position ahead of a recession. High-interest debt, such as credit-card balances or personal loans, can quickly eat into your budget, making it harder to manage everyday expenses when the economy tightens. Focus on prioritizing payments to reduce or eliminate this kind of debt, starting with the highest interest rates. This not only frees up more of your income but also reduces financial stress. By becoming less reliant on borrowed money, you can better weather potential income fluctuations and maintain greater control over your finances.

Organize your Financial Records

Organizing your financial records can have many benefits, such as improved efficiency, better decision-making, and easier access to important information. Digitizing your documents can help you keep track of them more easily, save space, and add an extra layer of security to protect against theft or damage. After digitizing your records, try the process of splitting PDF content to break a document into smaller, more manageable files. Continue Reading…

The following is an edited transcript of an interview conducted by financial advisor Darren Coleman of the Two Way Traffic podcast with tax lawyer Anna Malazhavaya of Advotax Law.

It appeared on September 6th under the title ‘What you need to know about recent tax changes in Canada.’ Advotax is a team of lawyers and tax professionals that serves individuals, businesses and real property owners with tax planning and tax-dispute resolutions involving the Canada Revenue Agency. The discussion explored everything from the capital gains inclusion rate to expanded powers of the CRA to clients asking about moving to the US.

“It’s emotional but for some the increase in the capital gains inclusion rate was the last straw as they choose to leave Canada,” said Anna who added that over four million Canadians hold more than one property which means the government’s claim that this affects only 0.13% of the population isn’t true. “People are calling me every week. The wealthiest, the most talented entrepreneurs, are leaving Canada. It’s very sad to see.”

Anna and Darren talked about this phenomenon and how the June 25th deadline made it more expensive to leave the country with what can be a hefty departure tax. They also got into RRSPs, RIFs, and bare trusts which involve putting your property in someone else’s name. Anna said while the bare trust may have been designed to catch those who are less than scrupulous, it also captures honest people and gave examples.

I want your perspective and what your clients are thinking about the capital gains change we saw recently, and the deadline for people making changes. Now we’re in the new environment where the inclusion rate, or the amount of money you have to pay tax on, has gone up. And the government told us this was only going to affect 0.13% of taxpayers. Do you think their math was right?

Anna Malazhavaya

I have doubts. I’m not an economist and don’t have access to all the government stats, but I can share some stats. Capital gain may apply on the sale of your property that is not your principal residence. This includes your cottage, and your investment in rental properties.

4 million Canadians hold more than one property

Darren Coleman

More than four million Canadians hold more than one property. So four million Canadians, potentially, may be subject to that new increase capital gain rate. So that’s not 0.13%. That’s more.

Anna Malazhavaya

It’s way more. Of course, if I argued for the other side, I would say, Well, you don’t know how much money these people made on the property, and the first $250,000 of capital gain is still subject to the old rate, and that’s true. But at the same time, something tells me if these people held the property for more than 10 years that gain will be substantial. Look at how the real estate market performed in the last 20 years.

Darren Coleman

A lot of these people will be subject to the new rules. And not only that, think about people who only have one property, and let’s say, live on a farm property, and they have their house. When they sell their property, not the entire sale price will be sheltered by the principal residence exemption, but only the portion that’s required for the maintenance of their farm property. Everything in excess will be subject to capital gain and can potentially be subject to these new higher rates. Do you know how the government arrived at their number? A reasonable solution would have been to look at past taxpayer data and say, if we look at the last five or 10 years, how many taxpayers had a capital gain over $250,000? Let’s average it out over a bunch of years. But that’s not what they did. They looked at one year, 2022, and said only 0.13% of taxpayers had a capital gain of over $250,000. But that was also a negative year for stock markets globally, and a bit of a negative year for real estate equity markets everywhere. Tell me a little more about how your clients are experiencing this change.

Anna Malazhavaya

Until 2022 I probably had five people consulting me about leaving Canada. Normally, it was the other way around. We had all those talented people who wanted to bring their money, settle their life in Canada, educate their children here, build their future, build businesses, hire people. Pay taxes at 54% mind you. But this year alone, I have over a dozen new clients who plan to leave Canada and for my practice it’s a big change. People calling me practically every week, saying, I’m done. You know what? This capital gain game change. It did not affect me today. It probably won’t affect me tomorrow, but it’s the straw that broke the camel’s back.

More Canadians want to leave the country

Darren Coleman

The people who used to hire people, who used to come up with brilliant solutions, making everyone’s life better, they’re leaving Canada. Very sad to see and you’re not alone in experiencing that. I had a conversation this morning with a cross-border tax accountant and he said he’s had a surge of people looking to leave Canada, and he blames it on the tax policies which are making it less attractive for them to be here. Is it easy to just pack up and go to places like Florida?

Anna Malazhavaya

Leaving Canada became a lot more expensive. If you want to leave Canada, you are treated by Canadian law as if you sold all of your assets, even though you’re not selling anything. You keep all your assets. But the government says, Okay, fine, you want to leave Canada, but we want all the tax on the gain that you accrued to date. Some call it a departure tax, although this isn’t an official name, but it can hit you hard if you decide to leave Canada. So you have to declare all the gain you had from all your assets. Continue Reading…

Discover essential strategies and insights into succession planning to ensure a smooth transition and ongoing financial success for your small business.

Adobe Stock: Prostock-studio

By Dan Coconate

Special to Financial Independence Hub

As small business owners approach early retirement, ensuring the continued financial success of their business becomes a top priority. The journey of building a business is filled with hard work, passion, and dedication.

To ensure that successors are prepared to carry on the legacy and achieve ongoing financial success, delve into these essential strategies.

Succession Planning

Succession planning is a critical part of preparing for retirement. Identifying potential leaders within the team early on and providing them with opportunities to grow is key. This includes offering challenging projects, exposing them to various aspects of the business, and involving them in key decision-making processes. An effective succession plan ensures a smooth transition and continuity when the time comes for new leadership to take the reins.

Financial Literacy Training

Financial literacy is indispensable for any leader aiming to drive business success. Investing in comprehensive financial training programs that cover budgeting, financial analysis, risk management, and strategic financial planning is crucial. Developing a strong grasp of financial principles equips future leaders to make informed decisions that positively impact the business’s bottom line.

Executive Coaching

Executive coaching plays a significant role in developing leadership skills and ensuring alignment with business goals. There are several benefits to offering personalized executive coaching sessions, whether led by you or a third party. It’s an easy way to help potential leaders enhance their decision-making abilities, improve their emotional intelligence, and refine their leadership style. Continue Reading…

We recently conducted a “Value of Advice” survey of Canadian investors that reinforced to us how important financial advice really is. We found that while advisors enjoy high levels of client satisfaction and loyalty, younger investors are increasingly opting to manage their assets themselves through online discount brokerages and digital services.

Among Canadian investors, 44% feel their advisor provides high value, and 74% believe their financial advisor is worth every dollar they pay. Additionally, 71% say they plan to remain with their current advisor, with that figure rising to 80% among those aged 55 and over.

While these results were not surprising, the level of trust that financial advisors enjoy is changing with a cohort of younger investors. Among those aged 18-34, 40% use online platforms for investment management, while only 38% rely on financial advisors. By contrast, 70% of those over the age of 55 use a financial advisor, with only 17% turning to online platforms.

A Tale of 2 Investors

It’s clear that Canadian investors highly value financial advisors and the guidance they provide. However, there is a tale of two investors split by age in terms of the duration, method and frequency of financial advice they receive.

This presents both a challenge and opportunity for financial advisors to provide more holistic wealth management services and relationship-oriented advice to younger investors.

While younger investors are more inclined to go digital with investing, they also show a significant level of hesitation. Among younger investors, 35% report not fully trusting their financial advisor. When asked whether they can manage their own investments, many admitted to lacking the time (47%), knowledge (39%), or confidence (42%) to do so effectively.

The study highlighted that financial advisors remain the preferred source of advice for most Canadians, regardless of age. In fact, 89% of investors report that their go-to source for financial information and advice is their financial advisor or bank. Moreover, human advisors are perceived to deliver better investment returns, with 44% of respondents believing that human advisors generate higher returns, compared to only 9% who hold the same view of robo-advisors.

Almost half in regular touch with advisors feel optimistic about their financial future

The data revealed that frequent communication with clients is shown to make a significant difference in client satisfaction and optimism. Among those who communicate with their advisor monthly or more, 46% feel optimistic about their financial future, compared to just 18% of those who communicate only once a year. Additionally, 40% of those who have a financial plan created by an advisor express a high level of optimism about their financial future, compared to only 22% of those without a formal plan.

We have been looking at the impact of financial advice for more than 25 years and the utility and benefits are the same.

As the investment landscape evolves, financial advisors will need to focus on building trust, maintaining regular communication, and emphasizing the value they provide in an increasingly digital world. Doing so will enable them to serve both traditional and younger investors more effectively, today and in the future.

Mario Cianfarani is head of distribution for Vanguard Canada. Most recently, Mario was head of national accounts & institutional sales and was previously head of ETF capital markets. Before joining Vanguard in June 2015, he was a portfolio manager at First Asset Investment Management, responsible for domestic and global equity ETFs and sector-based, North American covered call ETFs. Mario has held senior sales and trading positions with a number of Canadian capital markets teams. His experience includes trading equity derivatives and marketing derivative-related risk management solutions to a broad range of clients.

Mario earned a BA in applied mathematics from York University and is a CFA® charterholder.

2023-2024 HireAHelper Moving Migration Report: Artwork by Esther Wu

By Volodymyr Kupriyanov

Special to Financial Independence Hub

When we released our last study of starting a moving labor company as a side hustle, it was a great time to get into the business. Home sales were at an all-time high, and the number of Americans who moved that year inched up for the first time in a decade.

However, after only one year, the housing market has cooled off. And even though sales of newly built homes are still up 6%, home sales as a whole aren’t as high as last year.

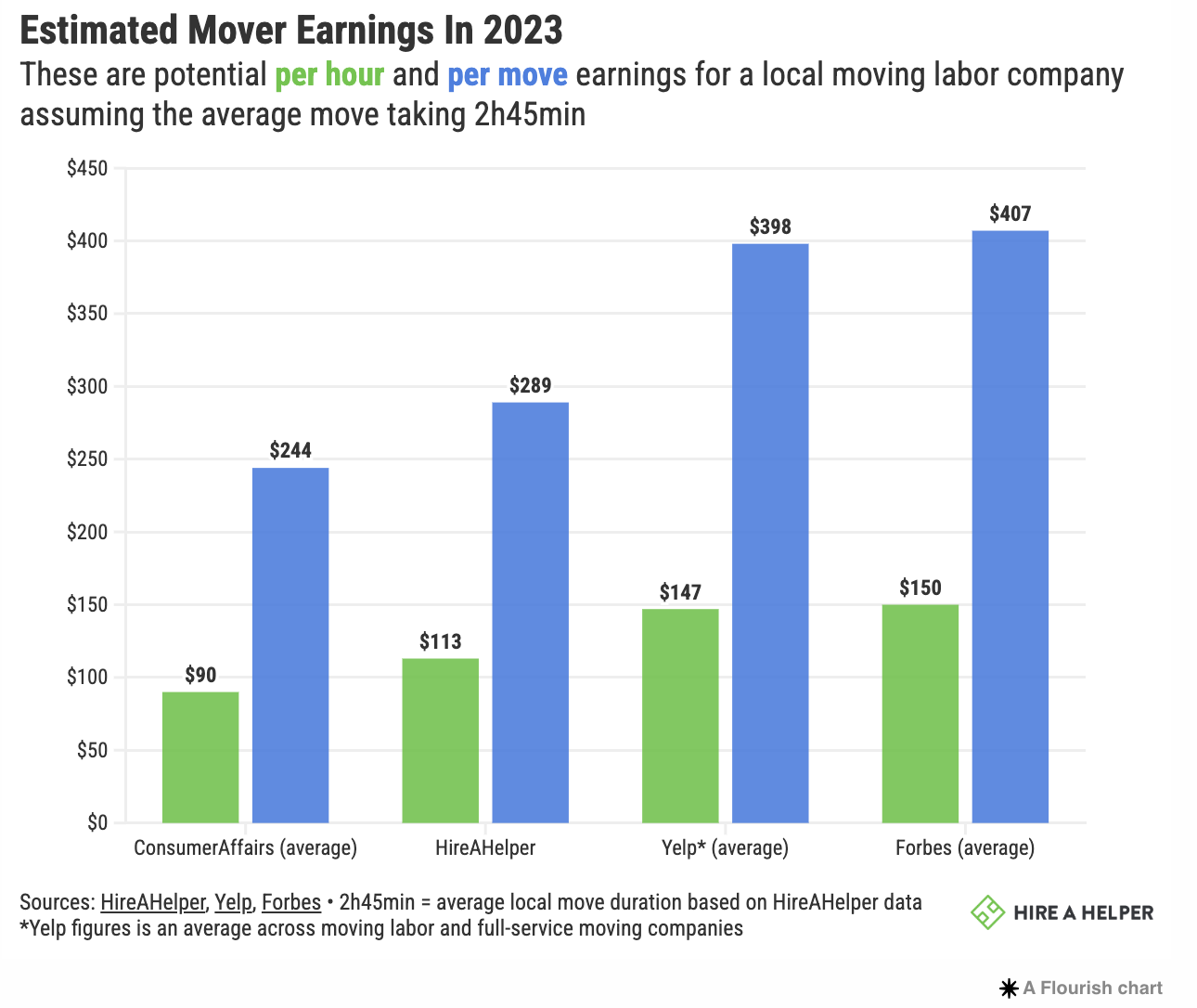

The cost of moving has also grown 4% in 2023 (ahead of inflation rates), and this is actually good news! It means movers’ earnings have most likely also increased. So if you’re interested in adding a side hustle to your income, starting a moving labor company is well worth considering.

Findings from 2023 Study on Moving Labor

In 2023, a typical moving company earns between US$90 and $150 per hour on average, or from $244 to $407 per move

Mover earnings in 2023 are highest in Birmingham, AL where average hourly earnings on a labor-only move reached $146

The state with the greatest demand is Mississippi, with 434 moves per moving company registered in the state

What is a Moving Labor Company, and can it work as a Side Hustle?

You can start a side hustle as a full-service mover. These are the huge van line companies, and they tend to offer the whole service package and charge significantly more. Moving labor companies are often responsible for loading, unloading, and, sometimes (though rarely), packing up people’s possessions.

Why is labor-only so profitable?

Here are a few more reasons why moving labor is a good choice for a side hustle:

You don’t require a special mover’s license in most states

No need to invest in your own truck or spend money on gas

With almost half (48%) of all moves taking place on the weekend, you can keep this side hustle alongside your main job or your studies

Fast Facts about Moving Company Earnings in 2023

Here are some estimates on moving marketplace earnings:

How much revenue do movers make per hour?

In 2023, the average amount a moving labor company earned on HireAHelper is $113 per hour (after fees). That rate is based on the service of two movers loading and unloading a customer’s belongings and does not include potential tips.

According to Forbes, local movers usually charge between $50 to $250 per hour in 2023. Continue Reading…