Hub Blogs contains fresh contributions written by Financial Independence Hub staff or contributors that have not appeared elsewhere first, or have been modified or customized for the Hub by the original blogger. In contrast, Top Blogs shows links to the best external financial blogs around the world.

In what it says is its first new ETF announcement in four years, Vanguard Investments Canada Inc. today announced a new Fixed-Income ETF designed to met investors’ short-term savings needs. Here is the full release on Canada News Wire.

Trading on the TSX under the ticker VVSG, Vanguard Canada says the Vanguard Canadian Ultra-Short Government Bond Index ETF offers AAA-rated high-quality government bonds and treasury bills with a low management fee of 0.10%. It seeks to track the Bloomberg Canadian Short Treasury 1-12 month Float Adjusted Index. The release says the ETF will invest primarily in public, investment-grade government fixed-income securities with maturities of less than 365 days issued in Canada.

Vanguard Canada’s first new ETF in 4 years

In an email to me, Vanguard Canada spokesman Matthew Gierasimczuk confirmed “It’s our first ETF launch in four years.” It brings the total number of Vanguard ETFs in Canada to 38, with $80 billion (CAD) in Canadian ETF assets under management. You can find the full list on its website here. Continue Reading…

In the quest for Financial Independence through savvy investing, we’ve gathered insights from Presidents and CEOs to share their top index fund picks.

From choosing a high-dividend yield ETF to recommending a total stock market index fund, explore the seven expert recommendations that could pave your path to financial freedom.

Choose High-Dividend Yield ETF

Suggest Vanguard Total Stock ETF

Prefer Zero Fee Total Market Fund

Select Australian-Domiciled International ETF

Opt for Monthly Distribution Index

Pick Broad-Market S&P 500 ETF

Recommend Total Stock Market Index Fund

Choose High-Dividend Yield ETF

My go-to for building Financial Independence has got to be the Vanguard High-Dividend Yield ETF. A lot of folks who’ve made it to FIRE (Financial Independence, Retire Early) live off dividends, and if that’s your goal, this ETF is worth considering. It sports a yield of 3.65% and keeps costs low with an expense ratio of just 0.06%. The fund aims to mirror the performance of the FTSE High-Dividend Yield Index.

It’s packed with stocks known for higher-than-average yields. You won’t find many fast-growing tech stocks here because those companies usually reinvest their profits into growth rather than paying out dividends. Instead, the ETF focuses on older, established companies with a strong history of profitability. As of the last update, the top five holdings included big names like Johnson & Johnson, JPMorgan Chase, Procter & Gamble, Verizon Communications, and Comcast.

While it might not match the S&P 500 in terms of rapid growth or impressive returns, the stability and consistent income it offers can be a major advantage, especially if you’re looking for reliable dividend income. — Eric Croak, CFP, President, Croak Capital

Suggest Vanguard Total Stock ETF

As a CFO, I recommend index funds like the Vanguard Total Stock Market ETF (VTI) for building long-term wealth. It provides broad exposure to over 3,600 U.S. stocks with an ultra-low expense ratio of 0.03%.

Over the past 25 years, the total U.S. stock market has returned over 9% annually. While volatile, for long-term investors, index funds are a simple, low-cost way to earn solid returns. I have leveraged index funds in my own portfolio and for clients to build wealth over time.

Vanguard’s scale and expertise allow for minimal costs and maximum tax efficiency. For small or large portfolios, VTI should be a core holding. For clients aiming to retire early or build wealth, low-cost broad market exposure is the most effective strategy. Total U.S. stock market funds provide the broadest, most diversified exposure available. — Russell Rosario, Owner, RussellRosario.com

Prefer Zero-Fee Total Market Fund

The Fidelity Zero Total Market Index Fund is my top pick for building Financial Independence. It covers the full spectrum of the U.S. market without charging any management fees, which means your investment grows faster without extra costs. This fund’s wide exposure to both established and emerging companies helps balance risk and reward. For anyone serious about long-term growth, it’s a great tool to steadily build wealth over time. — Jonathan Gerber, President, RVW Wealth Continue Reading…

When I ask clients and prospective clients about the return expectations they have for their portfolios, the responses vary wildly … anywhere from ‘about 5%’ to ‘over 10%.’ Almost all of these expectations are too high.

Admittedly, clients have different risk profiles leading to different asset allocations and ultimately, different outcomes. That’s reasonable. A problem crops up when otherwise reasonable people have been socialized into having out-sized expectations. How does one ethically re-calibrate expectations for irrational optimists who nonetheless think they’re within their rights to have those expectations?

The behavioural finance concept is overconfidence, although the attitude involves elements of optimism bias, cognitive dissonance and old-fashioned hubris, too. To quote J.M. Keynes: “Markets can remain irrational longer than you can remain solvent.” Few investors are prepared to acknowledge that the recent bull market seems unlikely to continue and that a recession appears to be on the horizon.

Learning from past Crashes

If we have learned anything from the great crashes of 1929, 1974, 2001 and more recently, the global financial crisis, it is that investors (often spurred by accommodative policy positions) can come to think of themselves as being all but invincible when central bankers are accommodative. Too often, they also lose their nerve when markets tumble and stay low for a prolonged period.

A good deal of personal finance is grounded in social psychology: especially group psychology. People can get ahead through investing not only by being shrewd about valuations and such, but also by accurately anticipating how other market participants might react to a given set of circumstances. Of course, it cuts both ways: and having reasonable expectations in the first place often assists investors in staying the course.

My concern is with the messaging being offered by many in the personal finance community these days is something I call “Bullshift.” The industry shifts peoples’ attention to make them feel more bullish. To hear many in the business tell it, there’s no appreciable need to be concerned about high valuations, high debt levels (both public and private), a long-inverted yield curve and interest rates at generational highs. Any one of these considerations would ordinarily give a rational investor pause. Taken together, they pose a clear and present danger for investors in the second half of 2024. Few seem concerned and it is that very lack of concern that concerns me.

Misleading investors with “Bullshift”

There is a directionally and mathematically accurate ad running by Questrade making the rounds that doesn’t tell the whole picture, either. Again, even the ‘good guys’ tend to mislead the average investor with Bullshift. The advertisement shows what you would earn over a long timeframe at 8% and what you would earn at 6%.

My question to you is simple: is it reasonable to assume an 8% return is even possible? There is longstanding evidence that higher-cost active investment strategies actually fail to outperform cheaper strategies such as passive index investing and that product cost certainly does matter. Continue Reading…

Here are some of the ways ETFs can be used strategically to help you sleep better at night.

Image courtesy BMO ETFs/Getty Images

By Erin Allen, VP, Online Distribution, BMO ETFs

(Sponsor Blog)

Volatility is often seen as the price of admission for achieving investment returns, but too much of it can feel like paying a hefty fee for a ride on an intense roller coaster, only to find yourself feeling queasy by the end and unable to enjoy the rest of the amusement park.

If the recent stock market turbulence in early August has left you contemplating panic selling, take a moment to breathe. Market corrections are a normal and healthy aspect of investing, and your portfolio doesn’t have to experience such dramatic ups and downs.

Why? Well, various defensively oriented ETFs can offer strategic ways to manage and mitigate risk, helping you stay the course and remain invested through the market’s inevitable fluctuations. Here are some ideas featuring BMO ‘s ETFs lineup:

Low-volatility ETFs

Imagine the broad market, such as the S&P 500 index, as a vast sea where the waves represent market volatility, and your investment portfolio is your boat navigating these waters.

How your boat responds to these waves is dictated by its beta, a measure that indicates both the direction and magnitude of your portfolio’s fluctuations relative to the market.

To put it simply, if the market’s “waves” have a beta of 1, and your portfolio also has a beta of 1, this means your portfolio will typically move in sync with the market, rising and falling to the same degree.

Now, consider if your boat were lighter and more susceptible to the waves, symbolized by a beta of two. In this scenario, your portfolio would be expected to swing twice as much as the market: more pronounced highs and lows.

Conversely, imagine your boat is a sturdy cargo ship with a beta of 0.5. In this case, your portfolio would react more calmly to market waves, experiencing only half the ups and downs of the market. This stability is what low-beta stocks can offer, and they can be conveniently accessed through various ETFs.

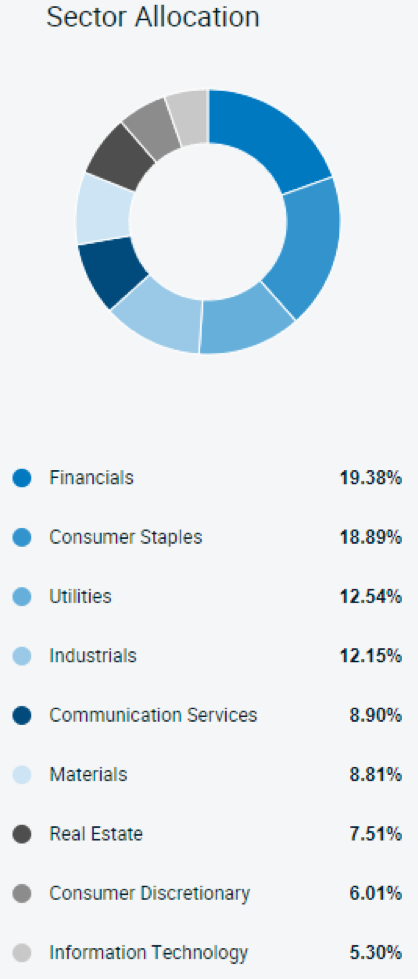

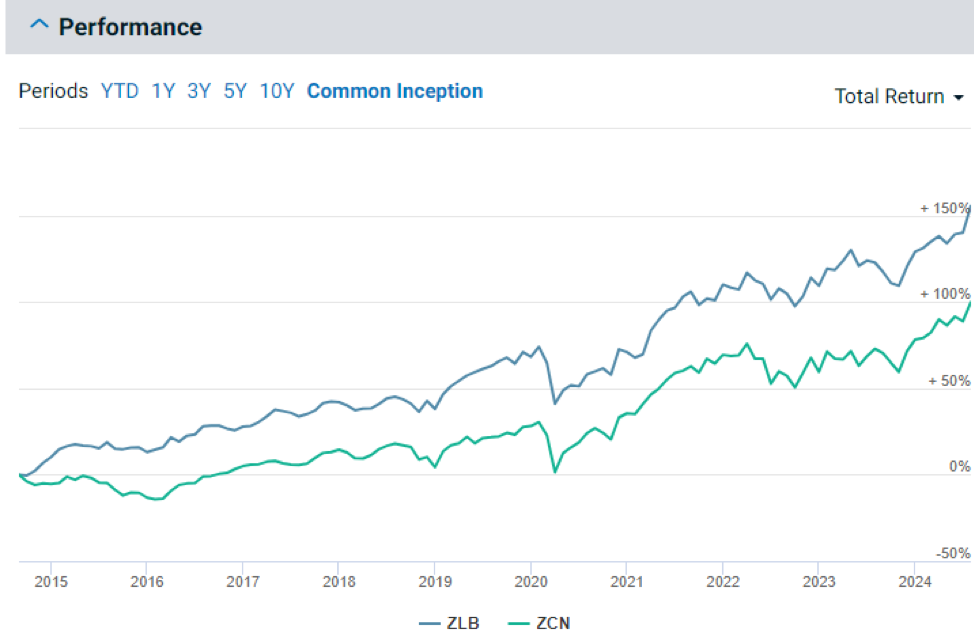

One such example is the BMO Low Volatility Canadian Equity ETF (ZLB)1, which selects Canadian stocks for their low beta. Compared to the broad Canadian market, ZLB is overweight in defensive sectors like consumer staples and utilities, which are less sensitive to economic cycles.

Holding allocations are as of August 19, 2024; sourced here1.

This ETF not only offers reduced volatility and smaller peak-to-trough losses compared to the BMO S&P/TSX Composite ETF (ZCN)2 but has also managed to outperform it — demonstrating that it is very much possible to achieve more return for less risk2.

While ETFs like the ZLB1 are engineered for reduced volatility through low-beta stock selection, it’s important to remember that they still hold equities.

In extreme market downturns, such as the one experienced in March 2020 during the onset of COVID-19, these funds can still be susceptible to market risk. This is pervasive and unavoidable if you’re invested in stocks; it affects virtually all equities regardless of individual company performances.

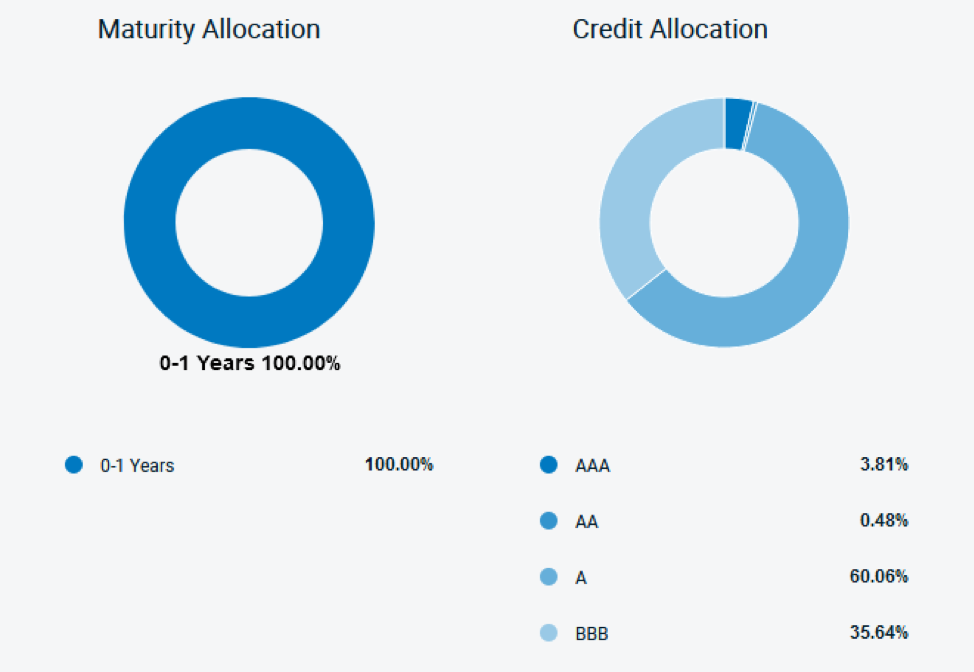

To fortify a portfolio against such downturns, diversification into other asset classes, particularly bonds, is crucial. However, not just any bonds will do — specific types, like those held by the BMO Ultra Short-Term Bond ETF (ZST)6, are particularly beneficial in these scenarios.

ZST, which pays monthly distributions, primarily selects investment-grade corporate bonds6. The focus on high credit quality, predominantly A and BBB rated bonds, is critical for reducing risk as these ratings indicate a lower likelihood of default and thus, offer greater safety during economic uncertainties.

Moreover, ZST targets bonds with less than a year until maturity6. This short duration is pivotal for those looking to minimize interest rate risk. Short-term bonds are less sensitive to changes in interest rates compared to long-term bonds, which can experience significant price drops when rates rise.

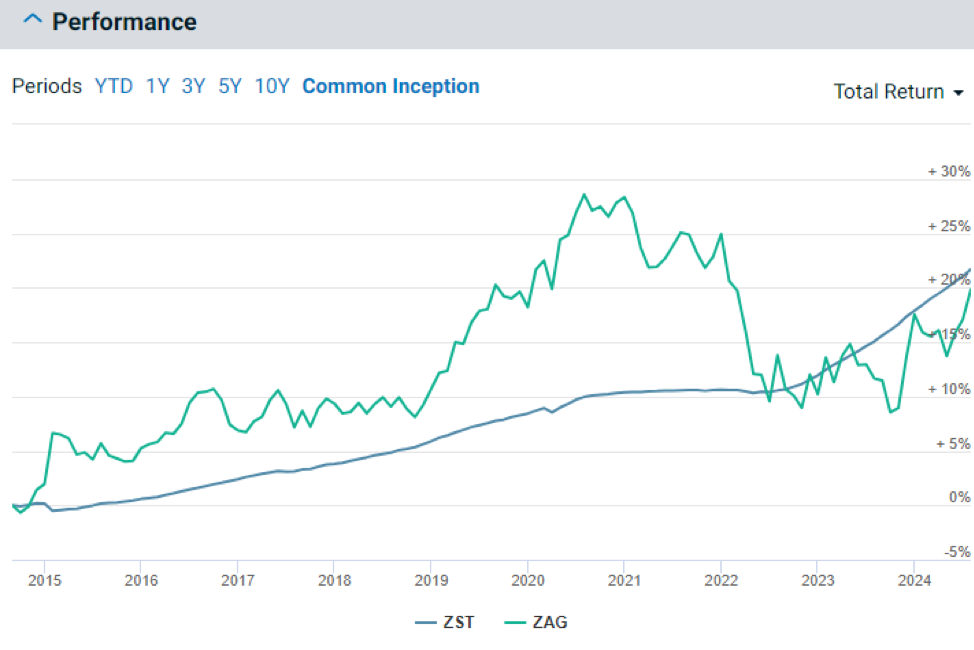

Charts as of July 31st, 2024 6

This strategic combination of high credit quality and short maturity durations7 is why, as demonstrated in the chart below, ZST has been able to steadily appreciate in value without experiencing the same level of volatility as broader aggregate bond ETFs like the BMO Aggregate Bond ETF (ZAG)8.

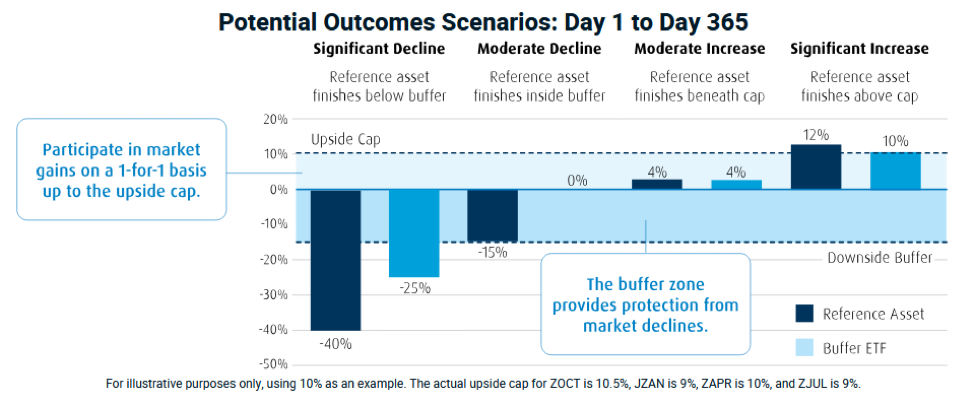

Buffer ETFs

If you recall the days of using training wheels when learning to ride a bike, you’ll appreciate the concept of buffer ETFs. Just as training wheels keep you from tipping over while also limiting how fast and freely you can ride, buffer ETFs aim to moderate the range of investment outcomes — both up and down.

Buffer ETFs may sound complex, but the principle behind them is straightforward. These ETFs utilize options to limit your downside risk while also capping your potential upside returns.

For example, a buffer ETF might offer to limit your exposure to a maximum 10% price return of a reference asset (like the S&P 500 index) over a year while absorbing the first -15% of any losses during the same period.

If the reference asset rises, your investment increases alongside it, up to a 10% cap. However, if the reference asset declines, the ETF absorbs the first 15% of any loss. Only after this “downside buffer” is exhausted would you start to experience losses.

BMO offers four such buffer ETFs, each named according to the start month of their outcome period when the initial upside cap and buffer limits are set. These include: Continue Reading…

Before we dive into this article, let’s play a quick game: a word association game. I’ll bet you a crisp $5 bill, or a shiny loonie for the more risk averse out there, that with three chances, I can guess the first word that pops into your head. Now, it has to be the first word, so no cheating. Ready, set… the word is ‘Retirement.’

If you said ‘Retirement Income,’ ‘Retirement Savings’ or ‘Retirement Home,’ I’ll come to collect my winnings. If you said anything like ‘Travel,’ ‘Hobbies’ or ‘Exploration, then good on you; I’ll send along an IOU.

The reason I felt so confident taking that bet is because when I tell people that I work in retirement planning, 99 out of 100 times, they assume that I work in financial services. The other time, people ask about senior living. Retirement has become so synonymous with financial planning, and so associated with ‘old age,’ that they’re practically inseparable. Yet, in reality, retirement is a stage of life, not a date on the calendar, an amount in your bank account, and is certainly not a death sentence. One of our primary goals when creating our startup, RetireMint, was to reframe the national conversation around “what it means to retire,” which, at its core, requires redefining how Canadians prepare for retirement.

Now, I am not discounting the importance and necessity of a sound financial plan. After all, you are reading this in Financial Independence Hub … Yes, financial planning is the keystone of retirement preparation, as you won’t even be able to flirt with the idea of retiring without it. Yet, retirement planning must adopt a much wider definition and break free from the tethered association of solely financial planning.

Retirement should really be a time to enjoy the fruits of your hard labour: a chapter that will hopefully span decades, fuelled by leisure, exploration, discovery and meaning.

Answering the ‘what, where and how’ of everything you want to see, do and accomplish in this next chapter requires conscious preparation in areas far beyond spreadsheets and bank statements.

The industry paradigm is that you have about 8,000 days in retirement, or around 22 years. In each of those years, you will have more than 2,000 hours of new-found free time that would have been spent working throughout the majority of your life. Filling these thousands of hours with meaningful and purposeful activity is much more easily said than done.

The common approach to retirement planning (yes, we are now using the wider definition) has been to ‘punt the ball down the field’ and ‘cross that bridge when you get to it.’ Yet, we see time and time again that those who leave their lifestyle planning to their first day of retirement are the ones who have the hardest time transitioning into this next chapter.

The people who say, “I’ll never get tired of sipping Piña Coladas on a beach,” face the same fate as the ones who say “I can’t wait to golf every day.” While these may be dream activities for retirees, they ultimately see diminishing returns if they’re your only activities, because humans are funny creatures: we need meaning and variation.

Despite its innocent demeanour, retirement has some dark, inconvenient truths:

Ages 50-64, 65-84 and 85+ have the three highest suicide rates in North America, and in the last five years, we’ve seen a 38% increase in suicides among Baby Boomers.

Canadians over 65 have a divorce rate three times the national average.

Over 25% of older Canadians are socially isolated, which causes a 50% increased risk of dementia.

And, 77% of older Canadians live with at least two chronic illnesses or conditions.

It’s statistics like these that starkly highlight the importance of planning for your lifestyle, wellness and purpose, as well as the need for trusted resources to help with this planning. This was the a-ha moment that sparked our urgency to develop RetireMint.

RetireMint stemmed from empirical evidence showing that once people’s finances are at least on the right track, their primary concerns and conversations with their financial advisors shift far beyond the scope of their meetings. “What am I going to do with the grandkids?,” “Where am I going to travel?” “What happens when I lose my work insurance coverage?,” are just a few of the plethora of questions that popped up time and time again.

It’s fantastic that Canadians have this level of trust and comfort with their advisors, but the truth is that financial advisors are not equipped to answer all of these broader retirement inquiries, and they’ll be the first to admit it. It’s clear that this undue burden falls on the shoulders of financial professionals, but if not for them, who is going to provide the answers? Continue Reading…

In what it says is its first new ETF announcement in four years, Vanguard Investments Canada Inc. today announced a new Fixed-Income ETF designed to met investors’ short-term savings needs. Here is the full release on Canada News Wire.

In what it says is its first new ETF announcement in four years, Vanguard Investments Canada Inc. today announced a new Fixed-Income ETF designed to met investors’ short-term savings needs. Here is the full release on Canada News Wire.