Once you achieve Financial Independence, you may choose to leave salaried employment but with decades of vibrant life ahead, it’s too soon to do nothing. The new stage of life between traditional employment and Full Retirement we call Victory Lap, or Victory Lap Retirement (also the title of a new book to be published in August 2016. You can pre-order now at VictoryLapRetirement.com). You may choose to start a business, go back to school or launch an Encore Act or Legacy Career. Perhaps you become a free agent, consultant, freelance writer or to change careers and re-enter the corporate world or government.

Planning major purchases during retirement requires aligning income timing, market conditions, and long-term financial stability to support lasting flexibility.

Image courtesy Adobe Stock/peopleimages.com

By Dan Coconate

Special to Financial Independence Hub

Retirement changes how income flows, which means planning major purchases during retirement requires a more deliberate approach than it did during peak earning years. Instead of relying on a steady salary, retirees draw from savings and structured income sources, so each major expense must fit within a longer financial horizon.

Careful planning allows individuals to move forward with confidence while preserving the stability that supports future years, particularly when financial decisions must stretch across an extended retirement timeline.

Understanding how Cash Flow Evolves

Income arrives differently after retirement, and each source carries its own implications when funding a large purchase. Withdrawals from registered accounts may affect taxes, while selling investments can alter long-term growth potential, which makes timing a central consideration.

When retirees map out funding strategies before committing, they gain a clearer sense of how the purchase will influence future income. That preparation reduces the risk of decisions that feel manageable in the moment, but creates pressure later, especially when income must stretch across decades and support both planned and unplanned expenses.

Weighing Lifestyle Value with Financial Reality

Major purchases reflect personal priorities, whether that involves extended travel or a second property that supports time with family. These decisions carry meaning, yet they still require a disciplined evaluation of ongoing costs and expected use.

In the case of recreational real estate, retirees may notice that waterfront properties appeal to vacation home buyers because of their setting and long-term desirability. That perspective fits within a broader assessment, since ownership involves upkeep and financial commitments that must align with retirement goals and long-term affordability, particularly when property ownership extends beyond seasonal use.

Considering Market Conditions before Committing

Financial markets influence both the cost of large purchases and the resources used to fund them, which makes timing an important part of the decision. Selling assets during a strong market period may reduce pressure on a portfolio, while moving forward during a downturn can create a strain that lingers.

A disciplined timing strategy allows retirees to act when conditions support the purchase. Maintaining that discipline supports a more stable financial path, even as markets fluctuate, and reinforces the value of patience when making high-impact financial decisions that cannot be easily reversed or adjusted once completed.

Preserving Flexibility for Future Needs

Large purchases should not restrict the ability to respond to unexpected developments, since retirement still brings changes that require financial attention. Healthcare needs and property repairs can emerge without warning, making flexibility a key part of any plan. Continue Reading…

The modern worker faces rapid inflation in housing and consumer prices. This results in reduced savings and financial insecurity. As a result, the Financial Independence/Retire Early (FIRE) movement has garnered many loyal followers. Individuals are saving aggressively and investing wisely to retire early and have enough money to cover living expenses.

Understanding Financial Independence

Financial Independence is achieved when an individual can cover daily expenses without having to work. One of the biggest ones is renting or owning a home. In 2023, more than 21 million renters spent over 30% of their income on housing.

Since housing consumes a large share of income, people are looking to move to areas with lower rents. This salary-to-housing ratio is even more skewed in high-cost urban areas, where rent prices are sky-high, such as in New York, Los Angeles and Chicago. There are plenty of other cities that provide the same energy while having a more affordable cost of living.

Moving to a Lower Cost-of-Living Area

There are plenty of things to consider before moving to cities with a lower cost of living:

Benefits

Geographic locations also directly impact living costs such as rent, food, utilities, transportation and healthcare. With lower expenses, individuals can afford more luxuries like dining out compared to when residing in high-cost cities. Individuals can lead more relaxed lives due to less financial stress. Other factors to improve one’s quality of life include access to nature, community amenities and smaller populations.

Reduced expenses due to a lower cost of living can accelerate savings over time, especially when directed to diverse investment accounts, retirement accounts and income-generating assets, helping individuals gain Financial Independence earlier.

Moving Tasks

Before deciding on new locations, people can create structured plans regarding moving expenses, new living costs and potential earnings. Employment rates, average salaries and cultural opportunities need to be researched and compared with their current lifestyles.

Housing and job searches should also be handled before the move. After moving, local communities, online forums and professional networks can help ease the transition into the new city. Financial goals should also be reassessed to reflect changes in income and expenses to maintain progress toward FIRE.

Sacrifices and Trade-offs

Since 2017, home purchases rose by 81%, while rent prices rose by 54% compared to a 43% increase in earnings. To further increase savings, people can downsize their living spaces or sacrifice proximity to major urban areas.

They might experience an initial discomfort with the change in lifestyle, but that will be outweighed by the potential long-term financial benefits. By assessing what to give up, professionals can gain more control over their finances and way of life. They can be more prepared for emergencies or other future situations.

5 Affordable U.S. Cities to Accelerate the Financial Independence Journey

1. Grand Rapids, Michigan

Grand Rapids, Michigan, can help individuals significantly reduce expenses due to the city’s growing economy and consistent job opportunities. They also don’t have to sacrifice lifestyle quality, as the Grand Rapids area is known for its wide range of outdoor activities, emerging art scene and friendly communities.

2. Austin, Texas

Austin, Texas, is a burgeoning tech hub with more affordable rents than in Silicon Valley and Seattle. Tech presence in Austin includes Apple, Tesla, Dell, AMD, Amazon, Google, IBM, Meta, Microsoft and Samsung, among others. Besides its tech scene, Austin has a vibrant music community and plenty of outdoor activities at Lady Bird Lake, Mount Bonnell and Barton Creek Greenbelt. The city also offers a distinct food scene, especially Texas barbecue and tacos.

3. Boise, Idaho

Boise is an ideal city to relocate to for individuals looking to save on living costs. The city offers stunning landscapes without breaking the bank on rent, making it perfect for families and young professionals alike. Residents have plenty of activities to explore in the city, including hiking, biking and skiing. It has a solid job market, a stable economy and plenty of amenities for different lifestyles. Boise also has top-rated schools with relatively lower utility and transportation costs.

4. Charlotte, North Carolina

Charlotte is growing as a major financial, healthcare and tech center, making it a great option for many young professionals. The city also has plenty of welcoming communities with diverse interests and backgrounds. The cost of living here is lower than in other ultra-urban cities, which makes day-to-day living and saving significantly more hassle-free. Residents can drive to the Blue Ridge Parkway for a relaxing weekend trip in the Great Smoky Mountains.

5. Richmond, Virginia

Richmond, Virginia, is great for those who are inspired by a place’s historical significance. It also offers significant modern growth, cost-of-living affordability and culture. The city has plenty of galleries, theaters and music venues for any art-loving individual. Community events and volunteer opportunities are plentiful.

Embracing a Strategic Move for Financial Freedom

The Financial Independence Retire Early movement is widely known. It encourages individuals to save more, invest in income-generating assets and retirement accounts to be able to retire earlier than the rest of the workforce.

Relocating to lower-cost cities is one of the most viable paths toward increased savings. There are plenty of cities with a vibrant energy, welcoming communities and plenty of activities. In the right locations, individuals can increase savings without sacrificing quality of life, but proper planning before moving is essential to achieving a fulfilling lifestyle.

Dan Parks is a senior writer at Modded.com. Based in Washington, D.C., Dan has a proven track record of distilling complex subjects into accessible narratives across various fields. His expertise in clear communication and meticulous research makes him a valuable contributor to discussions on personal finance and investment strategy, helping readers navigate intricate topics with ease. Dan is dedicated to providing readers with well-researched insights to foster financial literacy and independence.

Bitcoin has become an increasingly accessible asset for investors, with growing participation from both institutional and retail investors through regulated investment vehicles. Institutional adoption, new regulatory frameworks and improved custody solutions continue to bring Bitcoin further into the mainstream.

Cryptocurrency ownership among U.S. investors has increased from 6% in 2021 to 17% in 2025, according to Gallup[1].

At Hamilton ETFs, we focus on developing innovative solutions that address real portfolio needs. As interest in Bitcoin has grown, we saw an opportunity to apply our options expertise to the asset class in a way that addresses the needs of income-oriented investors while avoiding the traditional trade-off between income generation and upside participation.

Introducing BDAY

The Hamilton Enhanced Bitcoin DayMAX™ ETF (BDAY) is a first-of-its-kind strategy designed to provide 100% exposure to Bitcoin’s potential upside while generating income through Hamilton’s innovative DayMAX™ strategy, which utilizes zero-days-to-expiration covered call writing (0DTE).

Until now, investors seeking income from Bitcoin have generally faced a trade-off: generating option premium in exchange for less Bitcoin upside potential. By not writing call options on BDAY’s Bitcoin holdings (achieved through investing in IBIT, iShares Bitcoin Trust ETF), we preserve full participation in Bitcoin: up or down. In addition, the actively managed DayMAX™ covered call strategy offers more opportunities for income generation by monetizing volatility every day.

In short, BDAY consists of:

100% Bitcoin exposure, via iShares Bitcoin Trust ETF (IBIT), without covered calls

25% Nasdaq 100 exposure, via Invesco NASDAQ 100 ETF (QQQM), from modest leverage, on which to apply 0DTE options strategy to generate attractive semi-monthly income

The DayMAX™ advantage

BDAY brings our popular DayMAX™ approach to investors seeking Bitcoin exposure and income. Rather than writing covered calls directly on Bitcoin, BDAY generates attractive tax-efficient yield through a separate QQQM sleeve and an actively managed 0DTE covered call strategy.

This structure allows the portfolio to clearly separate its roles. Bitcoin serves as the growth potential, providing 100% exposure to the asset, while QQQM in conjunction with the DayMAX™ strategy is used to generate option premium income.

Expectations of the future shape how we behave today, especially when it comes to planning for retirement. When people overestimate or underestimate where their retirement income will come from, it can affect how they save, how they plan, when they retire, and how financially secure they feel over time.

That sounds simple enough. But retirement has a way of making simple things complicated.

Recent research from CAAT Pension Plan shows a clear gap between what working Canadians expect retirement to look like and what retirees actually experience.

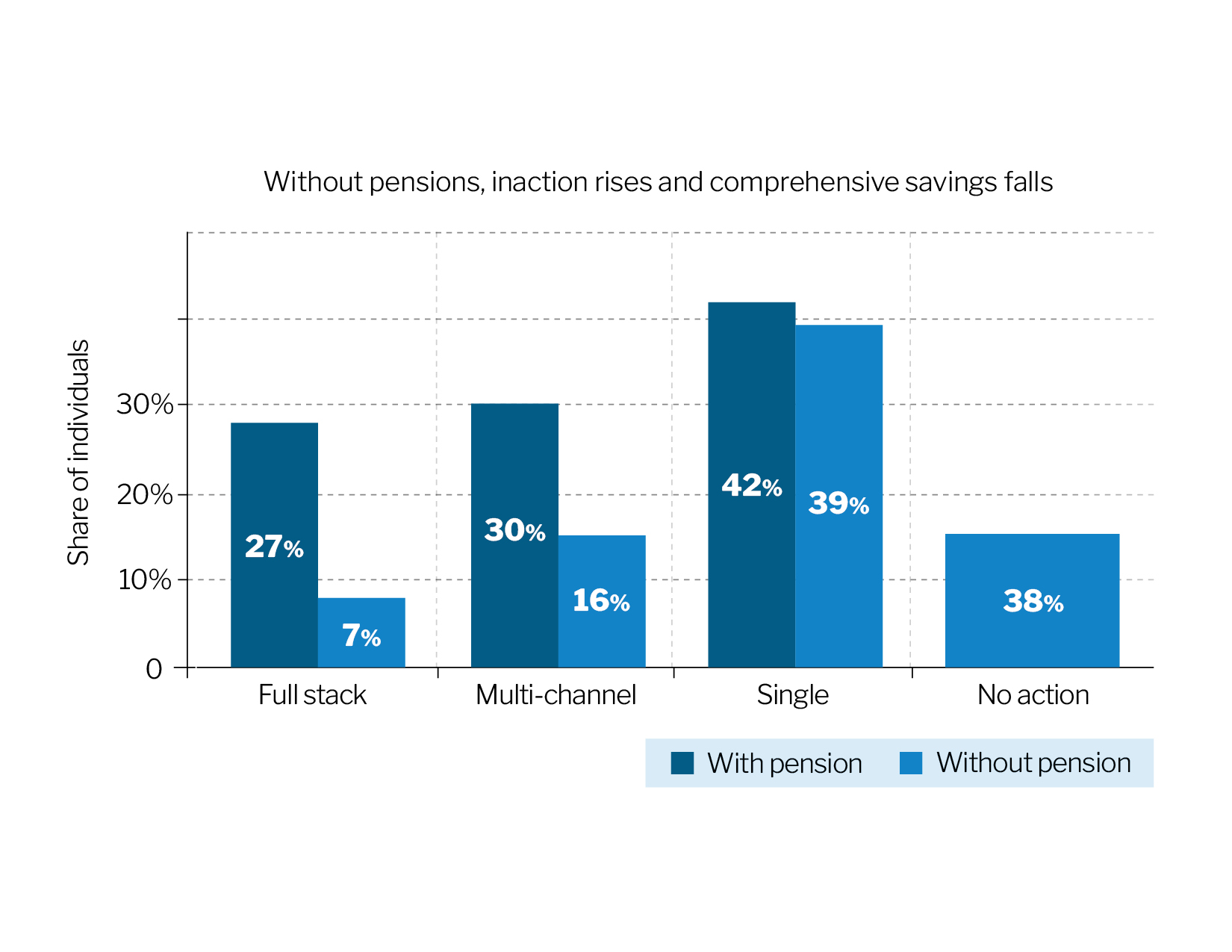

The retirement we picture

Nearly one in four working Canadians expect personal savings to be their primary source of income in retirement. In reality, only about one in seven retirees rely on personal savings as their primary source of income.

At the same time, working Canadians appear to underestimate the role of workplace pensions. Among working people with a pension, only 10% expect it to be their primary source of income in retirement. But among retirees with a pension, 23% say their pension is their primary income source. Pensions are a foundational source of income for many. Retirees with pensions report approximately $2,750 more in average monthly household income than retirees without pensions.

For many Canadians, that is the difference between getting by and living well. Defined Benefit [DB] pensions can provide a predictable stream of retirement income, reduce the burden of managing investments alone, and help protect against the risk of savings running out.

This expectation gap matters because expectations are not harmless. If people expect personal savings to carry more significance than they realistically will, they may delay planning, undersave, or assume they will have more time to catch up later. That can increase the risk of outliving savings, delaying retirement, or becoming more dependent on public supports.

The reality today is that 38% of Canadians without a workplace pension report taking little or no action toward saving for retirement. Among Canadians with household income below $50,000, that figure rises to 60%.

This can show up as delayed retirement. For Canadians, the average ideal retirement age is 60, while the average expected retirement age is 67. For many people, there is a meaningful seven-year gap between the retirement they hope for and the retirement they think is realistic.

There is a quiet lesson in that gap. When people do not have a clear path to retirement, they do not always change their savings behaviour today. Sometimes they change their expectations about tomorrow.

The pension habit

This research challenges the idea that pensions crowd out personal saving. Savings habits are an important building block in creating predictable income in retirement. Pensions can act as a foundation for those habits because they make saving structured, automatic, and easier to sustain.

This matters because good financial behaviour is often less about willpower than design. If saving depends on making the right decision every month, life has plenty of opportunities to get in the way. A pension changes the architecture of the decision. It turns saving from something people have to repeatedly choose into something that happens more reliably in the background.

The research suggests this happens in the real world. Pension plan members are nearly four times more likely than non-pension plan participants to report using a full suite of retirement savings tools, such as TFSAs, RRSPs, and non-registered accounts. Specifically, 27% of pension members use a full suite of savings tools, compared with just 7% of those without a pension.

Canadians with workplace pensions are also more likely to use multiple savings approaches at the same time, 30% compared with 16% of those without a pension.

Access is the real barrier

Many Canadians want to save, but they do not always have access to the tools that make saving easier. Continue Reading…

On paper, Financial Independence Retire Early (FIRE) is a simple concept: spend less than you earn, grow your savings gap, optimize your taxes, invest your savings, and wait for your money to compound over time.

But one thing that doesn’t get covered enough with the FIRE movement is the relationship side of money.

To be more specific, if you’re on the FIRE journey with a partner, how do you make sure the two of you are aligned? After all, if you and your partner aren’t on the same page, none of it matters.

For us, Mrs. T and I have been on the FI journey since 2011. This year marks the 15th year of our journey. That’s 15 years of saving, budgeting, investing, making difficult financial decisions, and occasionally having disagreements on money-related decisions.

I figure it’s worthwhile to spend some time discussing how we stay aligned on money and some of the relationship challenges we have faced since we started our FI journey.

How it all started: The financial epiphany

Although both of us came from frugal backgrounds and we both learned in our youth to spend less than we earn, we didn’t really focus on optimizing our finances or investing intentionally when we started dating and when we started living together.

It wasn’t until we read the Secret of Millionaire Mindset that we started having deeper and more detailed conversations about money and how we want our financial future to be. Around the same time, we were also considering getting married, so it was important to make sure we were both aligned on our future financial plans. We both recognized that building wealth through saving and investing could give us more options and freedom in the future.

But just because we talked about money didn’t mean we always agreed on every financial decision we made.

Far from that!

How we are different due to our money personalities

Mrs. T and I don’t think about money the same way.

Deep down, I’m an “extreme” saver and optimizer. I’d always find ways to optimize things and try to save as much money as possible. Even if I could save 50% on something, I would try to find more ways to save another 20%.

Mrs. T, on the other hand, is a more balanced saver. She doesn’t like spending money unnecessarily, but typically won’t climb the mountain to see if she could save even more.

Another way we are different is that I’m a self-proclaimed spreadsheet nerd. I am a numbers person and I love spreadsheets. I have many different spreadsheets tracking different things and data, charting our historical trends and projecting future ones. Whenever I see data in spreadsheets, I see data and optimization opportunities.

Mrs. T likes spreadsheets too but not nearly to the extent that I do.. She’s more practical and intuitive. She cares whether we have enough and whether we can enjoy life now without sacrificing our future. She likes to see things from the 30,000-foot view rather than getting into the nitty-gritty details, as I do.

Our different money personalities created some disagreements and discontent when we first started our FI journey. For example, Mrs. T enjoyed going to a cafe to have great conversations while having a good cup of coffee and delicious pastries (i.e. having hygge). Meanwhile, I would calculate in my mind how much money we could have saved and invested if we hadn’t spent the money.

Realizing what we needed to keep us aligned

Over time, I realized my save-save-save-then-save-more default mentality wasn’t healthy. I learned that I need to relax and spend money to enjoy the present moment. On the flip side, Mrs. T began to understand my worries and my insecurity with not having enough money and started to cut back slightly on the “nice to have” expenses.

We found our “balance” by meeting each other in the middle. We both learned that it’s vital for us to stay aligned financially. These are some systems and habits that have helped us:

Regular money conversations

We talk about money regularly but we try to keep it natural and relaxed rather than turning these chats into formal meetings. We’ll talk about money over meals, over coffee hygge, or while driving. Quite often, we involve both kids and explain to them why we are talking about these topics. In our household, we don’t shy away from money talks, we encourage them.

These money conversations happen regularly, sometimes multiple times a day. We keep them very casual and relaxed. Although we have regular money conversations, we don’t discuss our investment portfolio and net worth daily. We want to ignore the noise and focus on the long term. I’m in charge of the details and I provide Mrs. T the big picture updates without overwhelming her with all the details. So when it comes to investment portfolio and net worth, we typically discuss them in detail every quarter.

Reviewing our expenses: focusing on the trends rather than amount spent

When we first started tracking our expenses and using our budget system, I was very much focused on how much we spent on the different categories every month. I wasn’t looking at the big picture and certainly wasn’t focusing on the spending trend.

As our net worth grew larger and we had a few years of spending data on our hands, we finally developed a system that works for us. Every 6 months, Mrs. T and I will sit down for about 10 to 15 minutes to look at our spending spreadsheet. We look at the trends and see if there are categories we are overspending or underspending. If we are overspending in a certain category, we try to find out why. For example, if we were spending more than usual on dining out, perhaps it was because we had friends or family visiting.

Making the financial big decisions together

For the most part, I manage our investment portfolio and make the buying and selling decisions. Sometimes I would consult with Mrs. T if I were to make drastic decisions like adding a new position or closing a position. Mrs. T trusts my judgment on the day-to-day investment decisions, but I found it is always a good idea to talk to her about my investment thesis and get an agreement on big portfolio moves.< Continue Reading…