Once you achieve Financial Independence, you may choose to leave salaried employment but with decades of vibrant life ahead, it’s too soon to do nothing. The new stage of life between traditional employment and Full Retirement we call Victory Lap, or Victory Lap Retirement (also the title of a new book to be published in August 2016. You can pre-order now at VictoryLapRetirement.com). You may choose to start a business, go back to school or launch an Encore Act or Legacy Career. Perhaps you become a free agent, consultant, freelance writer or to change careers and re-enter the corporate world or government.

You must have a functional account that is easy to use to efficiently manage your retirement savings. Discover how to open a successful self-directed IRA.

Image courtesy of Logical Position

By Dan Coconate

Special to Financial Independence Hub

Many share the goal of achieving financial security in retirement, yet the path to reaching this milestone is often full of uncertainty and complexity. Learning about smart investing is one of the most effective strategies for ensuring a stable financial future.

A self-directed Individual Retirement Account (IRA) offers Americans a flexible and powerful vehicle for retirement savings, providing the opportunity to diversify your portfolio beyond traditional stocks and bonds. Learning how to open a successful self-directed IRA presents a unique advantage if you are seeking control over your retirement future. [Editor’s Note: Available in the U.S., IRAs are most comparable to Canada’s RRSPs.]

Choosing the right Custodian

The choice of custodian is vital in setting up your self-directed IRA. A custodian is an IRS-approved financial institution responsible for holding and safeguarding your IRA’s assets. Since not all custodians offer the option to invest in all asset types available to self-directed IRAs, selecting one that fits your investment strategy is essential. Custodian fees can vary widely and may include account opening fees, annual maintenance fees, transaction fees, and asset holding fees. These costs can significantly impact the overall returns on your investment, especially over the long term.

Funding your Self-Directed IRA

Funding your Self-Directed IRA is a crucial step toward building your retirement nest egg. A direct transfer from an existing IRA into your self-directed IRA is often the most straightforward method, involving minimal paperwork and no tax implications. A rollover from a 401(k) can also deposit substantial funds into your self-directed account, but it’s important to be aware of the rollover windows and potential tax consequences.

Understanding the Rules & Regulations

Understanding the rules and regulations that govern self-directed IRAs is not just a recommendation; it’s a necessity for ensuring the long-term success and compliance of your retirement savings account. This comprehension should include familiarizing yourself with prohibited self-directed IRA transactions to understand the tax implications, potential penalties, and fees of your investments. Learning these rules will ensure that you remain compliant while maximizing your IRA’s potential.

Choosing your Investments Wisely

You must choose wisely to financially prepare for retirement with the freedom to invest in multiple assets. Making informed investment decisions is one of the most crucial strategies for your self-directed IRA’s success. This decision must involve researching potential investments, understanding the market, and considering your overall retirement strategy. Strategic diversification and due diligence play key roles in achieving long-term financial growth and security. Continue Reading…

We’ve gathered the wisdom of successful entrepreneurs and financial experts to reveal their strategies for accelerating wealth accumulation. From focusing on high-leverage activities to applying the 50/30/20 budgeting rule, explore the diverse tactics shared by fifteen professionals, including founders and CEOs, on how to maximize income and expedite wealth building.

Focus on High-Leverage Activities

Diversify Your Income Streams

Live Beneath Your Means

Invest in Real Estate

Turn Passions Into Online Business

Leverage Offset Mortgages with Stoozing

Build a Collaborative Business Model

Pursue Passionate Side Hustles

Specialize in In-Demand Niches

Invest Earnings in Business Ventures

Hire a Specialized Tax Specialist

Automate Savings to Investment Transfers

Document Achievements in a Brag Book

Combine Education with Financial Investing

Apply the 50/30/20 Budgeting Rule

Focus on High-Leverage Activities

The best way to maximize your income and expedite the process of building wealth is to focus on your highest-leverage activities and outsource everything else. When you’re doing everything yourself, you can only do so much. But when you delegate as much as possible, you can focus on your core competencies and grow your business faster. This is something I’ve learned the hard way. In the past, I used to do everything myself.

But as my business grew, I realized that I was spreading myself too thin. So instead of trying to do everything, I hired people to do the things I didn’t enjoy or wasn’t good at. This allowed me to focus on my strengths and grow my business faster. For example, I used to spend a lot of time writing blog posts and creating content. But now I have a team of writers who do that for me. This has freed up a lot of my time and allowed me to focus on marketing and growing my business. — Matthew Ramirez, Founder, Rephrasely

Diversify your Income Streams

One effective approach I’ve used and recommend is diversifying your income streams. By expanding your sources of income beyond a single stream, you can create a more stable and potentially higher-earning financial foundation. Explore avenues such as investing in stocks, real estate, or offering freelance services.

One way I diversified my income streams was through investing in stocks. I researched and identified companies with strong growth potential and invested a portion of my savings in their stocks. Over time, as the companies performed well and their stock prices increased, I earned capital gains and dividends.

This additional income from my investments complemented my primary source of income and contributed to building wealth. By regularly monitoring the market and making informed investment decisions, I was able to maximize my earnings and accelerate my financial goals. — Sacha Ferrandi, Founder & Principal, Source Capital

Live Beneath your Means

Eschew lifestyle creep, which can hamper you from building wealth. Instead, live beneath your means by comparison shopping, creating and sticking to a budget, and funneling savings, raises, and additional monies received into an emergency fund, savings vehicles, and investments.

For example, comparison shopping for your auto and home insurance can save you hundreds of dollars a year. The same goes for negotiating interest rates with credit card companies and rates for other services. Instead of spending that extra money, boost your savings account or open a CD account.

If your employer offers a 401(k) plan, build your wealth by increasing your contribution to it whenever you receive a raise. Be sure to take advantage of the maximum amount if your employer offers a 401(k) match. — Michelle Robbins, Licensed Insurance Agent, Clearsurance.com

Invest in Real Estate

Making real estate investments became my cornerstone strategy for building substantial wealth. Strategically acquiring properties in prime locations and astutely capitalizing on market trends paved the way for a transformative financial journey. Through shrewd decision-making, I cultivated a stream of passive income from rental properties and witnessed significant appreciation in property values over time. The enduring nature of real estate investments proved to be a resilient and effective avenue for wealth accumulation.

By leveraging the power of property ownership, I secured a reliable income source and tapped into the wealth-building potential inherent in real estate. This strategic approach allowed me to navigate the complexities of the real estate market, aligning my investments with long-term growth prospects and contributing significantly to the acceleration of my overall wealth-building objectives. — Bill Lyons, CEO, Griffin Funding

Turn Passions into Online Business

I developed my personal finance site into a thriving business that has been instrumental in helping me build wealth. After paying off my student loans, I launched the site to help other millennials manage money by sharing the frugal tips and repayment strategies that worked for me.

Years later, My Millennial Guide now earns steady revenue through affiliate partnerships and digital consumer banking offers relevant to my audience. I’ve built a sizable audience by providing quality and engaging money advice for free.

My own journey to financial freedom after conquering student loan debt has proven firsthand how lucrative launching an online business around your passions can be. The flexible income from My Millennial Guide provided the runway to leave my corporate job and focus full-time on site growth.

Now, rather than relying on a single income source, multiple automated revenue streams from this one company allow me to maximize earnings while making an impact by sharing financial advice. The wealth-building opportunities entrepreneurship provides are limitless.

I’m proud that the free resources and recommendations I’ve shared on My Millennial Guide have empowered thousands toward financial freedom, while also securing my own prosperous future. Turning my purpose into a business became the ultimate wealth vehicle. — Brian Meiggs, Founder, My Millennial Guide

Leverage Offset Mortgages with Stoozing

A pivotal strategy in my journey to Financial Independence was leveraging an offset mortgage with ‘Stoozing.’ This method, while requiring discipline, has the potential to drastically lower mortgage payments and accelerate wealth accumulation. Taking advantage of 0% interest credit card offers, I redirected these funds into an account linked to my mortgage. This not only reduced the mortgage balance but also minimized interest expenses significantly.

The essence of Stoozing lies in its ability to turn credit into a tool for savings. With over $100,000 deposited from credit cards, my mortgage interest payments plummeted. This approach demands meticulous management to clear the credit card balance before the 0% interest period expires. By doing so, I could fast-track my path to financial freedom by a decade, demonstrating the power of innovative financial strategies in wealth building. — Shane McEvoy, MD, Flycast Media

Build a Collaborative Business Model

To make more money and get rich faster in the legal field, it makes sense to encourage cooperation and build a group law firm instead of a solo practice. Lawyers with different types of skills can work together in collaborative law firms. Because they have different skills, their members provide a range of legal services.

Collaboration allows firms to offer more services, which speeds up growth. When the team is more diverse, the firm can assist more clients and handle more complex legal cases. Working together can bring in more money and help individuals get rich faster. Help desk workers and lawyers share computers, filing cabinets, and office space in a collaborative law firm.

By using the same resources, firms may be able to reduce costs and operate more efficiently. Collaborative lawyers can retain more of their earnings by cutting down on individual expenses. You can get rich faster and make money through smart investments if you know how to manage your finances well. Lawyers can become leaders in their field by focusing on their expertise if they work together. People with specific legal needs should choose this firm because it specializes in those areas of law. Dominating a niche might enhance your legal reputation. Wealthy individuals are drawn to the firm because it has a large market and charges a premium for its specialized services.

Collaborative law firms can showcase their array of services and lawyers’ expertise by representing themselves as a one-stop shop for all your legal needs. This branding strategy makes the firm stand out in the competitive legal market. Effective branding positions the company as an authority, which attracts more clients. As more clients and business opportunities arrive, you make more money and build your wealth. — Martin Gasparian, Attorney and Owner, Maison Law

Pursue Passionate Side Hustles

What I have learned is that as you grow in your career and acquire new skills, this will help you to think about other avenues to travel to bolster your income. Take, for instance, I always wanted to be an adjunct professor, but it was a true process. It did not happen overnight. It took time. We can’t rush the process because once we get there in a hurry, then we can’t stay there. The goal is to get there and have the foundation to remain. Continue Reading…

The National Institute of Ageing is today releasing the next instalment [“the final Step 1”] of its series of papers on the Canada Pension Plan (CPP/QPP) and the Canadian retirement income system. The link invites readers to click on a download button for a full PDF of the report.

Recall that Findependence Hub’s introductory blog on this was published on April 11th here, and subsequently in my Retired Money column at MoneySense.ca on April 23: How to double your CPP Income. It also summarized in this second Hub blog on April 24th.

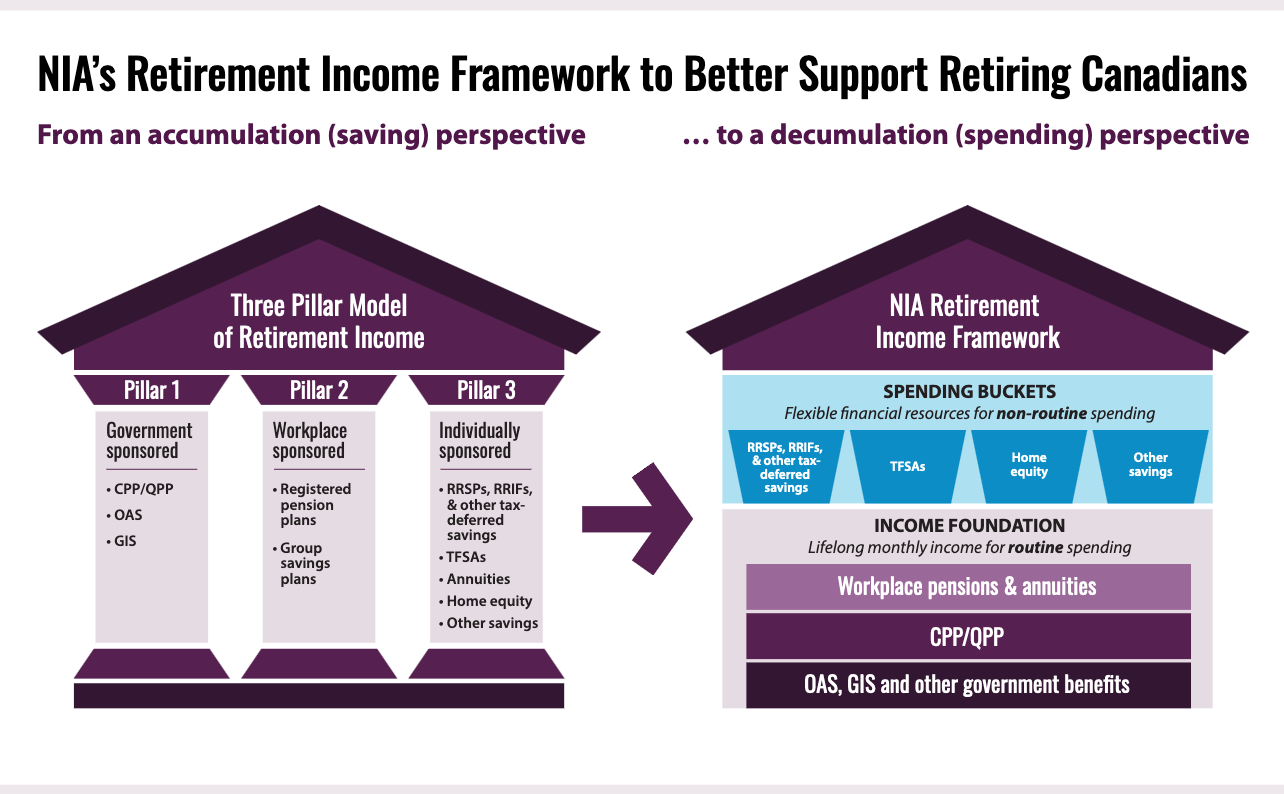

Below is a screenshot from the new paper: my comments follow below the graphic, which the NIA defines as a “redefined visual of the Canadian retirement income system.”

Recall that the entire series of papers is titled 7 Steps Toward Better CPP/QPP Claiming Decisions: Shifting the paradigm on how we help Canadians. Step #1 is titled (Re)Introducing the RetirementIncome System: A New Framework Tailored to the Retiree’s Perspective.

The accompanying text includes this overview:

“Canada’s retirement income system has traditionally been presented to the public as three pillars, consisting of government-sponsored retirement income programs (CPP/ QPP, OAS and GIS), workplace pension plans and personal savings. However, this traditional framing is a missed opportunity to help workers mentally transition into retirement, encouraging them to shift their attention toward the adequacy of their financial resources to successfully and sustainably finance their entire retirement.”

The paper goes on to point out that here is some irony involved in how the traditional “three pillar” framework of the retirement income system is presented: it does so from the perspective of providers (i.e., government, employers and the financial services industry), rather than those it is intended to inform.

“When viewed from the end user’s perspective, pensions are not a financial pillar of the retirement income system. They are the income foundation on which other financial resources rest.”

By viewing pensions as “a foundation rather than a pillar,” the NIA continues, “the resulting framework provides a structure that is more focused on spending, with an ‘income’ foundation that securely and sustainably replaces employment income. Private assets accumulated on an individual or collective basis — including tax-deferred savings such as registered retirement savings plans (RRSPs), registered retirement income funds (RRIFs), and defined contribution (DC) pension plans — are ‘spending buckets’ on top of this foundation, providing flexibility to support non-routine spending throughout different retirement stages.” Continue Reading…

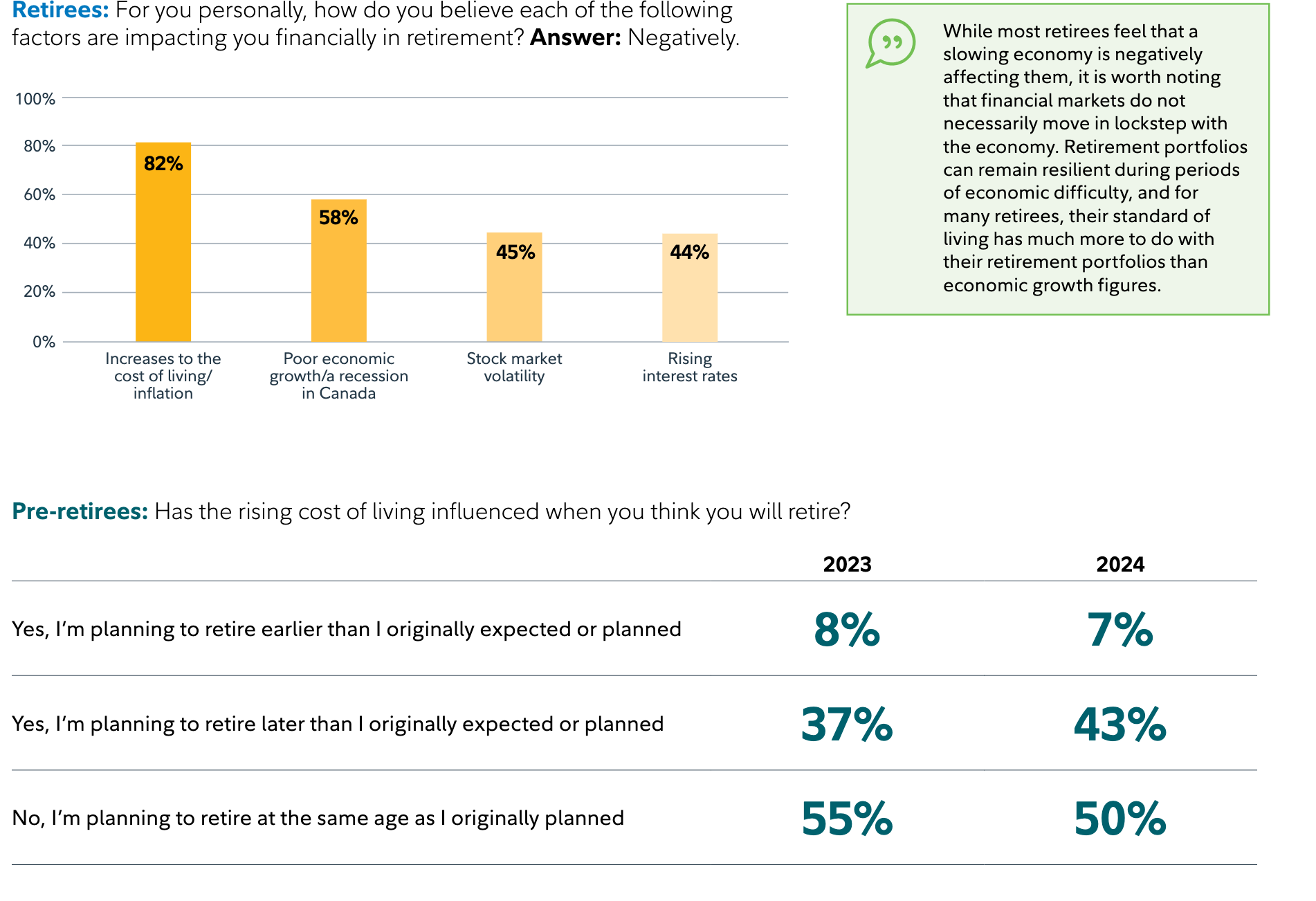

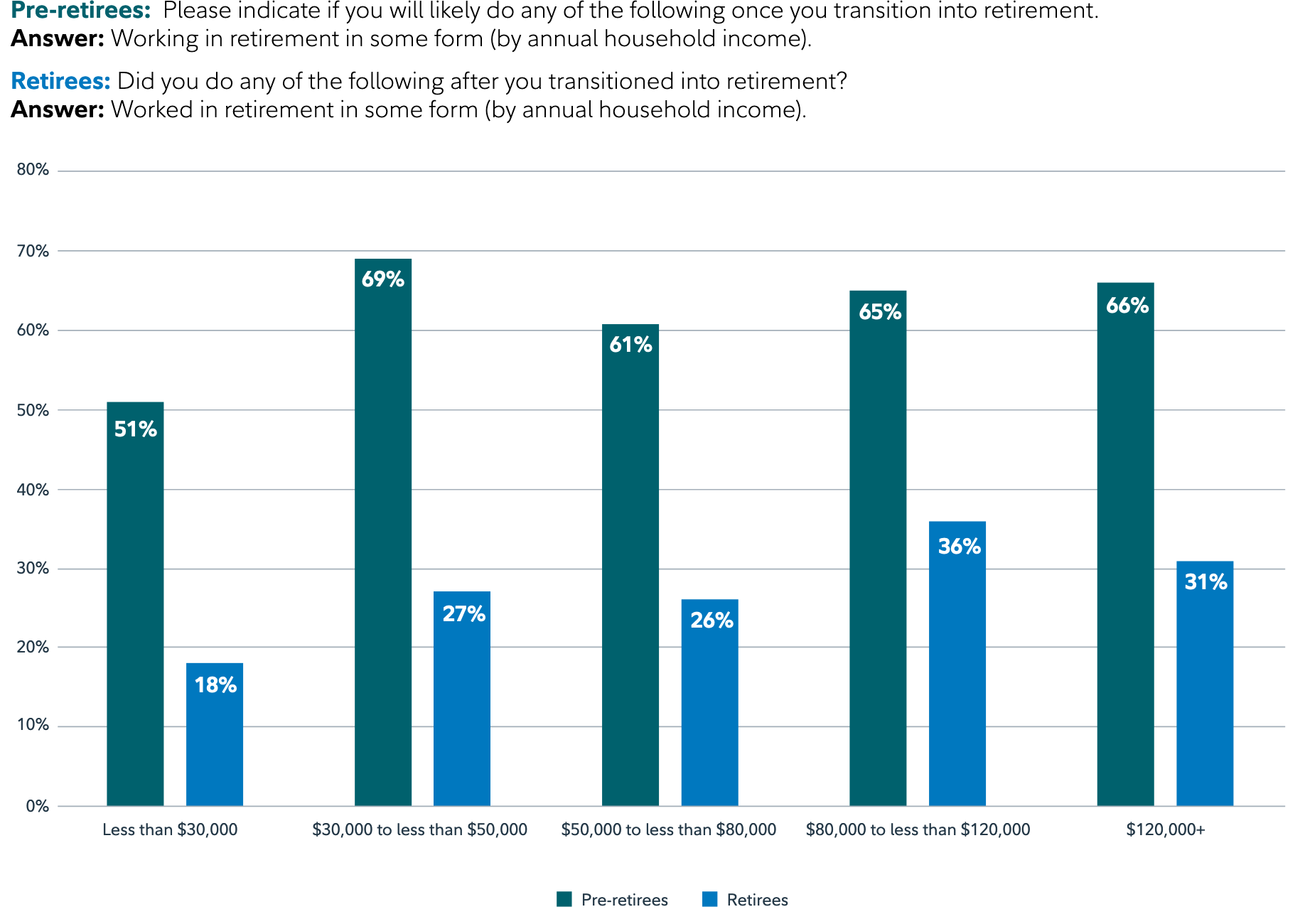

More than four in five (82%) Canadian retirees say inflation is having a negative financial impact on them in retirement, according to a just-released report from Fidelity Investments Canada ULC.

The 2024 Fidelity Retirement Report also found that 43% of pre-retirees say the rising cost of living is delaying when they think they will retire. In addition, 59% of retirees report helping their non-student adult children in retirement: both with day-to-day expenses as well as big-ticket items like home purchases, weddings and even education savings for their grandchildren.

“It comes as no surprise that retirees are feeling the bite of inflation. Other macroeconomic issues such as a slowing economy, rising rates and volatile markets are also common factors that have negatively affected retirees financially,” says the report, “Pre-retirees are also feeling the pinch. We find that compared with last year, a larger share of pre-retirees are considering delaying their retirement in response to the rising cost of living.”

As you can see from the graphic below, the percentage of pre-retirees who plan to retire later than originally expected rose from 37% in the 2023 survey to 47% in the new 2024 edition.

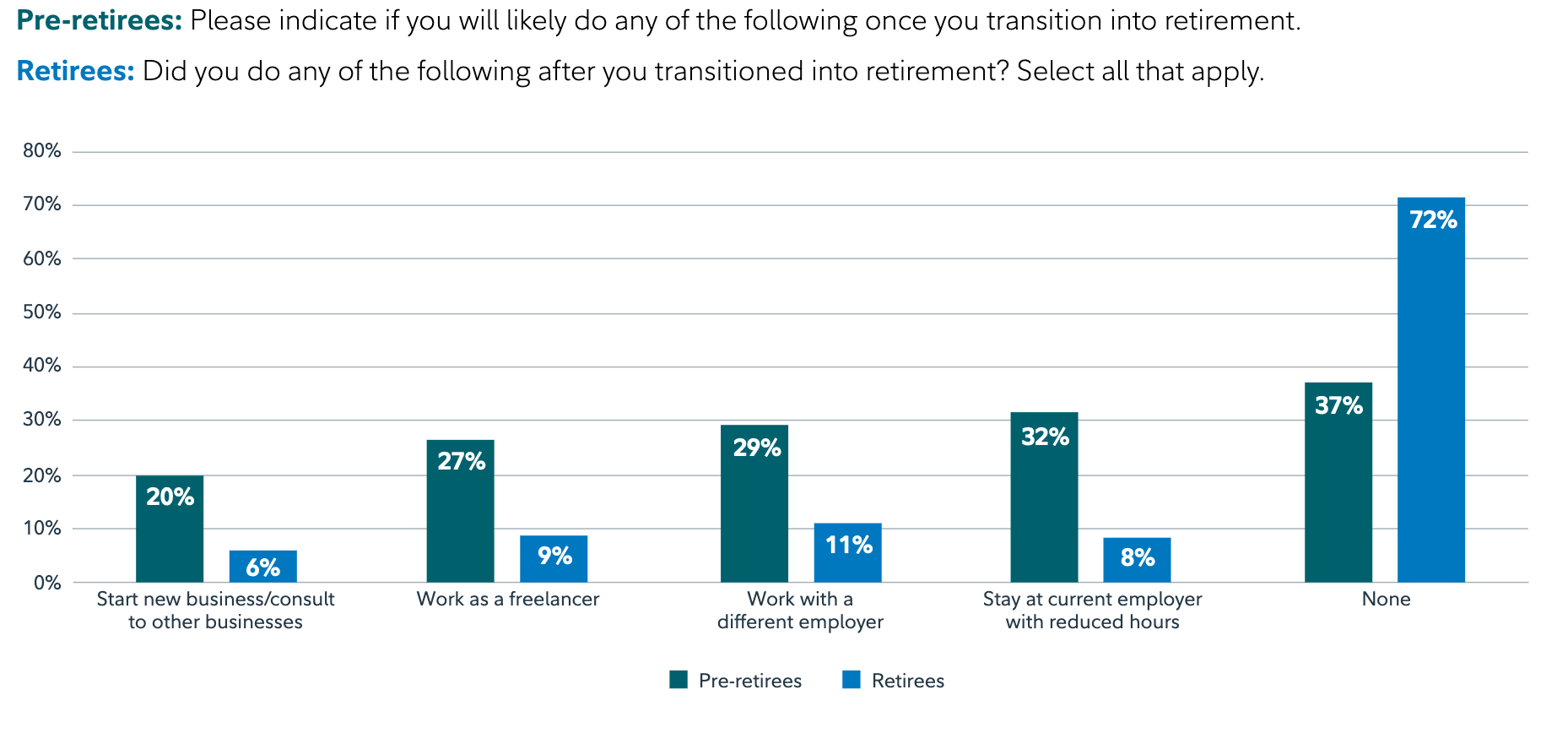

While less than a third of those already in retirement have worked in some capacity once they have left full-time work, most pre-retirees anticipate that they will work at least part-time once they’re retired, according to the report.

While Fidelity cites rising inflation as one reason for this trend, it also says “most pre-retirees would like extra money for recreational purposes.” Further, the report says, “We also find that there isn’t a clear relationship between those working in retirement and their level of household income, suggesting that in general, many Canadians may be working or anticipating working to maintain a higher material standard of living, rather than just to keep up with the rising cost of essentials.”

Many dream of retirement, but as the big day approaches, some experience a surprising emotion: fear. Billy and Akaisha Kaderli, your guides to navigating retirement, delve into the anxieties that can lurk beneath the surface of financial preparedness.

RetireEarlyLifestyle.com/iStock

By Billy and Akaisha Kaderli

Special to Financial Independence Hub

All of your ducks are in a row.

You have saved and carefully invested for years, and the personal discipline is about to pay off.

So why is there apprehension in the bottom of your belly? Let’s be honest. There is risk involved, and the future no longer seems certain or familiar.

“What if I forgot about something?” you think, and start going over every plan you have made.

No one likes to admit straight out that they are afraid of retirement. Why, that sounds silly. But changing your life from one of being focused on work duties, raising a family, paying bills, and receiving that dependable paycheck every week to one of the virtually unknown has its own set of stresses. You’re being dishonest if you say it’s not a big leap mentally, emotionally, or financially.

Lack of confidence often underlies questions disguised as logistics on how to retire. Sometimes, one must simply take the leap of faith, making a companion of the ever-present question “What if?”

If you have spent your whole life building security and providing that same security the best you could for your family, then stepping into the unknown world of retirement is like jumping off a cliff.

Even if you’re as prepared as you think you are.

Sure, we can distract ourselves with dreams of endless golf, or margaritas on an exotic beach somewhere, but when it’s quiet, we find ourselves looking over our shoulders, wondering whether some forgotten component is lurking just out of sight.

“What if I run out of money?,” you whisper to yourself.

Perhaps your personal fear-mongering nemesis is health care in retirement, your portfolio balance or even something as simple as boredom. There can be great comfort gained from all of one’s time being planned out months in advance.

Going sailing, Boracay, Philippine Islands

To expect retirement to be free of hitches or snags is unreasonable. There are no guarantees in life. None of us knows what the future will bring, and this is true whether you’re working or retired. Continue Reading…