Of the major North American cities that feel most like Toronto, Chicago is clearly the closest fit. It’s Toronto’s sister. Chicago is the third most-populous city in the U.S., behind New York and Los Angeles. According to the U.S. Census Bureau, Chicago proper has a population of 2.7 million, almost exactly the same amount as Toronto.1 Both cities have several million more living in the immediate suburbs. Chicago’s money resides mostly on one side of the city, with most of its poverty found on the city’s south and west sides. Wealthy suburbs span almost to Wisconsin in the city’s “North Shore” suburbs, which consist of some of the wealthiest zip codes in the U.S.

Like Toronto, Chicago is a money centre. It is widely considered to be in that tier of financial hubs that includes Boston and San Francisco, behind the center of it all in New York. Its construction is dense; people take trains and buses to commute into the downtown core. Critically, as far as desirability of property goes, Chicago’s weather is miserable, just like Toronto’s. The two cities are also characterized by left-leaning politics, so there isn’t much of a difference on that front either.

When we engage Torontonians about the U.S. and Chicagoans about Canada, time and again the answer comes back: the city that is most like Toronto is Chicago.

Except in one way.

Chicago homes are one third or half of similar homes in Toronto

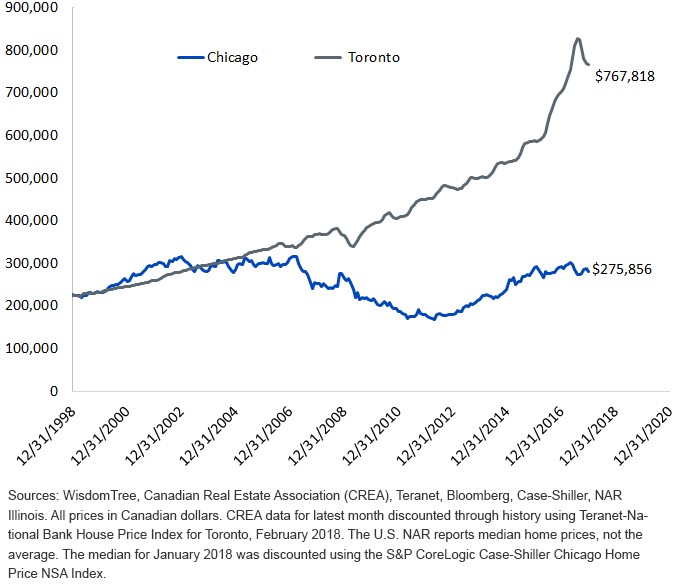

There is a major arbitrage just sitting there for anyone who liquidates Toronto property, hops on a 75-minute flight and purchases a mirror-image property for one-third or half the price in Chicago. Yes, Chicago is riddled with violence, but not in the neighbourhoods where someone would spend C$767,818, the average Toronto home price in February.2 In those neighbourhoods, the biggest risk is having a $500 stroller run over your toe.

Just what could C$767,818 get in Chicago?

According to the National Association of Realtors’ (NAR) Illinois chapter:

In the nine-county Chicago Primary Metropolitan Statistical Area (PMSA), home sales (single-family and condominiums) in January 2018 totaled 5,777 homes sold, down 8.0 percent from January 2017 sales of 6,277 homes. The median price in January 2018 was $224,000 in the Chicago PMSA, an increase of 7.2 percent from $209,000 in January 2017.

Converting US$224,000 to Canadian dollars at the January exchange rate of $1.231, that is C$275,856 for the median house in Chicago. Granted, U.S. housing data tends to be measured by the median, whereas the Canadian norm is to take the average, but there is still not much of a comparison; the gap is yawning, and this all started happening only in recent years. Continue Reading…