Most of your investing life you and your adviser (if you have one) are focused on wealth accumulation. But, we tend to forget, eventually the whole idea of this long process of delayed gratification is to actually spend this money! That’s decumulation as opposed to wealth accumulation. This stage may also involve downsizing from larger homes to smaller ones or condos, moving to the country or otherwise simplifying your life and jettisoning possessions that may tie you down.

On October 19 Fortune published an article with the headline:

“30 Years after Black Monday, the Dow Hits an All-Time High”.

The article goes on to speculate:

“only time will tell if we have another crash ahead of us. But in the meantime, investors seem to think that skepticism and caution may be just what we need to avoid one.”

Connecting the all-time high to the Black Monday crash from over 30 years ago smacks of the kind of fear-driven nonsense that characterizes much of financial markets journalism these days. The article raises the temperature further by pointing out that:

“this marks the fourth thousand-point milestone for the Dow this year, painting a very different picture than what was seen in 1987. According to the Wall Street Journal, the Dow had never before hit more than two of these milestones in a year.”

Transforming meaningless data points into blood-pressure-raising insights is a coveted skill for both market journalists and stock market analysts alike. After all it’s their jobs to get people to act: stock analysts to compel trades, journalists to direct readers/viewers to the skilled money managers that advertise in their pages or on their programs.

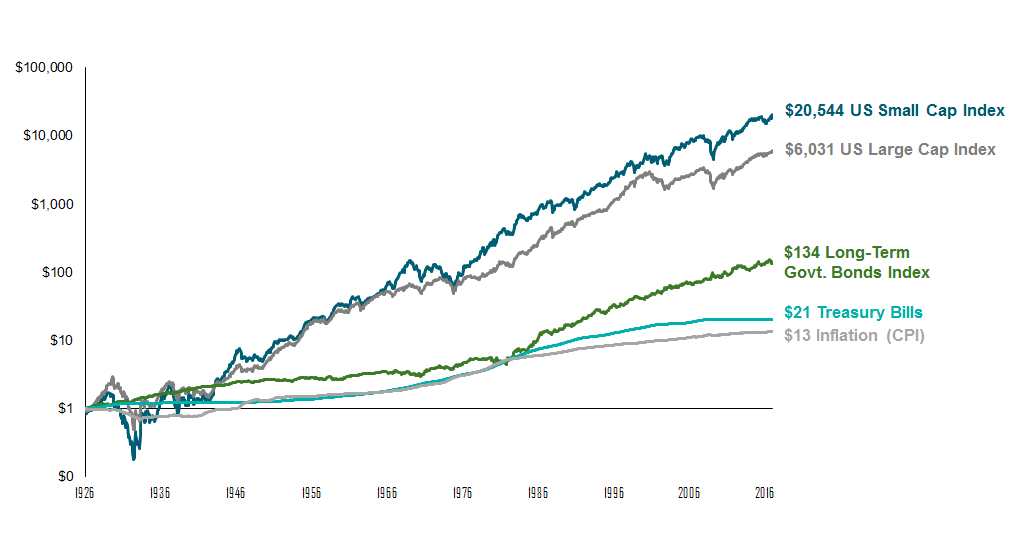

I’d be a poor headline writer. The first one I came up with, “Dow Hits an All-Time High more than 500 Times Since 1987 Crash” wouldn’t inspire much fear or anything else. The fact is that markets go up most of the time as is clearly displayed in the index data series shown at the top of this blog, courtesy of Dimensional Fund Advisors. Continue Reading…

The piece is based on a half-day conference held in Toronto on Wednesday sponsored by Franklin Templeton Investments. The third annual Retirement Innovation Summit was an equal mix of sessions on Retirement readiness and updates by Franklin Templeton executives on the current state of the markets.

The big theme was the well-established (two decades now) shift from the guaranteed-for-life Defined Benefit pensions earlier generations enjoyed, to market-variable alternatives like Defined Contribution pensions. As a result, longevity risk and market risk has been gradually shifting from the shoulders of employers to those of their workers/employees. And that in turn has meant that would-be retirees have to devote a lot more attention to the markets and investing than older generations that enjoyed what seems in retrospect to be a “golden age” of retirement income security.

Retirement is a gradual process, not a cliff

As for Retirement Readiness, one speaker described how Retirement itself has become more tentative. Instead of moving abruptly from 100% work mode to 100% leisure the moment you reach the traditional retirement age of 65, workers are experimenting with retirement and more often than not returning to the workforce, only to rinse and repeat.

Since the US financial crisis, the numbers of people aged 65 or more who are still working full-time has been on the rise. Of those still working after 65, only one in five did so because they felt they had to because of shaky personal finances. For the other four in five, it’s “because they want to or truth to tell, their spouse wants them out of the house,” the speaker said.

Furthermore, among both full- and part-time workers in that age category, 40% reported they had retired twice already: they had quit the working world, returned a few months or years later, then quit again and then returned to work again.”

Taking a Retirement Victory Lap

So much for the so-called “Retirement Cliff.” This of course is a major theme of the book I co-authored with Mike Drak: Victory Lap Retirement. We basically argue that retirement is a long process that involves slowly moving into. After all, you never see an airplane land by suddenly putting on the brakes in mid-air and dropping vertically: there is a gradual “glide path” to a smooth landing.

So it is with Retirement in our view: call it Semi-Retirement or an encore career or a legacy career but in essence it’s about moving gradually over five or ten years from 100% full-time work to perhaps 80%, 50%, 30% and so on, so that by the time you’re fully retired (perhaps in your 70s), the shock to your system is much less severe.

A home equity line of credit (HELOC) is a convenient way to access the value in your home. You might have seen commercials on TV or been offered one by your mortgage agent. Not only can you get a much lower interest rate than you can with an unsecured line of credit, you can also be approved for a sizeable loan. It’s tempting to have quick access to a lot of money, but is a HELOC right for you?

A HELOC is a secured line of credit that uses your home as security. As with a mortgage, the money you borrow is secured by your home. In Canada, as long as you can show that you can carry the debt, you can borrow up to 65% of the value of your home, provided you keep at least 20% of the value as equity.

For example, if your home is worth $1 million and you owe $400,000 on your mortgage, you can borrow up to $400,000 against your home ($1 million x 80% = $800,000 – $400,000 owing = $400,000).

There are many upsides to getting a HELOC. Depending on the value of your home, you can potentially borrow a large amount of money. Interest rates on HELOCs are significantly lower than on unsecured lines of credit (typically about prime + 0.5%). You can take out money or repay it at any time without penalty. And you can go up to 25 years before you have to pay back what you’ve borrowed.

One of the most appealing HELOC features is that the minimum monthly payment is just the interest that’s accrued. Using a HELOC calculator on that $400,000 line of credit example above, the monthly payment at today’s best HELOC rate of 3.7% is just $1,233. The minimum monthly payment on a traditional line of credit is typically 2% of the outstanding balance: $8,000 on a $400,000 balance. Even a traditional mortgage would require a much higher monthly payment. This feature alone is a big part of why HELOCs are so appealing.

Possible downsides of HELOCs

However, HELOCs also have their downsides.

Because the minimum monthly payment on a HELOC is just the interest, it can feel like it doesn’t cost you much to borrow money. But when you don’t repay the principal, your costs over the long run are actually much higher than with a traditional loan.

Let’s look at an example comparing a regular $50,000 loan with a rate of 4.7% repaid monthly against borrowing $50,000 at 3.7% from your HELOC repaid in a lump sum at the end the loan term.

If you pay the loan over five years, your monthly payment will be $936.83 and you’ll pay $6,209.80 in interest over that time.

Through their financial advisers, easy-to-use online dashboard and financial tools, they are making investing more accessible for Canadians from coast to coast.

Jon Chevreau

Jon Chevreau: Welcome, Tea. While many so-called robo-advisers seem to focus on young people building wealth, what about the end game? How do you handle the shift for older investors from accumulation into spending your savings in retirement?

Tea Nicola: Once a client who is accumulating assets decides that retirement is on the horizon and they let us know, we lead them into the retirement transition process. At this stage, they probably have a pretty good idea as to what they would like to spend after taxes. Their goal is to understand now if their savings and all their sources of income will be enough to fund their retirement years.

The conventional wisdom is to collect all the sources of income that the client will have and analyze it year by year. This step is essential to make sure that the goals are met. That includes the monthly cash flow for basic expenses, the annual travel budgets and one-off purchases as well as any legacies that they may desire.

We then make sure their savings can meet all those goals. If there are shortfalls, we adjust the savings rate to meet the goals by the time they want to stop working. Then, we iterate this every six months or so, both before and after the retirement date. We do this to make sure the transition is smooth and that routines are appropriately established.

Jon: You’re talking about managing expectations?

Tea: I would call it being realistic about expectations. For instance, we need to be careful about talking about a monthly income when it comes to drawing down on retirement savings.

What we typically see is an uneven drawdown, with extra spending in the first few years of retirement. The client is in a rush to do all the things they held off on while working. So, they go on world tour, get a golf membership, enjoy some fine dining, or generally treat themselves to something special. But after a few years, their spending habits ‘normalize.’ The initial exuberance declines and their expenses follow suit. You get cases like one client in her 90s, who is literally worth millions, who now has monthly expenses of about $2,000 a month.

With that in mind, our financial plans help clients to achieve the goals they want to achieve, without necessarily boxing them into a lifestyle category that doesn’t really apply for most of their retirement. This involves very realistic, practical planning that I would say goes into a bit more depth than other robo-advisers, or even many traditional wealth management firms.

Jon: Sometimes you’ll hear a kind of magic number bandied about for how much people need to retire. $1 million. $2 million … Is there a guideline that really makes sense?

Tea: It depends on the person, which is why financial planning needs to be tailored for each individual. Just like with salaries, we know that someone making $75,000 can feel like they’ve got as much money as they could possibly need. Continue Reading…

My latest MoneySense Retired Money column looks at the fate of members of the Sears Canada pension plans (DB and DC). You can find it by clicking on the highlighted headline here: What Sears retirees can do about the reduced DB pension.

While the focus is not per se on the demise of Sears Canada itself, and the loss of thousands of jobs, I refer readers to an excellent article by the Globe & Mail’s Marina Strauss (it may only be available to subscribers): Who Killed Sears Canada?

Not only will many retirees get an estimated 19% haircut on their promised pensions, but thousands of workers have lost their jobs without severance, and lost health and dental benefits. My MoneySense column reiterates that Ontario members of the Sears DB pension will be better off than Sears retirees in the other provinces, because of the Pension Benefits Guarantee Fund in Ontario, which we looked at a few columns back. Roughly half of Sears employees and retirees live outside Ontario.

Should workers take Commuted Value?

One of the questions before Sears retirees is whether to take the Commuted Value of the pension, if and when that option is offered, or to sit tight and wait for the promised pension benefits, even if they are — as expected — roughly 19% lower than they should have been. (The plan is roughly 81% funded.) Continue Reading…

On October 19 Fortune published an article with the headline:

On October 19 Fortune published an article with the headline: