Most of your investing life you and your adviser (if you have one) are focused on wealth accumulation. But, we tend to forget, eventually the whole idea of this long process of delayed gratification is to actually spend this money! That’s decumulation as opposed to wealth accumulation. This stage may also involve downsizing from larger homes to smaller ones or condos, moving to the country or otherwise simplifying your life and jettisoning possessions that may tie you down.

Even before the Tariffs threats emerged under Trump 2.0, Canadian seniors were starting to find the economic uncertainty and rising living costs to be unmanageable. No surprise then that many seniors approaching Retirement Age are delaying their exit from the workforce.

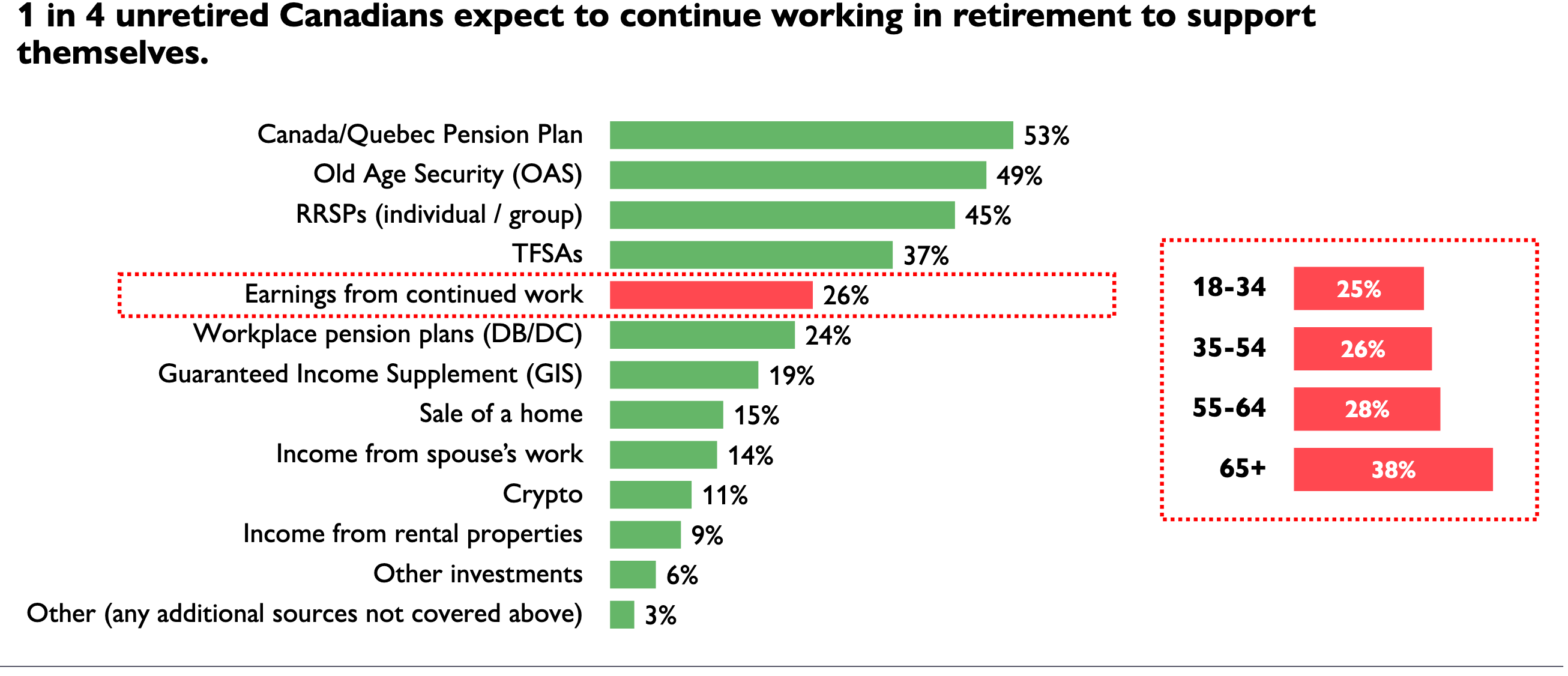

According to a report by HealthCare of Ontario Pension Plan, 28% of unretired Canadians aged 55-64 say they expect to continue working in retirement to support themselves financially. Here’s a screenshot from the HOOPP survey:

The Healthcare of Ontario Pension Plan (HOOPP) commissioned Abacus Data to conduct its sixth annual Canadian Retirement Survey in the spring of 2024. The latest survey finds “persistent high interest rates and a rising cost of living continue to have a significant negative impact on Canadians’ ability to save and manage the cost of daily life, threatening their retirement preparedness.” While all Canadians are struggling, “women and those closest to retirement are especially hard hit with lower savings and higher levels of financial stress.”

While most Canadians are struggling to save amidst a high cost of living, HOOPP finds women are particularly affected. Half (49%) of all Canadian women have less than $5,000 in savings and almost a third (28%) have no savings (compared to 33% and 17% of men, respectively), similar to the 2023 results

The MoneySense column also looks at more recent Retirement surveys that also reveal anxiety about rising costs of living. One is from Bloom Finance Co. Ltd., conducted by founder Ben McCabe after Trump’s Tariffs started to kick in this year.

A Bloom study conducted with Angus Reid found 46% of Canadians thinking of working part-time in Retirement. That’s in line with a Fidelity survey in 2024 that found half of Canadians plan to delay Retirement. According to the Bloom Report [in March 2024], 67% of Canadian homeowners over 55 were concerned their savings would not sustain their quality of life through retirement. Only 29% considered downsizing or alternative living situations to access their home equity earlier than expected. 59% of the same cohort agreed accessing micro-amounts of their home’s equity would help maintain their desired living standard. Continue Reading…

To apply this approach, at the end of each year, you pick the 10 stocks with the highest dividend yields from the 30 stocks that make up the Dow index.

You then invest an equal dollar amount in each of these 10 stocks and hold them for one year. You repeat the selection process and re-jig the portfolio at each year-end.

In theory, these stocks should outperform the market (the DJIA or the S&P 500).

2. The Small Dogs of the Dow Approach

In another variation, you pick the 10 highest dividend-yielding stocks, then select the five with the lowest stock price. Invest an equal dollar amount in each of those, hold them for a year, and repeat. This variation is known as the Small Dogs of the Dow, or simply The Dow 5.

Here’s a Dogs-of-the-Dow ETF

The ALPS Sector Dividend Dogs ETF (symbol SDOG on New York) follows its own version of the Dogs-of-the-Dow strategy. It picks five stocks with the highest dividend yields from each of the 10 sectors of the S&P 500 index. These sectors are consumer discretionary, consumer staples, energy, financials, health care, industrials, information technology, materials, telecommunication services, and utilities.

Each holding begins with roughly the same dollar value, so every company starts out with a similar influence on the ETF’s total return. The end result is a portfolio of 50 large-cap stocks.

Currently, the fund now holds a number of stocks we recommend as buys for subscribers of our Wall Street Stock Forecaster advisory. They include AT&T, Verizon, Kraft Heinz, Snap On, 3M, Newmont Mining and IBM. However, the ETF also holds a lot of stocks we don’t recommend.

Should you Follow the Dogs of the Dow Approach?

One best-selling book of the early 1990s advised investors to buy the Dogs of the Dow: the lowest-priced, highest-yielding Dow stocks. Followers of the approach made money. Of course, anybody who bought stocks in the early 1990s made money.

The Dogs of the Dow strategy worked well in the 1990s because interest rates were going down. This tended to raise all stock prices. But high-yielding stocks were affected more than most because they attracted bond investors who were switching into stocks.

That’s how things work with most formulaic approaches: Sometimes they seem to add value, because they happen to lead you to invest in stocks that were likely to go up for some reason other than the formula’s actual focus.

Of course, you also need to keep in mind that high yields can signal danger, rather than a bargain.

All in all, we don’t recommend the Dogs of the Dow strategy.

Here’s why high yields can be a danger sign

To reiterate: a high dividend yield may be a danger sign. It may mean insiders are selling and pushing the price down. A falling share price makes a stock’s yield goes up (because you still use the latest dividend payment as the numerator to calculate yield: but the denominator, the price, has dropped). But when a stock does cut or halt its dividend, its yield collapses. Continue Reading…

The utility sector is known for its defensive qualities, providing a stable investment option in times of market uncertainty. By overweighting defensive sectors, investors can lower the volatility (risk) of their portfolios. Many will refer to Canadian utilities as ‘bond proxies’ due to their steadiness. However, the true strength lies not in the dividends they offer but in the inherent defensive nature of these companies. Utility stocks are considered defensive because they tend to perform well during economic downturns. Consumers continue to need electricity, water, and other essential services even when the economy is struggling. So here we’ll take a look at Canadian utility stocks and ETFs.

There are a few reasons for an investor to embrace the utilities sector. They may want a portfolio that is less volatile. A retiree can witness a real financial benefit as a portfolio that experiences lesser drawdowns in recessions can create greater and more durable income over time.

Defensive sectors

In this post, the Defensive sectors for Retirement, the three defensive sectors were almost twice as good as a traditional balanced stock and bond portfolio. That is to say, the portfolio moved through the financial crisis of 2008-2009 and left the retiree with a portfolio almost twice as large as the traditional 60/40 balanced portfolio.

Keep in mind past performance does not guarantee future returns. That said, consumer staples, utilities and healthcare have a long history of offering greater portfolio stability.

Canadian utility stocks and ETFs

That above posts looks to U.S. staples, utilities and healthcare stocks. There’s no better place to find multinational consumer staples and healthcare stocks. The healthcare sector is non-existent in Canada. Our consumer staples sector in Canada (XST.TO) is very good, but is mostly domestic. More on that later.

In the Globe & Mail Rob Carrick offered an article (sub required) on Canadian utility ETFs. Rob noted that the fees for these ETFs are quite large compared to market index-based ETFs. The fees are in the 0.32% to 0.61% range. That said, that is the norm for ‘specialty’ or sector ETFs. Rob looked at three Canadian utility ETFs …

The two high-fee funds are the BMO Equal Weight Utilities Index ETF ( ZUT-T), with assets of $500-million and 14 total holdings; and the iShares S&P/TSX Capped Utilities Index ETF ( XUT-T) with assets of $379-million and 15 holdings.

A third fund, the Global X Canadian Utility Services High Dividend Index ETF ( UTIL-T) will on March 4 reduce its current MER of 0.61 per cent to an estimated 0.32 per cent. UTIL has assets of $379-million and 15 holdings.

Core utilities or extended universe?

One key decision that an investor will make is: what types of utilities do you want to own? You can stick to the traditional power/electricity producers, or you can include pipelines and the modern utilities known as the telcos.

ZUT.TO and XUT.TO are traditional power utilities. They are very similar, except the BMO ZUT is equal-weighted while the iShares XUT is cap-weighted (the largest companies get the greater weighting within the index). I’d give the edge to the BMO ETF. Continue Reading…

There is a basic principle that most people follow when it comes to their spending decisions. In essence, people generally try to either

(1) Get the most they can for the least amount of money, or

(2) Spend the least amount of money on the things they want (i.e. get the best deal)

In other words, rational utility maximizers try to be as efficient as possible when parting with their hard-earned dollars.

Strangely, many investors abandon this principle when it comes to their portfolios. With investing, what you get is return (hopefully more than less), and what you pay (other than fees) is risk. People often focus on return without any regard for the amount of risk they are taking. Alternately, many make the mistake of reducing risk at any cost, regardless of the magnitude of potential returns they leave on the table.

The foundation of successful investing necessitates achieving an optimal balance between return and risk. Different types of assets (volatile speculative stocks, stable dividend paying stocks, bonds, etc.) have very different risk and return characteristics. Relatedly, a portfolio’s level of exposure to different asset classes is the primary determinant of its risk and return profile, including how efficient the balance is between the two.

Offense, Defense, & Bobby Knight

Robert Montgomery “Bobby” Knight was an American men’s college basketball coach. Nicknamed “the General,”h e won 902 NCAA Division I men’s basketball games, a record at the time of his retirement. He is quoted as saying:

“As coaches we talk about two things: offense and defense. There is a third phase we neglect, which is more important. It’s conversion from offense to defense and defense to offense.”

Nobody can escape the fact that you can’t have your cake and eat it too. You can’t increase potential returns without taking greater risk. Similarly, you can’t reduce the possibility of losses without reducing the potential for returns.

Picking up Pennies in Front of a Steamroller vs. Shooting Fish in a Barrel

Notwithstanding this unfortunate tradeoff, there are times when investors should focus heavily on return on capital (i.e. being more aggressive), times when they should be more concerned with return of capital (i.e. being more defensive), and all points in between.

Sometimes, there is significantly more downside than upside from taking risk. Although it is still possible to reap decent returns in such environments, the odds aren’t in your favour. Reaching further out on the risk curve in such regimes is akin to picking up pennies in front of a steamroller: the potential rewards are small relative to the possible consequences. At the other end of the spectrum, there are environments in which the probability of gains dwarfs the probability of losses. Although there is a relatively small chance that you could lose money in such circumstances, the wind is clearly at your back. At these junctures, dialing up your risk exposure is akin to shooting fish in a barrel – the likelihood of success is high while the risk of an adverse event is small.

John F. Kennedy & the Chameleonic Nature of Markets

Former President John F. Kennedy asserted that “The one unchangeable certainty is that nothing is certain or unchangeable.” With regard to markets, the risk and return profiles of different asset classes are not stagnant. Rather, they change over time depending on a variety of factors, including interest rates, economic growth, inflation, valuations, etc.

Given this dynamic, it follows that determining your optimal asset mix is not a “one and done” treatise, but rather a dynamic process that takes into account changing conditions. Yesterday’s optimal portfolio may not look like today’s, which in turn may be significantly different than the one of the future.

It’s not just the risk vs. return profile of any given asset class that should inform its weight with portfolios, but also how it compares with those for other asset classes. As such, investors should use changing risk/return profiles among asset classes to “tilt” their portfolios, increasing the weights of certain types of investments while decreasing others.

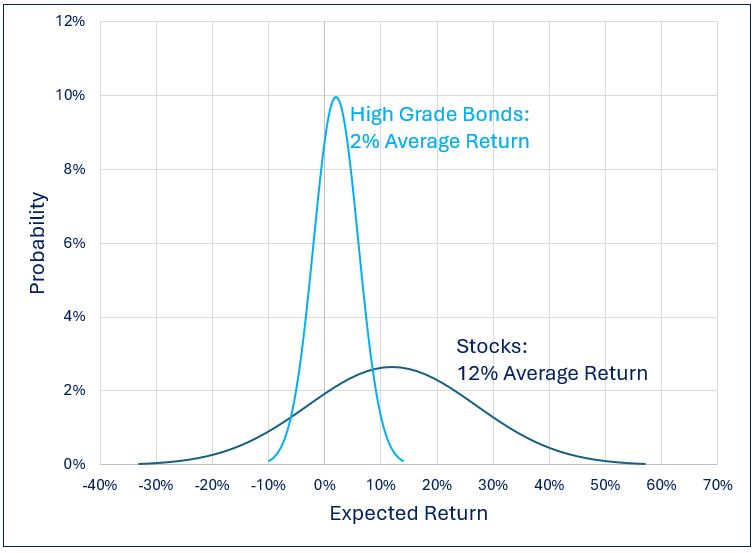

In “normal” times, the expected return from stocks exceeds the yields offered by cash and high-grade bonds by roughly 3% per annum. However, this difference can expand or contract depending on economic conditions and relative valuations among asset classes.

In the decade plus era following the global financial crisis, not only did rates remain at historically low levels, but the prospective returns on equities were abnormally high given the positive impact that low rates have on spending, earnings growth, and multiples. Against this backdrop, the prospective returns from stocks far exceeded yields on safe harbour investments. Under these conditions, it is no surprise that investors who had outsized exposure to stocks vs. bonds were handsomely rewarded.

Expected Return on Stocks vs. Yield on High Grade Bonds: Post GFC Era

As things currently stand, the picture is markedly different. Following the most significant rate-hiking cycle in decades, bonds are once again “back in the game.” Moreover, lofty equity market valuations (at least in the U.S.) suggest that the S&P 500 Index will deliver below-average returns over the next several years. Continue Reading…

In his 2024 re-election campaign, U.S. President Donald Trump vowed to pursue an aggressive trade policy that aimed to reduce or altogether eliminate what he viewed as unacceptable deficits between adversaries and allies alike. Following his January inauguration, President Trump has put Canada and Mexico into his crosshairs. Tariffs continue to be one of his favourite tools, if his rhetoric is any indication.

A tariff is a tax that is imposed by a country on the goods imported from another country. It is typically collected by a country’s customs authority. Some economists have argued that this results in a larger burden being paid by consumers, as companies will pass on tariff costs to the consumer.

In this piece, we will look at how ongoing trade tensions could impact world economies and markets. After that, we will zero in on ETFs that can potentially provide protection against the current bout of volatility.

Trade policy volatility and Canada

Last month, we looked at the impact the new GOP administration could have on the industrials space. That piece explored the trade policy volatility that existed in the first Trump administration.

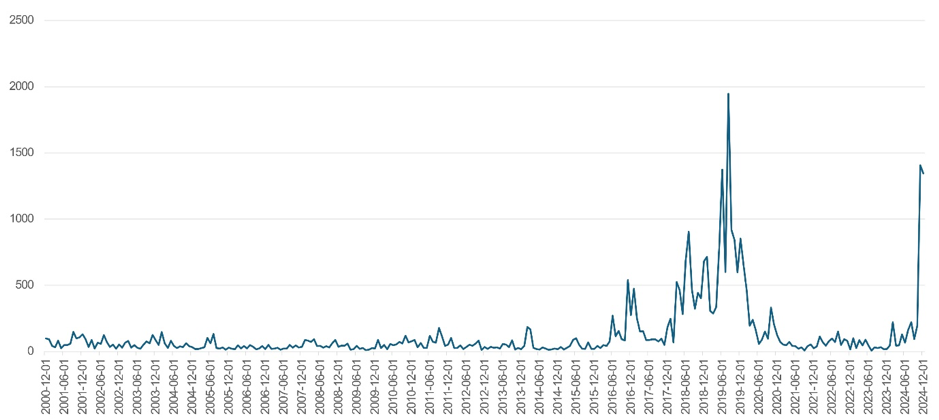

Baker, Bloom & Davis

US Categorical Economic Policy Uncertainty Index – Trade Policy

Source: Baker, Bloom & Davis. Bloomberg, Harvest ETFs, as of January 21, 2025.

On Monday, February 3, 2025, U.S. and global markets suffered sharp pullbacks in the morning hours. However, markets recovered after the Trump administration announced that tariffs on Mexico and Canada would be delayed for 30 days.

Canada finds itself at a crossroads as it contends with unprecedented pressure from a long-time ally, political uncertainty on the domestic front, and muted and decelerating economic data. The Bank of Canada must weigh these pressures as it determines how much it can slash interest rates to bolster economic activity..

That aside, Canada is home to many great companies with oligopolistic qualities. We detailed their strengths in a piece in October 2024. The Harvest Canadian Equity Leaders Income ETF (HLIF:TSX) invests in 30 of Canada’s most powerful and largest companies for their traits and growth potential. It overlays an active covered call strategy, which seeks to generate high monthly cash distributions.

Combat trade volatility with defence and diversification

Defensive sectors contain businesses that are stable, possess key barriers to entry, and are relatively immune to economic fluctuations.

Healthcare falls in this defensive category and is unique in its diversity. It includes companies that manufacture medical devices and equipment, as well as those that are involved in the making of diagnostic tools and lab equipment, companies involved in the ownership of doctors’ networks, as well as facilities and companies in the Managed Care segment.

The Harvest Healthcare Leaders Income ETF (HHL:TSX) is an equally weighted portfolio of 20 large-cap global healthcare companies. HHL aims to generate an attractive monthly distribution through an active covered call writing strategy. This ETF has paid out over $500 million in total monthly distributions to unit holders since its inception.

Utilities is a space that is often targeted by investors who are looking to shore up a defensive position in their portfolios. Companies in the utilities space possess enormous scale, significant barriers to entry, and dominance in their respective markets. The Harvest Equal Weight Global Utilities ETF (HUTL:TSX) offers access to a globally diversified portfolio of utilities equities. That global diversification offers benefits like reducing interest rate and natural disaster risk with exposure to different countries and regions. Continue Reading…