Most of your investing life you and your adviser (if you have one) are focused on wealth accumulation. But, we tend to forget, eventually the whole idea of this long process of delayed gratification is to actually spend this money! That’s decumulation as opposed to wealth accumulation. This stage may also involve downsizing from larger homes to smaller ones or condos, moving to the country or otherwise simplifying your life and jettisoning possessions that may tie you down.

My latest MoneySenseRetired Money column reprises a couple of interesting takes on the key factors in deciding one’s timing of taking on Retirement. You can read the full column by clicking on the highlighted headline here: The 5 Factors of Retirement for Canadians.

One take is from the Plutus-award winning US blogger and author Fritz Gilbert; the second a Canadian take from MyOwnAdvisor’s Mark Seed.

Then this site, as it often does with bloggers’ permissions, re-reran Gilbert’s blog late last year. It was then noticed by Mark, who was inspired to write his own version of the blog, with more of a Canadian spin and remarks on his personal perspective. It was also republished on the Hub.

So what was it that so intrigued three different financial bloggers (I’ll count this blog and the MoneySense column as evidence that three of us found it worthy of a write-up)?

Fritz Gilbert

Succinctly, here are the five factors originally identified by Gilbert:

Do you have enough money?

Are you mentally prepared for Retirement?

Have you made a realistic spending estimate?

Is your portfolio ready for withdrawals?

What’s your risk tolerance?

By now, you may be wondering about the mysterious sixth factor which in his blog Fritz says “doesn’t really matter at all.” Strangely, he adds, many people consider it to be the most important in their decision.

Spoiler alert: if you like a bit of suspense, read Fritz’s original blog before proceeding. For those who want the quick-and-dirty reveal, if you’ve not already guessed, it’s your age. Or as Fritz wrote: “For once in your life, age has nothing to do with this decision. Unlike driving, voting, and drinking, there are no legal constraints on when you can choose to retire. As long as you can check the boxes on the important factors listed earlier, you can choose to retire regardless of your age.” Continue Reading…

It’s never too early to start looking forward. I’ve been doing this on my site for some time and doing a bunch of assumptions and simulations on what our financial independence retire early might look like.

I also have interviewed many Canadians who are financially independent and/or retired early in my FIRE Canada Interviews.

Having some plans on your hands is better than no plans at all. Furthermore, having some quantitative targets available will allow you to set up different financial milestones and goals each year. Doing so will help you to stay focused and work your way to achieve them.

For those not familiar with Cashflows & Portfolios, it’s a site started by two long time Canadian bloggers, Mark and Joe. Mark runs My Own Advisor, which I started reading before I started this blog. Joe was the brain behind Million Dollar Journey, which I have been following for over a decade.

All three of us believe we need to retire the term: retirement. To be more specific, we believe it’s time to change the ‘traditional’ definition of retirement. It is also important to make sure you know what you’re retiring to.

Back in the day, when you turned 60 or 65, and once you had grown tired of working by already clocking decades of company time – trading those years in the workplace for your workplace pension to supplement income for your senior years.

Well, workplace pensions are dwindling and more and more, pursuing retirement in any traditional sense seems rather unhealthy today. A traditional retirement can be unhealthy physically, emotionally and financially.

On a physical level, retirement has traditionally meant a decrease in activity. You no longer have a driving reason to get out of bed in the morning, grab a coffee and get to the office – so you take it easier. That may not be beneficial to your wellness and based on my personal fitness experiences, not something that appeals to me.

On an emotional level, retirement for some could lead to social isolation. Potentially, you’ve identified and linked your self-worth to your organization, your co-workers and your manager.

Retirement means you’re leaving your workplace but the organization will undoubtedly continue to work without you being there. Unfortunately, life just works that way; it doesn’t stop for anyone. So, I believe it’s important to maintain a modest level of stimulation at any age, including retirement.

Not remaining socially engaged with other people in retirement could lead to mental health struggles.

Finally, retirement is not cheap, financially. Unless you have a workplace pension (and let’s face it, many Canadians don’t, me included!), you’ll need to rely on your disciplined, multi-decade savings rate to maximize your retirement income stream at age 40, 45, 50 or 55 – by giving up your regular paycheque.

Sure, while there are other retirement income streams to enjoy eventually, like Canada Pension Plan (CPP) and Old Age Security (OAS), many readers of this blog probably don’t want to wait until ages 60 or 65 to tap those income streams respectively.

Let’s get one point straight, it’s a privilege to be able to retire early at age 40, 45, 50 or 55. Early retirement isn’t for everyone and those who can “retire” early typically enjoy some sort of privileges in their lives. Such privileges need to be highlighted more within the FIRE community.

The reality is that you do need to have a certain level of income to build up enough assets by your 40s so your portfolio can withstand some drawdowns in the subsequent decades. A relatively high savings rate combined with a certain level of income will help and is in my opinion crucial. Continue Reading…

Recently, the Stingy Investor pointed to an article whose title caught my eye: The Academic Failure to Understand Rebalancing, written by mathematician and economist Michael Edesess. He claims that academics get portfolio rebalancing all wrong, and that there’s more money to be made by not rebalancing. Fortunately, his arguments are clear enough that it’s easy to see where his reasoning goes wrong.

Edesess’ argument

Edesess makes his case against portfolio rebalancing based on a simple hypothetical investment: either your money doubles or gets cut in half based on a coin flip. If you let a dollar ride through 20 iterations of this investment, it could get cut in half as many as 20 times, or it could double as many as 20 times. If you get exactly 10 heads and 10 tails, the doublings and halvings cancel and you’ll be left with just your original dollar.

The optimum way to use this investment based on the mathematics behind rebalancing and the Kelly criterion is to wager 50 cents and hold back the other 50 cents. So, after a single coin flip, you’ll either gain 50 cents or lose 25 cents. After 20 flips of wagering half your money each time, if you get 10 heads and 10 tails, you’ll be left with $3.25. This is a big improvement over just getting back your original dollar when you bet the whole amount on each flip in this 10 heads and 10 tails scenario. This is the advantage rebalancing gives you.

However, Edesess digs further. If you wager everything each flip and get 11 good flips and 9 bad flips, you’ll have $4, and with the reverse outcome you’ll have 25 cents. Either you gain $3 or lose only 75 cents. At 12 good flips vs. 12 bad flips, the difference grows further to gaining $15 or losing 94 cents. We see that the upside is substantially larger than the downside.

Let’s refer to one set of 20 flips starting with one dollar as a “game.” We could think of playing this game multiple times, each time starting by wagering a single dollar. Edesess calculates that “if you were to play the game 1,001 times, you would end up with $87,000 with the 100% buy-and-hold strategy,” “but only $11,000 with the rebalancing strategy.”

The problem with this reasoning

Edesess’ calculations are correct. If you play this game thousands of times, you’re virtually certain to come out far ahead by letting your money ride instead of risking only half on each flip. However, this is only true if you start each game with a fresh dollar. Continue Reading…

By Michael Kovacs, President & CEO of Harvest ETFs

(Sponsor Blog)

The Harvest Diversified Monthly Income ETF (HDIF:TSX) was built to meet Canadian investors’ need for income and sector diversity. We built it with a straightforward thesis, by holding an equal weight portfolio of established Harvest Equity Income ETFs, we could deliver growth potential and high monthly income. That made it one of the most popular Canadian ETFs launched in 2022.

Each of the ETFs held in HDIF captures a portfolio of leading large-cap businesses. They also each employ an active and flexible covered call option strategy to generate high income yields, offset downside, and monetize volatility. HDIF combined those ETFs with modest leverage at approximately 25% to deliver an enhanced income yield.

In April of this year, we launched the Harvest Diversified Equity Income ETF (HRIF:TSX). It holds the same equal-weight portfolio of Harvest ETFs, but without the use of leverage. Put simply, leverage adds a level of risk that some investors are not comfortable with. Therefore HRIF can deliver that same diversified portfolio of underlying ETFs and a high income yield in a package that more risk-averse investors may want to consider.

A truly diversified portfolio

At Harvest ETFs, we always start with portfolios of what we see as high-quality businesses. The ETFs held in HRIF capture companies that lead their sectors. By combining those portfolios into a single ETF, HRIF delivers a very diverse exposure to these companies.

The equal-weight portfolio held by HRIF at launch holds the following six ETFs.

Each ETF holds a portfolio of leading companies in their particular sector and market area. We define that leadership through quantitative and qualitative metrics such as market cap, market share, performance history and — in the case of certain underlying ETFs — dividend payment history. The companies selected in each ETF’s portfolio demonstrate leadership across those metrics.

HRIF also delivers a diverse set of performance drivers. Tech has been a market growth leader for over a decade and remains a key allocation for investors. Healthcare shows significant defensive qualities, especially during inflationary and recessionary times. The brand leaders in HBF and Canadian leaders in HLIF are selected in large part due to their resilience across market cycles, market shares, and dividend payment history. US banks have faced headwinds lately but have long-term positive exposure to interest rate increases and remain structurally important to the global economy. Utilities are an almost textbook definition of defensiveness, providing stability and ballast for the ETF.

Taken together, HRIF delivers leadership from a wide set of companies which, combined with its high income yield, makes it an attractive ETF for many investors.

HRIF’s High Income Yield Explained

HRIF launched with an initial target yield of 8.0% annually, paid as monthly cash distributions. That yield is earned by combining the underlying yields of its component ETFs, each of which employ an active & flexible covered call option strategy.

Covered call option ETFs effectively trade some upside potential for earned income premiums by ‘writing’ calls on a percentage of the ETF’s holdings. Where many covered call option ETFs use a passive strategy, writing calls on the same percentage of holdings each month, the Harvest ETFs held in HRIF use an active strategy. Continue Reading…

Well, a great deal of time has passed on that post by my thinking and goals remain the same – as least in part for semi-retirement!

Read on to learn why my approach to live off dividends remains alive and well this year in this updated post.

Why my goal to live off dividends remains alive and well

First, let’s back up to the controversy and offer a list why some investors couldn’t care less about my approach and why dividends may not matter at all to some people:

The trouble with any “live off the dividends” approach is that you’d need to save too much to generate your desired income. Fair.

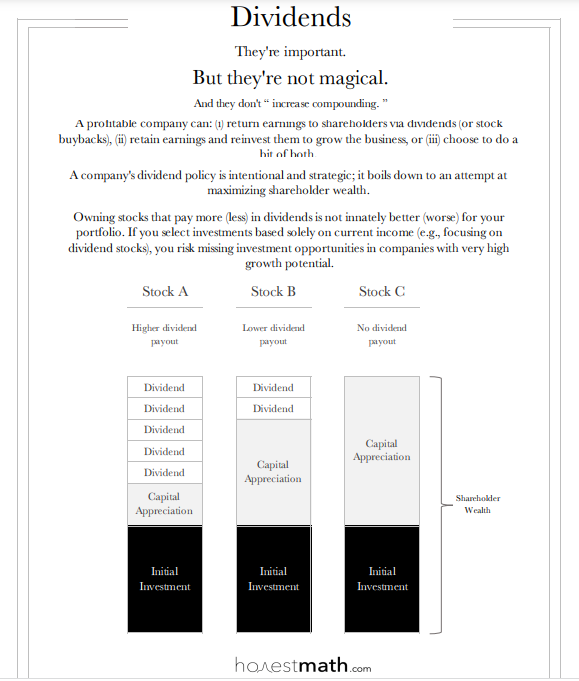

Dividends are not magical – there is nothing special about them. Sure.

A dollar of dividends is = a one-dollar increase in the stock price. True, a dollar is a dollar.

Stock picking (with dividend stocks) is fraught with under performance of the index long-term. I’m not convinced about that.

You can never possibly know long-term how dividends may or may not be paid by any company. Fair.

In many respects these investors are not wrong.

You do need a bunch of capital to generate income.

Dividends are part of total return. [See image at the top of this blog.]

Stock selection can open up opportunities for market under performance.

And the negativity doesn’t stop there …

Some financial advisors will argue your investing world starts to shrink if you demand 2% or 3% (or more) income from your portfolio, so dividend investing leads to poor diversification.

My response to this: I don’t just invest in dividend paying stocks.

Further still, some advisors will argue picking dividend paying stocks may lead to negative outcomes and too many biases.

My response to this: while I believe markets are generally efficient, I also believe that buying and holding some dividend paying stocks (while there could be market under-performance at times) does not necessarily mean I cannot achieve my goals. In fact, that’s the entire point of this investing thing anyhow – investing in a manner that keeps you motivated, inspired and helps you meet your long-term goals.

Consider this simple sketch art from Carl Richards, who is far more famous than I will be, and author of the One-Page Financial Plan and more:

Source: Behavior Gap.

From Carl’s recent newsletter in my inbox:

“Pretend you live in some magic fantasy world where all of your dreams (according to the investment industry) come true, and you actually beat an index every quarter for your whole life. Congratulations!

So here’s my question: You landed in Shangri La, according to the financial industry. You beat the index. But you didn’t meet your goals. Are you happy?

The answer is “No.”

Now let’s flip that scenario on its head. The worst thing in the world happens to you (again, according to the investment industry). You slightly underperform the index every quarter for your whole life. But because of careful financial planning, you meet every one of your financial goals. Let me repeat the question: Are you happy?

And the answer is obviously… “Yes.”

Stop worrying about beating indexes. Focus instead on meeting your goals.”

Amen.

Finally, some advisors will argue that dividends and share buybacks and other forms of reinvesting capital back into the business can be equally shareholder friendly.

My response to this: Well of course that makes sense. Dividends are just one form of total returns.

But you know what?

The ability to live off dividends (and distributions from our ETFs) will be beneficial for these reasons:

1. I continue to believe there are simply too many unknowns about the financial future. So, living off dividends and distributions will help ensure our capital remains hard at work since it will remain intact.

2. If we are able to keep our capital intact we don’t need to worry as much about when to sell shares or ETF units when markets don’t cooperate. We can sell assets as we please over time.

3. Living off dividends is therefore just one way I’m trying to reduce sequence of returns risks. See below.

Source: BlackRock.

As such, we’ll try to live off dividends and distributions in the early years of semi-retirement to avoid such risks.

4. I/we don’t necessarily believe in the 4% safe withdrawal rule. It’s impossible to predict next year, let alone 30 or more investing years.

5. I’m conservative as an investor. Seeing dividends roll into my account help me psychologically to stick to my investing plan.

6. Dividends is real money, tangible money I can spend if and when I choose without worrying about stock market prices or gyrations.

7. It is my hope dividends (and capital gains) can work together to help fight inflation. As consumer prices rise, as the cost of living rises, the companies that deliver our products and services will rise in price along with them.

8. I like dividend paying stocks for a bit of the “value-tilt” they offer.

In a taxable account Canadian dividend paying stocks are eligible for a dividend tax credit from our government. This means taxation on dividends are favourable, it is a lower form of tax; lower than employment income and interest income. This will help me in the years to come.

Will I eventually spend the capital from my portfolio?

Of course I will.

With no desire to leave a large estate, it wouldn’t make sense for us not to do so!

But with a “live off dividends” mindset I can sell assets or incur capital gains largely on my own terms during retirement. I plan to do just that.

Why my goal to live off dividends remains alive and well summary

This site continues to share a journey that includes how passive dividend income can fulfill many of our retirement income needs – whether that might be covering our property taxes, paying our utility bills, delivering enough monthly income to cover our groceries, fund some international travel or all of these things combined.

Here was one of my recent updates below.

We’re now averaging over $3,300 per month from a few key accounts.

(Hint: likely more next month!)

We’re trending in a great direction thanks to this multi-year investing approach and I have no intentions of changing my/our overall approach.

I firmly believe our focus on the income that our portfolio generates, instead of the portfolio balance, is setting us up to deliver some decent semi-retirement income.

Our goal to live off dividends and distributions remains very much alive and well for the years ahead.

I look forward to your comments.

Mark Seed is a passionate DIY investor who lives in Ottawa. He invests in Canadian and U.S. dividend paying stocks and low-cost Exchange Traded Funds on his quest to own a $1 million portfolio for an early retirement. You can follow Mark’s insights and perspectives on investing, and much more, by visiting My Own Advisor. This blog originally appeared on his site on March 27, 2023 and is republished on the Hub with his permission.

My latest MoneySense Retired Money column reprises a couple of interesting takes on the key factors in deciding one’s timing of taking on Retirement. You can read the full column by clicking on the highlighted headline here: The 5 Factors of Retirement for Canadians.

My latest MoneySense Retired Money column reprises a couple of interesting takes on the key factors in deciding one’s timing of taking on Retirement. You can read the full column by clicking on the highlighted headline here: The 5 Factors of Retirement for Canadians.