Most of your investing life you and your adviser (if you have one) are focused on wealth accumulation. But, we tend to forget, eventually the whole idea of this long process of delayed gratification is to actually spend this money! That’s decumulation as opposed to wealth accumulation. This stage may also involve downsizing from larger homes to smaller ones or condos, moving to the country or otherwise simplifying your life and jettisoning possessions that may tie you down.

Well, readers of this site will know I’m a big fan of companies that reward shareholders with dividends.

And why not love dividends?

Although I use a few indexed products in my investment portfolio, for extra diversification just in case, getting paid on a consistent, growing basis from Canadian and U.S. stocks: that’s a beautiful thing. I got another raise this week that I’ll link to below!

Digging deeper, I’m not that worried about the markets or inflation right now. There is a reason why dividends matter to me. Why do dividends really matter?

Beyond the Canadian dividend tax credit, beyond consistent payments and ever growing income I’ve experienced to date, dividends help me stick to my plan.

There is no financial advisor in my plan, nor fees paid to any advisor in my plan.

There is no day trading, there are no wasted fees or losses for trading.

There is no wild market speculation, I’m not trying to time anything.

I focus on my savings rate for investing and I invest more money when I have it. It’s that simple.

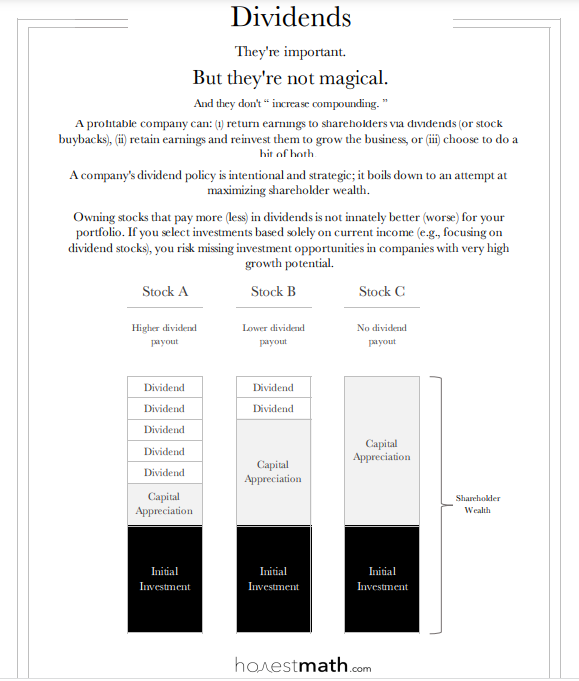

Recall that dividends paid is real money paid from real company profits. Buying and holding an established company that has paid dividends for decades is a good sign (at least from a historical perspective) that this company had enough cashflow to reward shareholders and stay in business.

Companies that don’t pay dividends tend to use their money for other means, grow their business; make acquisitions or buy back shares, pay down risky debt, therefore driving the stock price higher over time.

These are not poor management decisions by any means: far from it. There are lots of ways shareholder value is created and to be honest, acquisitions, share buybacks and other company reinvestments could be better company decisions in the long-run!!

When it comes to the capital gains versus dividend income debate, there really isn’t a debate to be had, since every dollar you earn in capital gains from a stock is worth just as much as your dividend dollar paid. I love the graphic shown at the top of this blog.

Dividends from established companies however are paid consistently, and dividend payments might even rise over time by some, so this level of predictability can provide some financial security especially when you’re invested in a diverse portfolio of stocks.

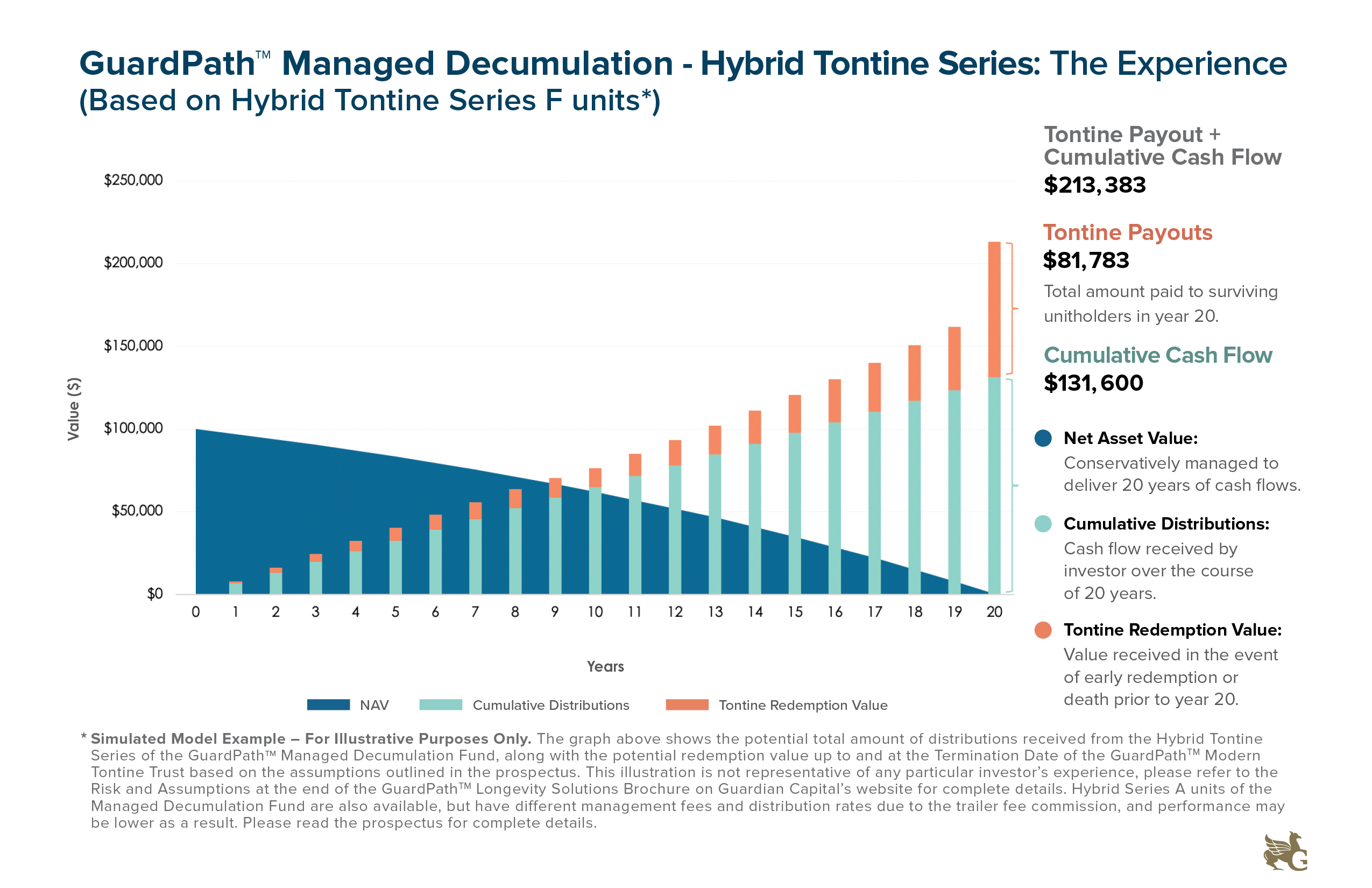

We’ve illustrated this blog with financial projections of one of the three new Guardian Capital Retirement solutions developed in partnership with Milevsky. Some of the ideas were adapted from Milevsky’s latest book: How to Build a Modern Tontine. The theory behind this book is a driving force for Guardian Capital’s efforts to commercize these concepts and put them in the hands of retirees and would-be retirees worried about outliving their money. Nobel Laureate Economist William Sharpe has described this as “the nastiest, hardest problem in finance.”

Milvesky’s book is certainly aimed at industry practitioners and sophisticated financial advisors and investors, and contains a lot of mathematics that may beyond the reach of average investors or retirees. So rather than attempt to review it, we’ll move on to the efforts to bring these ideas to the market. What Milevsky calls “tontine thinking” is belatedly showing up in the marketplace in Canada, starting last year with Purpose Investments’ and now with three different solutions from Guardian Capital. Hub readers also can read an excerpt of the book which ran earlier Wednesday: Longevity Insurance vs Credits — a Primer.

All this has been a long time coming. MoneySense readers may recall two of my Retired Money columns about Milevsky and the future of tontines published in 2015: Part one is here and part two here. Also see my 2018 column that explains tontines in detail: Why Ottawa needs to push for tontine-like annuities.

As the MoneySense feature explains, Milevsky is Guardian Capital’s Chief Retirement Architect. It sums up the original 2021 launch of Purpose Longevity Fund, and how it compares to Guardian’s three solutions.

Think of Purpose’s product as a lower-case tontine, and Guardian Capital’s as a Tontine with a capital T.

Guardian Capital’s Modern Tontine

Guardian Capital’s September 7thpress release uses the term “Modern Tontine.” There, Guardian Capital Managing Director and Head of Canadian Retail Asset Management Barry Gordon said “With our modern tontine, investors concerned about outliving their nest egg pool their assets and are entitled to their share of the pool as it winds up 20 years from now … Over that 20-year period, we seek to grow the invested capital as much as possible to maximize the longevity payout.”

Along the way, investors who redeem early or pass away leave a portion of their assets in the pool to the benefit of surviving unitholders, boosting the rate of return. “All surviving unitholders in 20 years will participate in any growth in the tontine’s assets, generated from compound growth and the pooling of survivorship credits. This payout can be used to fund their later years of life as they see fit, and aims to ensure that investors don’t outlive their investment portfolio.” Continue Reading…

This guest blog is excerpted from Moshe Milevsky’s recently published book, How to Build a Modern Tontine

By Prof. Moshe A. Milevsky, Ph.D.

Special to the Financial Independence Hub

I have been asked about the difference between a tontine – be it modern or medieval – and a conventional life annuity, purchased from a regulated life insurance company. Both might appear to perform similar tasks at first glance, but the differences are subtle and important and get to the essence of the distinction between longevity insurance versus longevity (or survivorship) credits.

One aspect of the life annuity story is the financial benefit of risk pooling, and the other is the insurance benefit and comfort from having a guaranteed income that you can’t outlive. Allow me to elaborate with a statement that some readers might find shocking. If you are 75 years old with $100,000 in your RRIF and would like to guarantee a fixed annual income for the rest of your life, there is absolutely no need to purchase a life annuity from an insurance company to achieve that goal. There are other options.

This might sound like something odd for a long-term annuity advocate to say. But the fact is that a non-insurance financial advisor can design a lovely portfolio of zero-coupon strip bonds that will do the job. That collection of bonds will generate $4,000 per year for the rest of your life, even if you reach the grand old age of 115. Ok, financial advisors need to eat too, so they may not do it for $100,000, but I’m sure that a lump sum of $1,000,000 will pique their interest and in exchange you will get $40,000 per year.

Moreover, with these strips, if you don’t make it all the way to the astonishing age of 115, they will continue to send those $4,000 (or $40K) to your spouse, children or favourite charity until the date you would have reached 115, if you had been alive. This collection of strips would be completely liquid, tradeable and fully reversable, although subject to the vagaries of bond market rates. For this I have assumed a conservative, safe and constant 2.5% discount rate across the entire yield curve, which isn’t entirely unreasonable in today’s increasing environment.

Stated technically, the present value of the $4,000 annual payments, for the 40 years between your current age 75 and your maximum age 115, is exactly equal to $100,000 when discounted at 2.5%. Yes, those numbers and ages were deliberately selected so my numerical example rhymes with the infamous 4% rule of retirement planning but has absolutely nothing to do with it.

Now, I’m sure you must now be thinking (or even yelling) “Moshe, but what if you live beyond age 115, eh? You will run out of money!”

Touché. Let’s unpack that common knee-jerk reaction to non-insurance solutions for a moment. To start with, the probability of reaching age 115 is ridiculously and unquantifiably low. If you do happen to be the one in a 100 million (or perhaps billion) that reaches age 115, I suspect you will have other things on your murky mind. Personally and post-covid, there is a very long list of hazards that worries me more than hitting 115.

Nobody really “runs out of money” in this century

Second and more importantly, nobody really “runs out of money” in retirement in the 21st century. That is plain utter fear-mongering nonsense. With CPP, OAS/GIS, the elderly will continue to receive some income for as long as they live even if they have completely emptied every piggy bank on their personal balance sheet. In fact, with tax-based means-testing you might get more benefits if you actually do empty your bank accounts.

Ok, so back to my prior claim and the supporting numbers, if you want a guaranteed (liquid, reversable, bequeathable) income for the rest of your life, you can exchange your $100,000 for a bunch of strip bonds and voila, you have created a sort of pension plan. My point here is that the primary objective isn’t a guaranteed lifetime of income: which anyone can create with a simple discount brokerage account and a DIY instruction manual. Continue Reading…

As we update our list of the Best Canadian Dividend Stocks for 2022, we continue to focus on four key areas:

Dividend Yield

Dividend Growth Consistency

Earnings Per Share

Overall Company Revenues

As we head into Q3, Canadian dividend stocks have continued to reward our confidence in them. While high-flying tech stocks have gotten slaughtered (and then recovered a little bit), and European stocks continue to see their growth evaporate, Canadian oligopolies continue to churn out dependable dividend growth. With Canadian forward P/E now at 12 – well below their historical average of 14 – there is no better place to be in terms of equity exposure if you prize caution and dividend yield.

While they have suffered drawdowns at times due to market-wide momentum, they have held up quite well, and earnings reports have supported the long-term viability of their dividends.

While many companies around the world are seeing their bottom lines chewed up by increasing costs, our top Canadian dividend stocks continue to show the pricing power that made us so confident in recommending them in the first place.

As a longtime dividend investor (I’ve had a Canadian dividend investing portfolio for over 15 years now, since I started the Smith Manoeuvre) I’ve learned that while current dividend yield is a beautiful thing, it’s the long-term dividend growth and earnings per share (EPS) that will really drive your overall portfolio returns.

My personal selection for the top dividend stocks for long-term investments are available below.

Our Top 10 Canadian Dividend Growth Stocks (September 2022)

Here’s a look at our top 10 long-term Canadian dividend stocks in order of their dividend increase streak.

For my full 32-stock list of Canadian dividend earners that I’m buying today – as well as the 74-stock list of US Dividend all stars that I recommend – check out the platform that I personally use to do my dividend stock research.

Note: Data on this article updates periodically. If you are looking for real time data and guidance, read our recommendation below.

More Up to Date Canadian Dividend Stocks Data

The easiest way to keep up to date with the best dividend stock picks, is by signing up with Dividend Stock Rock. DSR is not just a weekly newsletter with stock picks. It’s a program that will help you manage your portfolio and improve results using unique and sophisticated tools.

The person behind DSR is Mike, the most prominent and active dividend stock blogger in Canada and is a certified financial planner since 2003.

You can first read our detailed DSR review, or sign up now by clicking the button below. Our readers are eligible for an exclusive 33% off discount using code MDJ33.

Visit DSR & Get Exclusive Discount

2022 Canadian Dividend Update

The war in Ukraine has shaken markets around the world, and with the word “recession” appearing every two paragraphs in most financial publications, people have pulled money out of markets to some degree. (Although perhaps not as much as the initial “meltdown skeptics” initially anticipated.)

This has resulted in some stocks seeing their valuations get beat up despite actually increasing both their revenues and operating profits. You can see from the chart below for example that Canadian banks stocks just continue to print free cash flow and increase dividends at a safe (but lucrative) rate.

Given their very attractive current valuations, you’d have to expect a recession to crater their earnings by 20%+ for this to make sense – and I just don’t see that happening.

Bank

Dividend Increase

EPS

2017 Dividend

2021 Dividend

2022 Dividend

Payout Ratio

BMO.TO

25.47%

53.28%

$0.88

$1.06

$1.33

36.56%

NA.TO

22.54%

57.29%

$0.56

$0.71

$0.87

31.37%

TD.TO

12.66%

20.06%

$0.55

$0.79

$0.89

40.86%

RY.TO

11.11%

41.39%

$0.83

$1.08

$1.20

39.02%

BNS.TO

11.11%

45.30%

$0.76

$0.90

$1.00

46.54%

CM.TO

10.27%

69.38%

$1.27

$1.46

$1.61

41.81%

With payout ratios like the ones above, combined with those really solid Earnings Per Share numbers – we remain strong in our belief that there are no better options for investors who want stable long-term growth combined with free cash flow.

With inflation fears now dominating the media news cycle, we see more than ever that companies with solid balance sheets and oligopoly-driven moat stocks are the smart long-term play. Companies that can pass along those inflation-fuelled rise in costs have historically outperformed during inflation cycles.

Frankly, I think all of this talk about inflation might be a bit overdone, and that it’s likely to come down to the 3-3.5% range next year. At that rate, it’s really only a mild concern in the grand scheme of things. I’d be much more worried if this was deflation we were talking about!

Our list of top Canadian inflation stocks explains exactly which companies we believe are best positioned in order to pass along the inevitable price increases and increased costs that will come along in 2022.

Of course we remain committed to our long-term strategy of balancing EPS with a company’s ability to grow its dividend, in order to allocate our personal dividend nest egg.

Afterall, the only thing better than a high dividend yield today, is a much larger (and increasing) one tomorrow!

Check out our in-depth Dividend Stocks Rock Review for a deeper dive on just why we trust the service so much, and more details on our exclusive promo offer code.

My Top Canadian Dividend Stock Recommendations

Sorted in order of dividend streak:

Fortis (FTS.TO) – 48 Years of Dividend Growth

3.67% Dividend Yield

6.68% 5 Year Revenue Growth

6.10% 5 Year Dividend Growth

79.85% Payout Ratio

22.06 P/E

Investment Thesis:

Fortis aggressively invested over the past few years resulting in strong and solid growth from its core business. You can expect FTS’s revenues to continue to grow as it continues to expand. Strong from its Canadian based businesses, the company has generated sustainable cash flows leading to four decades of dividend payments.

The company has a five-year capital investment plan of approximately $19.6 billion for the period 2021 through 2025. Only 33% of its CAPEX plan will be financed through debt. Nearly two-thirds will come from cash from operations. Chances are most of its acquisitions will happen in the US.

We also like the FTS goal of increasing its exposure to renewable energy from 2% of its assets in 2019 to 7% in 2035. The FTS yield isn’t impressive at around 3.70%, but there is a price to pay for such a high-quality dividend grower.

Dividend Growth Perspective:

Management increased its dividend 6% in 2019 and 2020 and has declared that it expects to increase dividends by 6% annually until 2025. We like it when companies show motivation for growth (through acquisitions) and reward shareholders at the same time!

After all, Fortis is among those rare Canadian companies who can claim it has increased its dividend for 48 consecutive years. Fortis is a great example of a “sleep well at night” stock.

Enbridge (ENB.TO) – 26 Years of Dividend Increases

6.38% Dividend Yield

6.37% 5 Year Revenue Growth

9.52% 5 Year Dividend Growth

117.23% Payout Ratio

22.30 P/E

Investment Thesis:

ENB’s customers enter 20-25-year transportation contracts. It is already well positioned to benefit from the renewed profits of the Canadian Oil Sands (as its Mainline covers 70% of Canada’s pipeline network).

As production grows, the need for ENB’s pipelines remains strong.

After the merger with Spectra, about a third of its business model will come from natural gas transportation. Enbridge has a handful of projects on the table or in development. It must deal with regulators notably for their Line 3 and Line 5 projects. Both projects are slowly but surely developing.

The cancellation of the Keystone XL pipeline (TC Energy) secures more business for ENB for its liquid pipelines. ENB has now a “greener” focus with their investments in renewable energy. The stock offers a yield over 6% which makes it a strong candidate for any retirement portfolio.

Dividend Growth Perspective:

The company has been paying dividends for the past 65 years and has 26 consecutive years with an increase. While it’s probable dividend growth won’t be as generous as compared to the past three years (10%/year), the current generous yield makes up for it. Management aims at distributing 65% of its distributable cash flow, leaving enough room for CAPEX.

Look for their latest quarterly presentation for their payout ratio calculation. Management expects distributable cash flow growth of 5-7%. Therefore, you can expect a similar dividend growth rate. We have used more conservative numbers in our DDM calculation.

Canadian National Railway (CNR.TO) – 26 Years of Dividend Increases

1.90% Dividend Yield

3.76% 5 Year Revenue Growth

10.40% 5 Year Dividend Growth

35.57% Payout Ratio

21.17 P/E

Investment Thesis:

Canadian National has been known for being the “best-in-class” for operating ratios for many years. CNR has continuously worked on improving its margins. The company also owns unmatched quality railroads assets.

CNR has a very strong economic moat as railways are virtually impossible to replicate. Therefore, you can count on increasing cash flows each year. Plus, there isn’t any more efficient way to transport commodities than by train. The good thing about CNR is that you can always wait for a down cycle to pick up some shares. There’s always a good occasion around the corner when we look at railroads as attractive investments.

Finally, the cancellation of the Keystone XL pipeline has driven more oil transportation toward railroads. CNR has benefitted from this tailwind.

In 2021 CNR entered a bidding war against CP to buy the Kansas City Southern Railroad. When the deal fell through for CNR, and the company announced a renewed focus on efficiency, long-term investors were rewarded handsomely as the stock shot up in value.

Dividend Growth Perspective:

CNR has successfully increased its dividend yearly since 1996. The management team makes sure to use a good part of its cash flow to maintain and improve railways, all while rewarding shareholders with generous dividend payments.

CNR shows impressive dividend records with very low payout ratios. While the business could face headwinds from time to time, its dividend payment will not be affected. Shareholders can expect more high-single-digit dividend increases.

Telus (T.TO) – 18 Years of Dividend Increases

4.58% Dividend Yield

5.76% 5 Year Revenue Growth

6.68% 5 Year Dividend Growth

103.38% Payout Ratio

22.10 P/E

Investment Thesis:

Telus has grown its revenues, earnings, and dividend payouts on a very consistent basis. It is very strong in the wireless industry and is now attacking other growth vectors such as the internet and television services.

The company has the best customer service in the wireless industry as defined by their low churn rate. It uses its core business to cross-sell its wireline services. Telus is particularly strong in Western Canada, but has the recent Rogers turmoil to increase market share throughout the country.

Telus is well-positioned to surf the 5G technology tailwind. This Canadian telecom stalwart looks at original (and profitable) ways to diversify its business. Telus Health, Telus Agriculture and Telus International (artificial intelligence) (TIXT.TO) are small, but emerging divisions that should lead to more growth going forward.

Dividend Growth Perspective:

This Canadian Aristocrat is by far the industry’s best long-term dividend-payer (as opposed to short-term yield). Telus has a high cash payout ratio as it puts more cash into investments and capital expenditures.

Capital expenditures are always taking away significant amounts of cash due to their massive investment in broadband infrastructure and network enhancement. Such investments are crucial in this business.

Telus fills the cash flow gap with financing for now. At the same time, Telus keeps increasing its dividend twice a year showing strong confidence from management.

Emera (EMA.TO) – 15 Years of Dividend Increases

4.31% Dividend Yield

6.15% 5 Year Revenue Growth

5.24% 5 Year Dividend Growth

128.82% Payout Ratio

29.42 P/E

Investment Thesis:

Emera is a very interesting utility with a solid core business established on both sides of the border. EMA now shows $32 billion in assets and will generate annual revenues of about $6 billion. It is well established in Nova Scotia, Florida, and four Caribbean countries.

This utility is counting on several “green projects” consisting of both hydroelectric and solar plants. Between 2021 and 2023 management expects to invest $7.4 to $8.6B in new projects to drive additional growth. These investments decrease the risk of future regulations affecting its business as the world is slowly moving toward greener energy.

Most of its CAPEX plan will be deployed in Florida where Emera is already well established. In general, Florida offers a highly constructive regulatory environment. In other words, EMA shouldn’t have any problems raising rates. This is another “sleep well at night” investment.

Dividend Growth Perspective:

Emera has been increasing its dividend payments each year for over a decade. With the purchase of TECO energy management intends to continue that tradition. The company forecasts a 4-5% dividend growth rate through 2022, while targeting a payout ratio of 70-75%.

At a 4%+ dividend yield, this is a keeper for several years. Don’t get fooled by the high payout ratio, as the adjusted earnings show a payout ratio around 80% including the recent dividend growth. This is the type of company that fits perfectly in a retirement portfolio.

It’s a trade-off. I hold a concentrated portfolio of Canadian stocks. What I give up in greater diversification, I gain in the business strength and potential for the companies that I own to not fail. They have wide moats or exist in an oligopoly situation. For the majority of the Canadian component of my RRSP account I own 7 companies in the banking, telco and pipeline space. I like to call it the Canadian wide moat portfolio.

(updated August 24, 2022) Like many Canadian investors I discovered over the years that my Canadian stocks that pay very generous dividends were beating the performance of the market. You’ll find that market-beating event demonstrated by the Beat The TSX Portfolio. Eventually, I moved to the stock portfolio approach.

Over longer periods you’ll see that BTSX beat the TSX 60 by 2% annually or more. And as always, past performance does not guarantee future returns.

For the bulk of my Canadian contingent I hold 7 stocks.

Canadian banking

Royal Bank of Canada, Toronto-Dominion Bank and Scotiabank.

Telco space

Bell Canada and Telus.

Pipelines

Canada’s two big pipelines are Enbridge and TC Energy (formerly TransCanada Pipelines).

For the U.S. component there is a basket of U.S. stocks. Here’s an update of our U.S. stock portfolio. That portfolio continues to provide impressive market-beating performance.

Here’s the Canadian wide moat 7 from 2014 vs the TSX Composite, to the end of July 2022. I slightly overweight to the telcos and banks. The portfolio for demonstration purposes is rebalanced every year. When reinvesting I usually throw money at the most beaten-up stock. That would be a reinvestment strategy that seeks value and greater income, the general approach of the Beat The TSX Portfolio.

2021 was a very good year for the wide moat portfolio. It beat the TSX, but did underperform the Beat The TSX Portfolio model and Vanguard’s High Dividend ETF (VDY). The outperformance of the Wide Moat 7, over the market, is accelerating in 2022.

In 2022 the Canadian Wide Moat 7 is up 1.14%. The TSX Composite is down 5.56%. For the record, the Vanguard High Dividend (VDY) is up 2% in 2022 to the end of July.

Charts courtesy of Portfolio Visualizer

Annualized returns and volatility

The Canadian Wide Moat 7 has delivered greater total returns and with less volatility and less drawdowns in corrections. The market beat is somewhat consistent with the Beat The TSX Portfolio beat of over 2% per year.

And of course the portfolio dividend income is more than impressive. I did not create portfolio exclusively based on the generous and growing income, but it is a wonderful by-product. The following is based on a hypothetical $10,000 portfolio start amount. The starting yield is above 4%, growing towards a 10% yield (on cost) based on the 2014 start date.

In the above, the dividends are reinvested. For example, the Telus dividend is reinvested in Telus. While I will take a total return approach for retirement funding, the generous portfolio income contribution will add a dimension that will help reduce the sequence-of-returns risk. I am in the semi-retirement stage.

Performance update to the end of May 2022

In this chart I begin with the inception date of the Vanguard High Yield VDY, 2013. We see the Canadian Wide Moat 7 vs VDY and the TSX Composite – XIC.

The Wide Moat stocks have outpeformed for the full period, but that is thanks mostly to better returns out of the gate. The outperformance is also aided by lesser drawdowns in market corrections. We see that both the Wide Moat approach and VDY have beat the market, with ease.

Wide Moats with an energy kick

I also hold Canadian energy stocks in the mix. That energy allocation is near 10%. Here’s what it looks like over the last year with that energy kicker. The following table looks at from January of 2021 to the end of July 2022. Continue Reading…