By Ambrose O’Callaghan, Harvest ETFs

(Sponsor Blog)

Back in December 2023, we looked at how a barbell bond strategy works. In this piece, we will explore the barbell investing strategy from a different perspective. Conceptually, this investment strategy seeks to strike a balance between risk and reward by investing in high-growth “risk-on” assets, and defensive “risk-off” assets. By accessing the benefits of both “extremes,” this strategy aims to achieve balanced capital gains.

Today, we will review the barbell strategy using six Harvest ETFs on each end. Three defensive-oriented ETFs that also provide access to monthly cashflow through an active covered call option strategy, and three “risk-on” ETFs that offer exposure to growth-oriented areas, while also delivering consistent cashflow every month.

Reducing Risk | Defensive Income ETFs

HHL | Healthcare exposure plus monthly income

In August, we provided an overview of the healthcare space and how it has impacted the Harvest Healthcare Leaders Income ETF (TSX: HHL), Canada’s largest healthcare ETF. To reiterate; the health care sector has shown both defensive and growth-oriented qualities through its history. Healthcare is defensive due to the essential nature of it services, whereas its growth qualities stem from the high demand for specialized products as well as technological innovations.

Healthcare equities have faced challenges in North American and global markets through the first three quarters of 2025. As we highlighted in our recent monthly commentary, valuations have been compressed relative to the market and investors have looked for catalysts for a rebound in this climate. To that end, it is worth highlighting some stock-specific catalysts that are starting to surface.

Those catalysts have included Warren Buffett’s UnitedHealth purchase and headlines focused on the issue of reshoring and repatriation. More stock-specific catalysts have included some positive earnings released across select names. The most recent examples came in the form of Intuitive Surgical Inc., which jumped double-digits on the back of an improved medical devices market and large-capitalization biopharmaceutical innovator Regeneron Pharmaceuticals that posted strong returns following and upbeat quarter. Compared to previous quarters when strong earnings went virtually un-noticed by the markets, seeing strong stock performance matching the strong reported earnings is perhaps a more subtle sign that sentiment has stabilized in the sector.

HHL offers exposure to a defensive sector that also has growth qualities. The portfolio is composed of 20 large-cap U.S. healthcare stocks, overlayed with an active covered call option writing strategy to generate high levels of monthly income. Indeed, HHL has delivered income every month for over a decade since its inception.

HUTL | Why utilities right now?

Utilities have long been regarded as a mainstay for those seeking stability, income, and defensive positioning in their portfolios. However, rising power demand, technological progress, policy shifts, and the ongoing global energy transition has made utilities a unique target for those who also want growth qualities. The Harvest Equal Weight Global Utilities Income ETF (TSX: HUTL) offers unique advantages as a utilities ETF, due to its global reach and its income generation.

HUTL | Benefits of utilities and steady income

Essential services with stable cash flows

Utilities deliver critical services like electricity, gas, water, and telecommunication, which are largely immune to economic cycles. Because of this, utilities are a stable source of revenue and cashflow.

Power demand growth

Electricity demand has soared in recent years and is set to increase at an even greater rate due to the proliferation of data centres and a broad electrification push. Data centres consumed roughly 1.5% of global electricity in 2024, a rate that could double by 2030. Goldman Sachs estimates that data centre power demand will grow by 165% by 2030.

Energy transition & infrastructure spending

Clean energy investment is projected to reach $2.2 trillion this year, more than double fossil fuel investment. HUTL offers exposure to leaders in this space, including VERBUND AG, Endesa, Fortum, Brookfield Renewable, and others. Meanwhile, the IEA forecasts that $450 billion will go into solar investment in 2025, with additional spending in grid and storage spending.

Diversification and the global advantage

Utilities are critical, but these companies also face risks from climate events and changing regulatory policy. HUTL’s global equal-weighted portfolio means that utilities exposure is spread across regions, reducing concentration risk. This helps to mitigate that regulatory risk as well as geographic challenges like storms, wildfires, and a changing political landscape.

Income generation and lower volatility

HUTL utilities Harvest’s active covered call option writing strategy to generate option premiums, which also serves to reduce portfolio volatility. Meanwhile, the utilities sector has historically outperformed during turbulent market periods. This is an added benefit in an uncertain market.

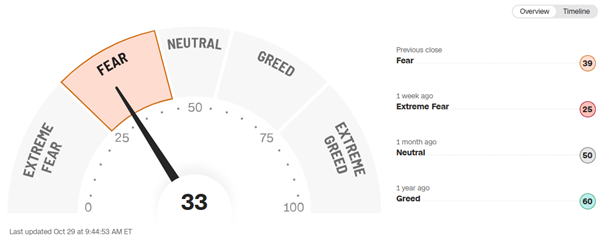

HVOI | A low volatility strategy with monthly income

In April, broader markets were reeling from the uncertainty that emerged in the wake of the “Liberation Day” tariff announcement. Markets have calmed in the months that followed, with the U.S. administration rolling back significantly on the high tariffs it originally had promised. That said, the CNN Fear and Greed Index shows that investors remain concerned at this late stage in 2025.

CNN Fear & Greed Index

Source: CNN.com, Fear & Greed Index, October 29, 2025.

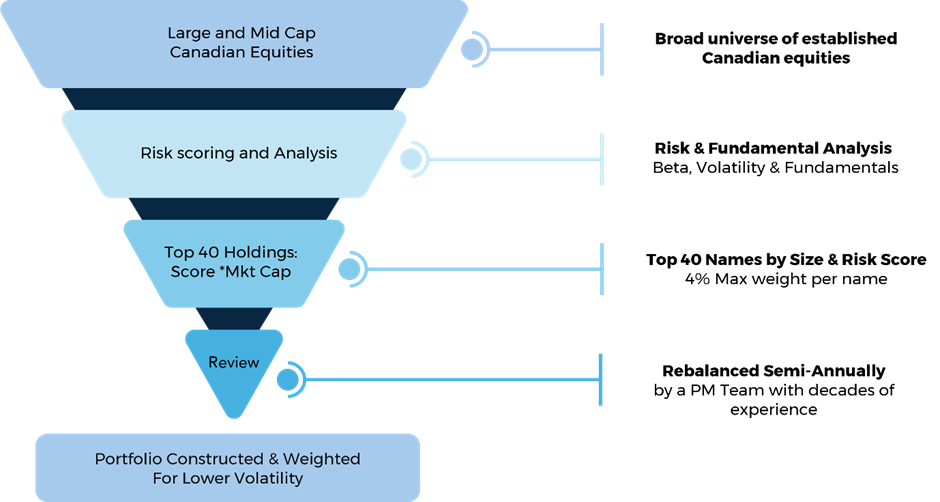

Harvest launched the Harvest Low Volatility Canadian Equity Income ETF (TSX: HVOI) in April 2025. This ETF holds 40 top Canadian equities, which are ranked and weighted by their risk score and market cap weight, with a 4% maximum weight per name. The equities are scored according to risk and fundamental metrics.

Low Volatility | Portfolio Construction

Source: Harvest Portfolios Group, Inc. April 2025.

Benefits of HVOI

- Access to rules-based portfolio that manages risk

- Covered call strategy to generate monthly cashflow and lower volatility

- Flexibility to employ cash-secured puts to generate additional income

- Rules-based and disciplined portfolio construction process

Pressing Offense | 3 Growth-Oriented Income ETFs

HHIS | One ETF with top U.S. stocks built for a high monthly yield

In August 2024, Harvest ETFs launched the Harvest High Income Shares™ ETF suite. High Income Shares™ are single-stock ETFs that offer exposure to top companies in both the United States and Canada. The ETFs are overlaid with an active covered call writing strategy, seeking to generate high monthly income. Harvest High Income Shares™ have reached above $3 billion in total AUM since inception at the time of this publication. Continue Reading…