Most of your investing life you and your adviser (if you have one) are focused on wealth accumulation. But, we tend to forget, eventually the whole idea of this long process of delayed gratification is to actually spend this money! That’s decumulation as opposed to wealth accumulation. This stage may also involve downsizing from larger homes to smaller ones or condos, moving to the country or otherwise simplifying your life and jettisoning possessions that may tie you down.

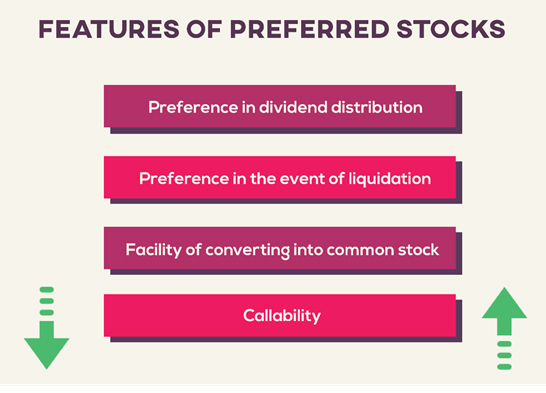

You identify preferred shares by their stock symbols. Their symbol contains a “PR” or a “PF.” For example, an Enbridge Inc. preferred share is ENB.PR.N.

Preferred shares pay dividends, often in the range of 5 or 6 per cent. This is usually one or two per cent more than what the company pays common share holders.

Like a bond, they are a form of loan; thus they do not share in the capital gain of a corporation, nor do they have any ownership or voting rights. While they rank ahead of common shares in realizing money from a company’s liquidation, they rank behind bondholders. Their ranking is of little benefit. After the lawyers, bankruptcy trustees and the banks (with their fully secured debentures) are paid off, the chance of anything being left for distribution is just about nil.

While you can conveniently buy and sell preferred shares on the stock market very few investors have any interest in them. Zero trades in a day is not unusual. There are 654 shares on the TSX pay paying a dividend of 3.5%. or more. Of these, 364 are preferred shares and of those only 112 had more than 4,000 shares traded in a typical day, despite their high dividends. This is due to the low possibility of preferred shares delivering an increase in share price to speculators.

Preferred shares are issued at a standard price of $25 each. Of the 364 preferred shares only 17 had a share price exceeding $25 and of these only one was greater than $30. The chance of realizing a capital gain from a preferred share is 1.91% and 183 or (50% of them) had lost at least 20% of their value. They were now worth less than $20. Five were trading for less than $10. It is not surprising that not one analyst recommended that investors buy any of these 364 preferred shares. Continue Reading…

One of the more frequent questions I get from clients regarding their retirement planning is, with the pension income splitting legislation, are spousal RRSPs worthwhile anymore? The answer is yes, in several situations.

Before I outline the planning situations that are useful for spousal RRSPs, first a little primer on what they are and how pension income splitting changed the view of them.

Spousal RRSPs

A spousal RRSP is an RRSP account in which one spouse makes contributions based on his/her room to a RRSP in the other spouse’s name. This is a way to income split in retirement, as future withdrawals, subject to restrictions noted below, would be in the recipient spouse’s name and presumably in a lower tax bracket than the contributor spouse.

The restriction is on the withdrawal timing. If the recipient spouse withdraws any amount from the spousal RRSP in the year of a contribution or the two years following, the amount withdrawn attributes back to the contributing spouse. The only exception to that is a minimum RRIF payment.

In summary the contributing spouse receives the RRSP deduction at his/her current marginal tax rate and the future income is withdrawn at the recipient spouse’s lower tax rate in retirement, maximizing the RRSP tax deferral advantage.

Pension Income Splitting

The pension income splitting legislation introduced in 2007 allowed not only defined benefit pension income to be split between spouses, but also RRIF payments after the age of 65. No matter who owned the RRIF, both spouses could share equally in the income for tax purposes. As the RRIF payment could be divided 50/50 between spouses, the income splitting advantage of the spousal RRSP diminished.

The Case for Spousal RRSPs: Tax Efficient Decumulation

After years of saving, much of today’s tax planning is around decumulating assets. My clients not only want to drawdown their registered accounts but do so in the most tax efficient manner possible. For many, this opportunity often lies in time period between retirement and the receipt of CPP and OAS.

This is one of the most advantageous times to employ an RRSP meltdown strategy. With no further employment income, before receiving government pension income and with presumably little to no other income, RRSP withdrawals can be made with minimal tax consequences. Continue Reading…

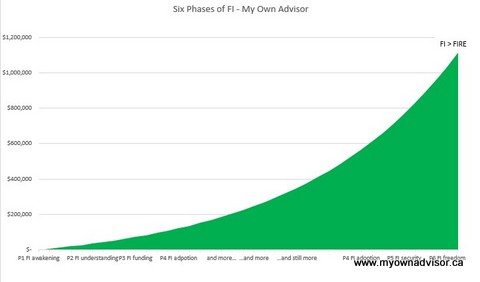

The term “financial independence” has many meanings to many people.

To some, this means the ability to work on your own terms.

To others, it boils down to not working at all but instead having “enough” to meet all needs and possible wants.

Where do I stand on this subject? This post will tell you in my six phases to financial independence.

Retirement should not be the goal: Financial security and independence should be

Is retirement your goal? To stop working altogether? While I think that’s fine I feel the traditional model of retirement is outdated and quite frankly, not very productive.

As humans, even our lizard brains are smart enough to know we need a sense of purpose to feel fulfilled. Working for decades, saving money for decades, only to come to an abrupt end of any working career might work for some people but it’s not something I aspire to do.

With people living longer, and more diverse needs of our society expanding, the opportunities to contribute and give back are growing as well. To that end, I never really aspire to fully “retire”.

Benefits of financial independence (FI)

In the coming years, I hope to realize some level of financial security and eventually, financial independence. For us, this is a totally worthwhile construct. The realization of FI can bring some key benefits:

The opportunity to regain more control of our most valuable commodity: time.

Enhanced opportunities to learn and grow.

Spend extra money on things that add value to your life, like experiences or entrepreneurship.

Whether it’s establishing a three-day work week, spending more time as a painter, snowboarder, or photographer, or you desire to get back to that woodworking hobby you’ve thought about: financial independence delivers a dose of freedom that’s hard to come by otherwise.

FI funds time for passions.

FI concepts explained elsewhere

There are many takes on what FI means to others.

There is no right or wrong, folks: only models and various assumptions at play.

For kicks, here are some select examples I found from authors and bloggers I follow.

JL Collins, author of The Simple Path to Wealth, popularized the concept of “F-you money”. This is not necessarily financially independent sums of money but rather, enough money to buy a modest level of time and freedom for something else.

Various bloggers subscribe to a “4% rule”* whereby you might be able to live off your investments for ~ 30 years, increasing your portfolio withdraws with the rate of inflation.

*Based on research conducted by certified financial planner William Bengen, who looked at various stock market returns and investment scenarios over many decades. The “rule” states that if you begin by withdrawing 4% of your nest egg’s value during your first year of retirement, assuming a 50/50 equity/bond asset mix, and then adjust subsequent withdrawals for inflation, you’ll avoid running out of money for 30 years. Bengen’s math noted you can always withdraw more than 4% of your portfolio in your retirement years however doing so dramatically increases your chances of exhausting your capital sooner than later.

For simplistic math, such bloggers calculated your “FI number” could be approximately your annual expenses x 25. So, if you’re annual expenses are about $40,000 per year (CDN $ or USD $ or other), then your “FI number” is a nest egg value of $1,000,000.

Using that framework, there are levels of FI some bloggers have adopted:

Half FI – saved up 50% of the end goal (in this case, $1 M).

Lean FI – saved up >50% of end goal to pay for very lean but life’s essentials like food, shelter and clothing (but nothing else is covered).

Flex FI – saved up closer to 80% of the end goal, this stage covers most pre-retirement spending including some discretionary expenses.

Financial Independence (FI) – saved up 100% of the end goal, you have ~ 25 times your annual expenses saved up whereby you could withdraw 4% (or more in good markets) for 30+ years (i.e., the 4% rule).

Fat FI – saved up at or > 120% of your end goal (in this case $1.2 M for this example), such that your annual withdrawal rate could be closer to 3% (vs. 4%) therefore making your retirement spending plan almost bulletproof.

There is the concept of “Slow FI” that I like from The Fioneers. The concept of “Slow FI” arose because, using the Fioneers’ wording while “there were many positive things that could come with a decision to pursue FIRE, but I still felt that some aspects of it were at odds with my desire to live my best life now (YOLO).” They went on to state, because “our physical health is not guaranteed, and we could irreparably damage our mental health if we don’t attend to it.”

Well said.

My six phases of financial independence

(Picture from our catamaran cruise, Barbados 2019)

To the “Slow FI” valuable points, since we all only have one life to live, we should try and embrace happiness in everything we do today and not wait until “retirement” to find it. Continue Reading…

Once you’re halfway through retirement, you’d expect about half your savings to be gone, right? This turns out this is very wrong when we don’t adjust for inflation. The return your portfolio generates causes your savings to hold steady for a while and then fall off a cliff.

I read the following quote in the second edition of Victory Lap Retirement:

“A recent Employee Benefit Research Institute study found that people in the U.S. who retired with more than $500,000 in savings still had, on average, 88 percent of it left eighteen years after retirement.”

Frederick Vettese provided further detail. This 88% figure is the median rather than the average.

This statistic was used as proof that retirees aren’t spending enough. After all, if you planned on a 35-year retirement, half the money should be gone after 18 years, right? Not even close. Below is a chart of portfolio size based on the following assumptions.

– annual portfolio return of 2% above inflation

– annual withdrawals of 4% of the starting portfolio size, rising with inflation each year

– inflation of 2.12% (the average U.S. inflation from 2001 to 2018)

So, to be on track for a 35-year retirement, your remaining portfolio 18 years into retirement should be 83% of your starting portfolio size. This is a far cry from an intuitive guess that about half the money should be left.

Still, the earlier quote said the average retiree who started with at least half a million dollars had 88% of their money left 18 years into retirement. Further, thanks to a reader named Dave who found the original EBRI study online, we know that the 88% figure is inflation-adjusted. Continue Reading…

MoneySense.ca: Photo created by freepik – www.freepik.com

My latest MoneySense Retired Money column looks at the topic of whether average savers transitioning to Retirement really need to fear outliving their money. The piece picks up from a blog this summer from Michael James on Money, which will be republished in its entirety tomorrow here on the Hub.

You can access the full MoneySense column by clicking on the highlighted text: How long will your retirement nest egg last? In addition to citing Michael J. Wiener’s work, the piece passes on the views of two prominent recently retired actuaries: Malcolm Hamilton and Fred Vettese, as well as my co-author on Victory Lap Retirement, ex corporate banker Mike Drak.

Like this blog, despite being online the column’s scope is somewhat constrained by a word limit. In fact, in an email, Hamilton told me he didn’t think such a topic could be addressed in just 800 or 900 words.

Actuary and retirement expert Malcolm Hamilton

“Why? We presume that good advice is universal … that it applies to everyone. It does not, particularly when addressing concerns about running out of money. For years I have looked for evidence that large numbers of seniors spent too much and suffered as a consequence. I haven’t found anything persuasive.”

No one knows how much Canadians should save or how quickly they should draw down their savings after retirement, Hamilton added: “Some people are frugal. They save heavily before retirement and spend sparingly after retirement, leaving large amounts to their children when they die. We all want parents like this. Others are spendthrift. They save little before retirement and live frugally after retirement because they have no money except government pensions.”

Finding balance between extremes of Over-Saving and Over-Spending

By Ian Duncan MacDonald

By Ian Duncan MacDonald