By Mark Seed, My Own Advisor

Special to the Financial independence Hub

You could argue beyond the how much do I need to retire question, this need comes up next: how to generate retirement income.

Rightly so.

I mean, we all want to know how best to use our retirement incomes sources wisely. Those retirement incomes sources are necessary to help fulfill income needs, while being tax efficient; income to provide some luxuries now and them, or to potentially deliver generational wealth should that be your goal.

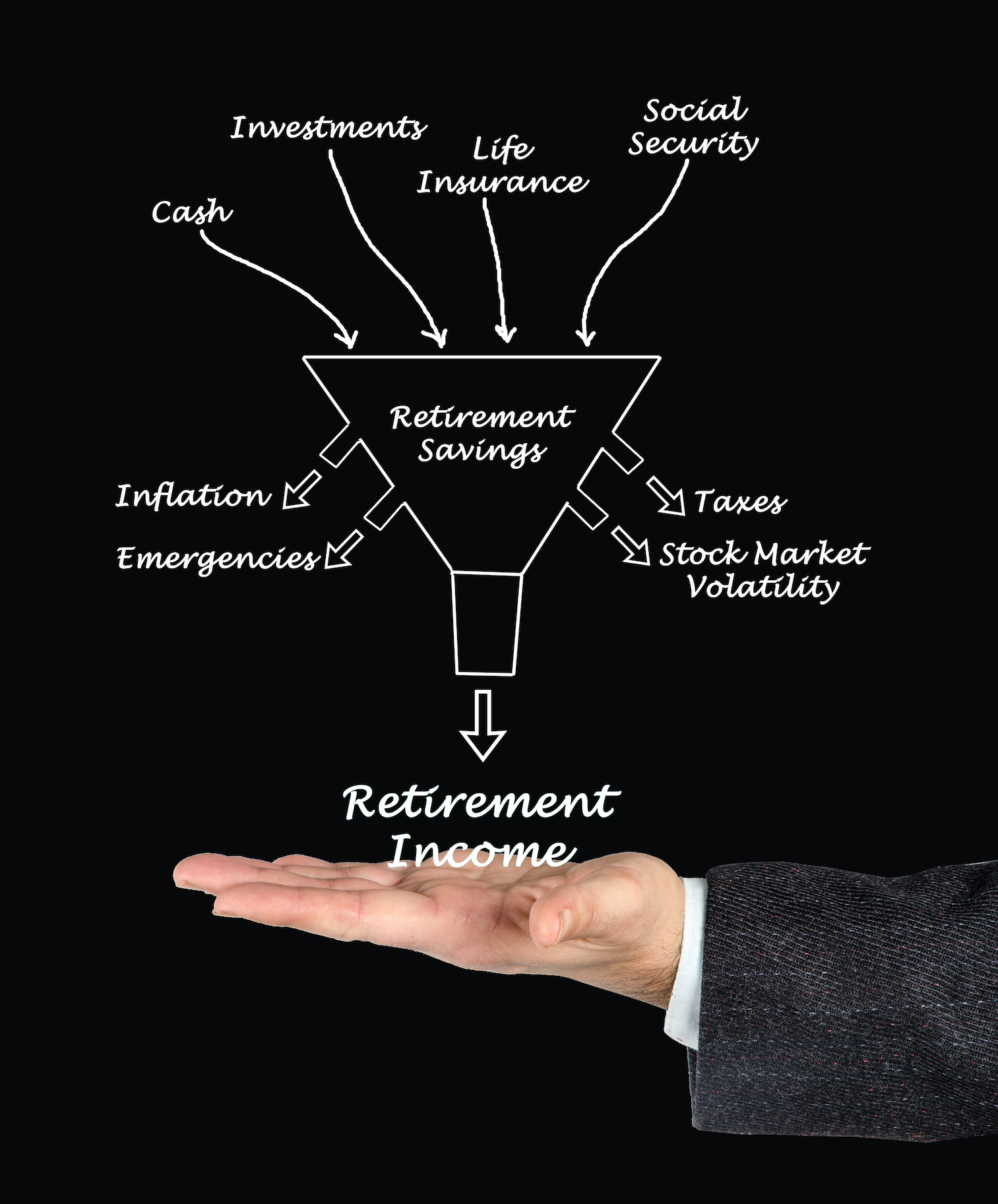

My retirement income plan and options

I’ve been thinking about my income plan, or at least my semi-retirement income plan, for some time now.

I captured a list of overlooked retirement income planning considerations here.

Yet I can appreciate not everyone writes about nor thinks about this stuff.

There are obvious ways to generate retirement income but I suspect some might not appeal to you for a few reasons!

Option #1 – Save more

I doubt most people will like this option but it’s probably necessary for many Canadians: you’re going to need to save more than you think to fund your retirement. This is especially true if you have no workplace pension of any kind to rely on and/or you haven’t assessed your spending needs. More money saved will help combat inflationary pressure, rising healthcare costs and longevity risk. Which brings me to option #2.

Option #2 – Work longer

If you didn’t like option #1, you might not like this one! Working longer into your 60s or potentially to your 70s might be the reality for a good percentage of Gen X and Y. Part of the reasons these cohorts will need to work longer is because many Boomers remain in the workforce so they can fund their retirement. Some Boomers are continuing to work because they enjoy it. Some are continuing to work because they absolutely have to.

Option #3 – Spend less

The 4% rule remains a decent rule of thumb – it tells us we should be “safe” to withdraw approximately 4% of our portfolio with a minimal chance of running out of money.

Using 4%, a retiree would need $1-million invested to produce a steady income of $40,000 a year. Spending less, will absolutely help portfolio longevity and give stocks in your portfolio a longer time frame to run.

Our initial retirement income plan has us leveraging a mix of income streams in semi-retirement:

- Part-time work – to remain mentally engaged – in our 50s.

- Taxable but tax-efficient dividend income.

- Strategic RRSP withdrawals.

I’m not quite “there” yet in terms of other incomes streams, including TFSA withdrawals and exactly when to take those, but I’m working through that.

Generating retirement income

When it comes to you, options abound. You might have similar income streams or other ideas altogether. Remember, personal finance is personal.

I’ve had the pleasure of working with a few advice-only planners on this site and I’m happy to bring back Steve Bridge, a CFP from Vancouver for his detailed thoughts on this subject. Steve works as an advice-only financial planner with Money Coaches Canada (no affiliation with My Own Advisor). You can find him on that site for his services and you can follow him often on Twitter like I do at @SteveMoneyCoach.

Steve, welcome back to chat about this important subject!

Always a pleasure Mark. I love what you do here and I follow your journey. Continue Reading…