Most of your investing life you and your adviser (if you have one) are focused on wealth accumulation. But, we tend to forget, eventually the whole idea of this long process of delayed gratification is to actually spend this money! That’s decumulation as opposed to wealth accumulation. This stage may also involve downsizing from larger homes to smaller ones or condos, moving to the country or otherwise simplifying your life and jettisoning possessions that may tie you down.

Nothing has worked more effectively for the financial industry to justify asset accumulation or AUM (Assets Under Management) than the theoretical underpinnings of the 4% “rule” or “guideline.”

There are innumerable articles on how individuals will require one million dollars or more for retirement based on this dubious principle.

Certainly it is crucial to save but to focus on any particular threshold misses the point that what counts in retirement is a regular, dependable stream of income for a lifetime.

There are two factors in retirement to balance: lifestyle and longevity. Any 4% or otherwise rule is irrelevant if longevity is uncertain. Most people want to maintain a certain quality of life in retirement as well as living healthy.

Here is a hypothetical question: would you take Social Security if it were offered as a lump sum or continue to collect it monthly for the rest of your life (with the bonus of inflation adjusted payouts)? Continue Reading…

Pension incomes are not created equal. They come in all shapes and sizes. They are as varied as the people who have accumulated them and who seek to use them.

In this seemingly infinite variety, in this mathematical complexity, there is a common thread as far as advisors are concerned: delivering clients the most after-tax income possible.

CPP, OAS, Defined Benefit Pension, Dividend Income, Interest Income, RRIFs, Part Time Employment Income, Corporate Dividends, TFSAs: These are just a few of the various sources of income individuals may have access to when they exit the workforce. Upon retirement, decisions about what, when, and how much income to draw upon, move to the forefront.

Tax is key to coordinating multiple income streams

Coordination here is key as each of these sources of income is subject to different tax rates, different tax deferrals and different estate taxes. Tax is key, in other words.

Recent or prospective retirees need more than a competent advisor at this stage. Understanding the tax rates, tax deferral rates and the implications regarding OAS and Income Splitting is one thing. But accounting for these sources of income and the complicated ways in which they interact requires an algorithm.

The specialized software, Cascades, cascadesfs.com, performs these calculations, giving users informed withdrawal strategies. Designed by financial advisors in partnership with software developers, Cascades uses actual tax rates, not average tax rates, projecting for the duration of retirement, including longevity risk.

Because numbers require context to be meaningful, let us consider prospective retirees Bill and Anne Smith.

Case Study: a Couple in their late 60s

Retirement Plan: Bill and Ann are 68 and 67 currently. They have been retired for a few years but still have RRSPs and a LIRA and want to know if they should start using them for income or defer payments until age 71.

Income Sources: Both have CPP and OAS. Anne has a defined benefit pension from having worked as a teacher.

Investments: Bill has a healthy RRSP and Anne has a modest RRSP and a LIRA. They have maxed out their TFSAs and each have about $100,000 additionally in individual non-registered accounts.

Total: 12 different income sources and investment accounts to manage for retirement income

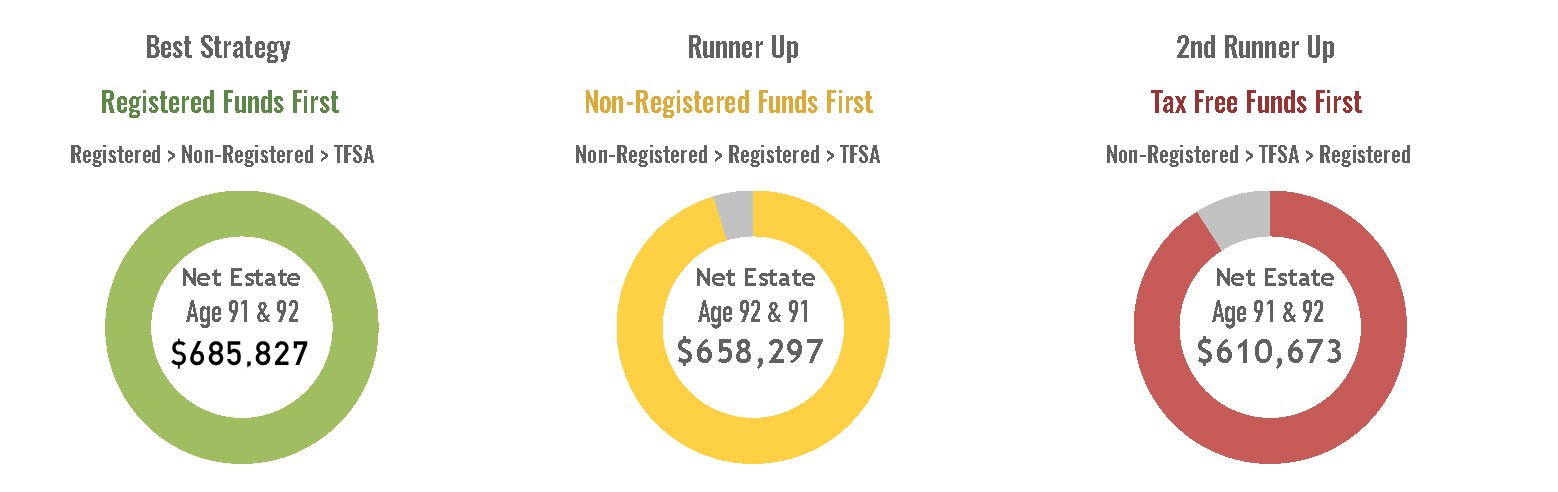

Cascades provides direction in the following way. Users — whether they be Anne and Bill themselves, or their advisors — fill in a detailed online questionnaire, submit their responses and in under ten seconds they have a report. This report (an excerpt is shown at the top of this blog) automatically gives three potential strategies and shows which one works best. For Anne and Bill, drawing down and re-investing their registered accounts first is expected to save them over $75,000 in their estate compared to a complete deferral of their registered money.

As far as Bob and Linda Sanderson are concerned, on the other hand, a Cascades report advises them to do just the opposite and ultimately predicts a savings of $125,000. Here’s how:

Quite different withdrawal recommendations for this younger couple

Bob and Linda are both 55 and currently working. They plan to retire in 10 years. They have a rental property they maintain that they plan to sell in 15 years and want to know how to plan for the long-term.

Income Sources: Both will receive CPP and OAS. Bob will receive a small defined benefit pension. Both will earn rental income until sale of the property. Both will receive corporate dividends until age 80 from a holding company.

Investments: Both have large RRSPs, nearly capped TFSAs, and a small amount of non-registered savings. Additionally, Linda has a small LIRA.

Total: 18 different income sources and investment accounts to manage for retirement income.

Cascades proposes three withdrawal strategies and highlights the best plan. Using all of their non-registered savings before rolling over registered investments will save Bob and Linda over $125,000 in their estate compared to an early drawdown of their registered money. Cascades software is designed to help users do their due diligence on the matter of retirement planning. The results are specifically tailored to the retirement in question and they are reliable, informed and rigorously defined as they are by Canada’s vast and varied tax laws.

.

Ian Moyer is the founder of Ian C. Moyer Insurance Agency Inc. and Cascades Financial Solutions Inc.

Just over 6 months ago I left a job that I truly enjoyed and moved to what I like to call a new life-work stage. I’m not retired; let’s call it a stage of semi-retirement. My RSP and TFSA portfolio was not retirement ready; it’s only halfway there. The acronym FIRE has become very popular over the last few years: Financial Independence Retire Early. I guess I would fit that definition to some degree, but I don’t have that financial part down yet.

I still need to make half a living, and that’s by design.

Many will attempt to sprint to the finish line of retirement. That is, they will work hard and as much as they can so that when they reach that magic age and that magic number (considerable retirement portfolio or pension) they can stop and rest and enjoy that financial freedom. That sounds wonderful, but perhaps troublesome for many. We hear of too many stories of retirees falling ill or passing away within the first few months or years of retirement. There are many physical and biological and psychological reasons for that unfortunate reality. I’ll cover that in a separate article.

Many will take the halfway-to-retirement route and instead of a sprint to the finish line, they’ll stroll to the finish line. That’s me, strolling. The thing is I am walking this walk alone; my wife still works and she wants to work for another 4 or 5 years. She’s ‘not ready to retire.’ And that’s good, we do need her income for now, until I can start to earn half a living. For us to fully retire we would need to downsize from our accidental investment: our Toronto home. Next year we’ll have our 2 kids in University and we want to keep our home as a base and a familiar comfort zone. This is not the time to take off to the beach.

First 6 months of semi-retirement.

Out of the gate the new work-life stage was nothing short of incredible. Last June I packed up the laptop and set up shop in Prince Edward Island. My first home office was a little beach cottage in Stanhope. It was my ‘workcation’. I launched my site from the wonky Wifi of Lyon’s Cottages. The property manager Ken did everything he could to keep that Wifi signal chugging along for 3 weeks.

It was an incredible period, being able to hang out with my daughter who is just finishing up her undergrad work ‘on the island.’ My wife and son joined us for a week of family vacation. That’s a whirlwind of new activities and emotions. Leaving your career and co-worker friends, starting a new business and taking off to Canada’s most lovely beaches. There was a lot of ‘new and exciting’ all rolled into a few weeks.

That said, I got a good taste of that ‘waiting.’ And as Tom Petty (RIP) sang, ‘The Waiting Is The Hardest Part.’ While I have a very generous amount of loner in me I was surprised at how uncomfortable a feeling that was – that working alone and being alone for many hours on end. I couldn’t wait for my daughter to finish work and head up to the cottage for dinner and a walk along the beach.

I couldn’t wait for the rest of the family to join us for that week of family vacation.

I was offered a very quick introduction to the ‘feeling of retirement.’ And I can tell you that is feels a lot different when you are doing that retirement thing – alone. It’s well-known that we have to have a solid plan when we retire. To run to that retirement finish line and then wonder what the heck you are going to do is at the very least misguided. Your time will not magically fill itself with wonderful and fulfilling activities.

When we are working our week is filled with tasks that need to get done on time. We usually know how to fill that time and we often wish there were more hours in the day or more days in the week. Retirement is not much different. We have to fill our days and weeks with tasks and chores and accomplishments. We need some structure. You likely will not be on vacation most weeks or months. Vacation is the easy part, and that may not feel all that different to the vacations that you took in your working life.

That said, I would guess that we can start to take our vacations for granted when those vacations are a regular event. We humans can get used to (and bored with) just about anything. I love to travel with family, that might be my most cherished time. But I think I could get somewhat bored of endless travel, or at least the trips could lose some of the magic. Vacations feel great in our working years because there is anticipation and there is an end date.

Retirement has to have meaning and purpose.

The concept of purpose might be the most important consideration. That word gets used a lot by those who study retirement and retirees. When we lose our purpose that can send a lot of negative signals to our brain and our body. And certainly that purpose can take many shapes and forms. A retiree might look after the grandkids on regular basis, take care of older parents, volunteer, work on a side job that includes a useful mission.

If you are retiring alone for a few years, waiting for your partner, you’d best have a very good plan built around that purpose. And you might want to fill your 9-5 Mondays to Fridays with enough contact with others – engaging human contact. Free time to do ‘nothing’ loses its appeal real quick. It’s not all that special when free time is followed by more free time.

Make the most of your time when you are waiting for your spouse to retire. I’d suggest that the real retirement starts when you are both retired. But you can make the waiting years very enjoyable and fruitful and meaningful.

Retirees who are doing it right.

Fritz Gilbert at Retirement Manifesto retired the same month, June of 2018. He offers a wonderful blog that details his and his wife’s FIRE journey. Here’s 6 Lessons From The First 6 Months of Retirement.

You’ll find their retirement consists of a lot of structure and a lot of purpose. There’s regular exercise. There are Grandkids and dogs to take care of. It’s busy enough. There’s lots of room for vacations. As much as one can try to prepare, Fritz is also surprised by the new venture known as retirement.

I’m Lucky

I semi-retired with a purpose, my blogand other writings that help Canadians with their own search for FIRE and other financial goals. That’s all very exciting and interesting and rewarding. But I know I need more. I need to get ‘out there’ more to promote the blog and mission and to reach Canadians face to face. I will also add some volunteer work for more tasks and greater purpose.

My first 6 months of semi retirement reinforced what is well-known, that being financially prepared is only half of the prep work that is required for a successful and happy retirement. Retirees need a plan. A newlife plan for your newlife.

Money + Plan = FIRE-AH.

Financial Independence Retire Early – And Happy.

Kindly hit those share buttons for Twitter, Facebook and Linkedin at the bottom on this article. And for my 6 month anniversary present, kindly click Follow Cut The Crap Investing at the very bottom of this page.

Dale Roberts is the Chief Disruptor at cutthecrapinvesting.com. A former ad guy and investment advisor, Dale now helps Canadians say goodbye to paying some of the highest investment fees in the world. This blog originally appeared on Dec. 11, 2018 and is reproduced here with his permission.

Is your job failing to provide you with money to spend on the things that you always wanted to have for yourself? Since you most likely have free time other than the typical eight hours of sleep per day, you should use it to earn additional income.

If you need further convincing as to why you should seek to build a source of income aside from the one that your current job provides, you should consider talking to a financial advisor or planner like those from Capstone who can walk you through the nitty-gritty of how to plan out your finances going forward. But if you already want to get straight to it, here’s how you can create a supplementary source of income:

Build an online store

Shopping online has become a common activity for some, especially those with tons of money to spend but don’t want the inconvenience of driving into town. However, instead of settling at becoming an online shopper yourself, why not try selling products via the Internet?

You might want to consider registering a seller account first at an e-commerce platform such as Amazon or eBay. You can set up shop in your chosen e-commerce platform in only a matter of minutes, thus allowing you to focus more on spreading the word about your online store and targeting potential buyers.

Once you’ve established yourself as an online seller, you can then consider creating a dedicated website for your onlinestore where you can have fuller control of all the profit generated by your side business. Just remember to retain your day job for the time being until you can already live comfortably using the earnings that your online store receives.

Work as a Freelance Writer

You may have a knack for writing about anything under the sun, but your current job might find you doing anything but that. However, since you don’t spend your entire day working at your job, you can use your free time in an income-generating way by rekindling your passion for writing and finding work as a freelance writer.

Website owners and bloggers who find very little time to write content – especially if they have a hectic schedule – often hire freelance writers and pay them to create articles and posts. Once you become a freelance writer for a website owner or blogger, your research skills will be put to the test, thus making you learn more about specific topics in a more active way compared to when you stumble upon a random article on the Internet and read it in your spare time. Best of all, you can work anytime you want as a freelance writer. Continue Reading…

It’s no secret that many Canadians think about escaping the cold winter months for some place warmer. While some may like to spend their vacation days relaxing beside the beach or pool, boomers are increasingly seeking out unforgettable travel experiences.

While embracing bucket list travel might mean trying new things off the beaten path, like driving a Ferrari in Italy, hiking the Inca Trail or helping build clean water wells in Africa, there’s always a risk that adventure could turn into misadventure. A recent TD Insurance survey revealed more than a third of Canadian boomers who travel annually say they or someone they’ve travelled with has had a travel emergency, such as an injury that required a trip to the doctor.

The survey also revealed many boomer travellers report they don’t purchase travel insurance because they’re already covered under their work benefits or credit card. Although existing travel insurance plans may cover certain travel emergencies, it’s important to take the time to review them for any gaps in coverage, especially if you’re planning activities you haven’t tried before, and purchase supplementary coverage if needed.

For Boomer travellers setting out to check off their travel bucket list items, here are a few more pre-travel tips, so your epic adventure can be exactly that:

1.) Follow your interests

What’s on your travel bucket list is very personal and will vary widely depending on your interests. Do you want to test your physical limits by hiking along the Great Wall of China? Do you dream of seeing the annual migration on the Serengeti Plains? Bucket list travel are trips of a lifetime, so take the time to not only decide what you want to see or do, but also properly prepare in advance of your travels.

2.) Pre-departure prep

Proper preparation is key to making your bucket list trip terrific. Prepay or set up autopayments for bills that will be due while you are away. Verify whether you need any vaccinations for where you’re travelling to. Ensure you have enough prescriptions to last the trip. There’s lots to be done ahead of time so that your bucket travel is as dreamy as imagined. Check out TD Insurance’s Travel Checklist for more tips. Continue Reading…