Happy Canada Day!

Happy Canada Day!

Just in time for America’s Independence Day, I’m happy to announce that a new updated 2021 edition of Findependence Day is now available in the US market. Published by Best Books Media in New York, you can buy the paperback version of the book here through Amazon.com.

Or you can buy the new paperback for US$15.99 or Nook ebook for US$1.99 at Barnes & Noble.

Below is an Interview with Myself, which explains the timing, the differences and other things. If “An Interview with Myself” strikes some as a little bizarre, let me acknowledge that I originally got that idea from British journalist and author Malcolm Muggeridge, who I knew when he was the Writer in Residence at the University of Western Ontario journalism school in 1978-1979.

So without further ado, here’s the Q&A with myself:

Jon Chevreau: So Jon, you already had an American edition out in 2013. Why are you updating it eight years later?

Jon Chevreau: So Jon, you already had an American edition out in 2013. Why are you updating it eight years later?

Jon Chevreau: Good question, Jon, it’s mostly a matter of timing and the fact that North America, led by the United States, is just starting to emerge from the Covid pandemic. Suddenly, young people are starting to have hope again about their futures, including their financial futures. And, Findependence Day is a novel geared to younger adults, millennials, people just starting out on their life’s journey.

JC-Q: I see. I know Canada is a bit behind the USA in its vaccination program and economic recovery, but why a new US edition and not a new Canadian edition?

JC-A: True but the fact is that while the original Canadian edition has sold well and continues to sell in Canada, the original print run was such that there are still enough copies left that it doesn’t make much sense to make the old version obsolete. And besides, the content in the Canadian edition is still current.

As you know, Jon, the first edition from 2008 was actually written as a North American edition and attempted to include both Canadian and American content. But you decided a few years ago that the US market — which after all is ten times as large — needed its own edition with no reference at all to Canada or to Canadian financial content.

JC-Q: How do the different editions differ?

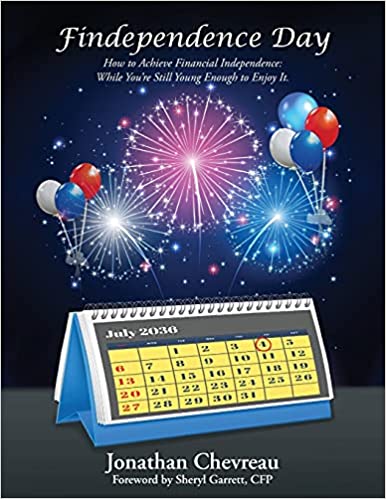

JC-A: Well, both the 2013 Trafford U.S. edition and the updated 2021 Best Books US edition are what I wanted the original edition to be. The cover concept was always the one you see above: it’s just that when Power Publishers published the first edition, the design team there went with the cover concept of the red balloon in the blue sky.

JC-A: Well, both the 2013 Trafford U.S. edition and the updated 2021 Best Books US edition are what I wanted the original edition to be. The cover concept was always the one you see above: it’s just that when Power Publishers published the first edition, the design team there went with the cover concept of the red balloon in the blue sky.

JC-Q: But you really wanted the image of a calendar set in the future, circling July 4th as the Findependence Day selected by one of your main characters?

JC-A: Correct. The 2013 and 2021 covers are quite similar although Best Books slightly reworked it and we changed the futuristic date from 2027 to 2036.

JC-Q: So the protagonist, Jamie, still has 15 years to achieve his dream of Financial Independence while he’s still young enough to enjoy it?

JC-A: Quite right, Jon.

JC-Q: Any other big differences?

JC-A: Well, the other thing the two US edition incorporated was something some people suggested I include in the original Canadian edition but chose not to at the time. That’s the chapter summary at the end of each chapter of the key lessons that Jamie and his wife Sheena learned. The new 2021 edition retains that feature and updates some of the financial info.

JC-Q: How do you categorize Findependence Day? Is it non-fiction or is it fiction?

JC-A: I wish you hadn’t asked that one, Jon because that’s a tough one to answer. In truth, it’s a hybrid of fiction and non-fiction, which I realize is a bit unusual.

JC-Q: So which is it, if you put a gun to our head?

JC-A: First, I’d say please remove the gun. Second, I’d say it’s primarily a novel but a financial novel.

JC-Q: Like David Chilton’s The Wealthy Barber and its many imitators?

JC-A: Sure, David Chilton established this genre way back in 1989 and no one has sold more copies than him in that niche. Incidentally, David has told us he “believes” in Findependence Day and that it is “excellent.” You can find that among the many laudatory testimonials the book has gathered over the years.

JC-Q: So why the hybrid and how does Findependence Day differ from all those other Wealthy Barber knockoffs?

JC-A: Well, most of the imitators tend to be what I call “information dumps” — the focus tends to be on the financial information and the stories around them tend to be a bit thin when it comes to characterization, plot etc.

JC-Q: And Findependence Day isn’t?

JC-A: We tried to bring traditional novel-writing structure and techniques into the book so that the young people who are its target audience would first be entertained and drawn in sufficiently that they’d want to see what happened to Jamie and Sheena. Yes, we sprinkle in the financial info as the plot proceeds but not at the expense of Story. So the minute any financial dump starts to sound contrived and unlikely to occur in real life, we cut it short and returned to the story.

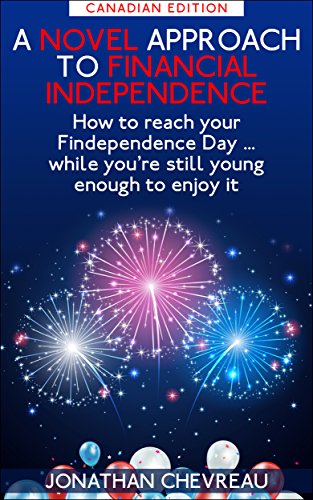

That’s another reason for the end-of-chapter summaries and incidentally the reason we also created two Amazon ebooks that summarize the plot and reprise the end-of-chapter summaries. They cost just $2.99: they’re called A Novel Approach to Financial Independence. (one for Canada, the other for the US)

That’s another reason for the end-of-chapter summaries and incidentally the reason we also created two Amazon ebooks that summarize the plot and reprise the end-of-chapter summaries. They cost just $2.99: they’re called A Novel Approach to Financial Independence. (one for Canada, the other for the US)

JC-Q. In short, we tried to write a “real novel.”

JC-A. We did try and many reviewers seemed to think we pulled it off. One financial planner, Diane McCurdy, said Findependence Day is “the closest you’ll come to a great beach book that helps you make enough money to retire!”

JC-Q: How is it a beach read? Continue Reading…