By Penelope Graham, Zoocasa

Special to the Financial Independence Hub

The past two years have been tumultuous times for the Ontario real estate market. Not only have prospective home buyers had to contend with the nationally-implemented mortgage stress test, but a round of policies introduced at the market’s peak have contributed to a vastly different price environment in some of the province’s municipalities.

Called the Fair Housing Plan, this 16-part set of measures was introduced by the former Liberal provincial government with the intention of rebalancing supply and demand as well as out-of-control price growth. It was announced in April 2017, prompted by a year-over-year home price spike of over 30% in the Greater Toronto Area.

New rules spooked sellers

The tangible measures included a 15% foreign buyers’ tax as well as beefed up rent controls, the resulting market chill was likely psychological. Sellers, concerned they had missed the market’s price peak, reacted by flooding MLS with listings while buyers waited to see if the opportunity to get into the market at a lower price point would present itself.

That combination, along with the impact from the stress test — which requires borrowers to qualify for a mortgage roughly 2% higher than the actual rate they’ll get from their bank — effectively led to a housing correction. (Text continues below the ad)

However, in the two years since the measures were introduced, the dust has largely settled in markets across the province; though some cities have weathered them better than others, according to new data from Zoocasa.

Some markets harder hit than others

The study, which compares average sold home prices in April 2017 to the same month this year, reveals which markets have sustained an overall drop in home values, while others have actually continued to appreciate. It also examined the sales-to-new-listings ratio in each municipality, which is a metric used by the Canadian Real Estate Association to determine the level of competition in the market. A ratio between 40 and 60% can be considered a balanced market, while below and above that threshold indicate buyers’ and sellers’ conditions, respectively. Prices were sourced from various real estate boards across the province.

Of all the Ontario housing markets, those located in York Region have absorbed the brunt of the new measures, with steep price declines and a considerable change in buyers’ conditions over the two-year time period.

Home prices in the city of Newmarket, for example, have plunged -30% over the 24-month period, dragging the average below the $1-million mark to $725,710. That decline was prompted by a -31% drop in sales; however, as the supply of new listings also declined by -42%, market conditions actually tightened to a ratio of 45% from 37% last year, well within balanced territory, despite the lower price point.

The City of Aurora also saw prices fall by -30%, down to $888,387, following a -35% drop in sales and a -30% drop in new listings, leaving buying conditions unchanged at a ratio of 42%. The community of Richmond Hill also experienced a significant price drop of -27%, though still remains at a high-priced $1,016,216. It remains in a sluggish buyers’ market with a ratio of 38%, down from 40% in 2017.

Prices for Oakville homes for sale were also among the most affected, dropping -18% over the last two years to an average of $1,019,751. However, the market remains balanced with a ratio of 46%. However, homes in some municipalities, such as on the Hamilton MLS and in the Mississauga real estate market, were impacted by a far lesser extent; both cities saw values fall just 4%, to $528,286 and $767,283, respectively. In contrast, conditions are more favourable to sellers in these markets, with ratios of 63% and 59%.

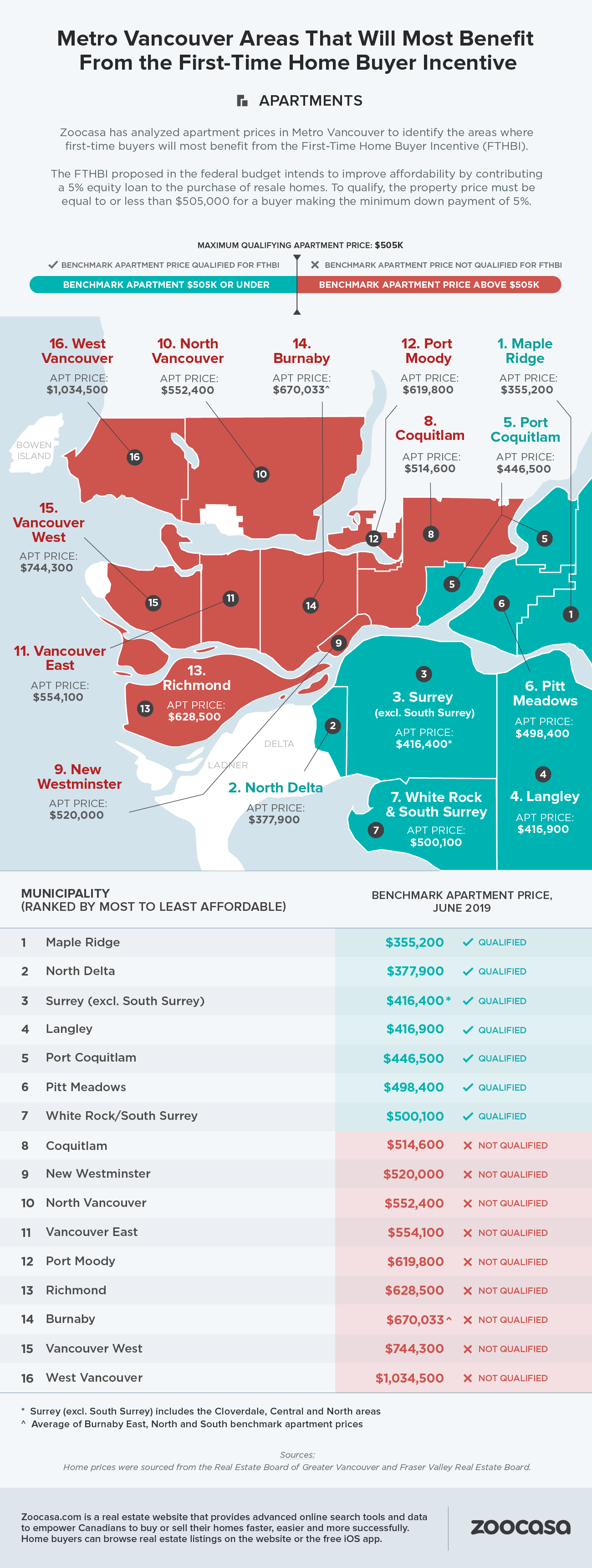

Check out how prices and market conditions have changed across Ontario between April 2017 and 2019 in the adjacent infographic.

Penelope Graham is the managing editor of Zoocasa.com, a real estate resource “that uses full brokerage service and online tools to empower Canadians to buy or sell their home faster, easier and more successfully.”

Penelope Graham is the managing editor of Zoocasa.com, a real estate resource “that uses full brokerage service and online tools to empower Canadians to buy or sell their home faster, easier and more successfully.”

By Penelope Graham, Zoocasa

By Penelope Graham, Zoocasa