While investing in technology companies can be lucrative, it’s also risky. With great risk comes great reward, so the saying goes. However, not everyone has the luxury of risking their savings. Is there a way to maximize returns while minimizing risks?

Volatility is the Name of the Game in the Tech Sector

The COVID-19 pandemic was a catalyst for exponential growth. Venture capital (VC) activity set records in 2021. In the United States, VC-backed businesses raised around $329.9 billion, almost doubling 2020’s $166.6 billion in funding. Approximately $774.1 billion in annual exit value was created that year.

The potential for high returns is tempting, but this trend has slowed as peoples’ reliance on technology has waned. Startups are burning through their cash reserves. Those looking to make money from the tech sector should be strategic about their investments.

In the tech sector, volatility can make investors disgustingly rich — or cause them to lose everything. Technological advancement, driven by fierce competitiveness, happens fast, frequently disrupting the status quo. This allows unknown disruptors to rise to the top quickly.

Take DeepSeek, for example. A Chinese artificial intelligence company built an open-source large language model (LLM) of the same name to compete with ChatGPT for a fraction of the cost. NVIDIA stock — which has risen 285 times higherover the last 10 years — was down nearly 17% on the day this new competitor was unveiled.

Rumor has it DeepSeek was built for drastically less with subpar technology, which makes its disruption all that more consequential. While analysts expected OpenAI’s revenue would exceed $11.6 billion in 2025, it may not be so lucky. The AI companies dominating the market have just been undercut, affecting investments thought to be relatively safe.

How Rapid Innovation can lead to Substantial Gains

The tech sector thrives on innovation because technology goes hand in hand with modernity. The industry is also fiercely competitive, driving research and development. Continual reinvention provokes disruption, making this landscape fertile ground for dramatic, abrupt growth. Often, firms don’t have to fight hard to break into new markets.

Investing in a Volatile, High-Growth Sector is Risky

Market volatility won’t always work in your favor. Even industry giants — seemingly unshakable leaders — can fall to a previously unknown disruptor. Think back to DeepSeek’s impact on NVIDIA. Everything from changing market conditions to regulatory changes can quickly sour a strong investment.

Take Zoom, for example. Zoom didn’t see widespread adoption until the COVID-19 pandemic when it ousted Skype as the most well-known videoconferencing platform. Its share price peaked at $559 in October 2020. One month later, Pfizer and BioNTech announced a vaccine candidate against COVID-19. The next day, it dropped to $403.58. Since then, it has further plummeted, remaining just above $50 for much of 2023 and 2024. Continue Reading…

Theatrical release poster for the film, Idiocracy. via Wikipedia.

By Mark Seed, myownadvisor

Special to Financial Independence Hub

A few months ago I wrote:

“Yes, interesting times may call for interesting portfolio changes! Or not. :)”

Well, here we are.

Regardless about how you feel about the current U.S. Administration, I would think most people would agree that this U.S. President feels very emboldened right now. With no future term to go: this is his last shot at taking shots at pretty much anything and everyone he wants without too many consequences near-term. At least it seems that way …

Since writing this post below from December I thought I would update such a post about any recent portfolio changes and beyond that, how our shopping habits have shifted (if at all) in recent months.

How to invest and shop during Trump idiocracy

I put the term “idiocracy” in the post title since it’s very much how I feel right now.

It’s like watching the Ferris Bueller movie scene: on tariffs.

History repeats.

Now that tariffs are in place and we’re now in a (trade) war between Canadian and U.S. businesses, consumers and workers (sadly), I’m expecting these tariffs will roil stock markets for months or years to come.

I have.

This is how I intend to invest and shop during some prolonged Trump idiocracy.

Approach #1 – What investments can withstand stagflation?

New tariffs are likely, in my opinion, to trigger a sustained period of low economic growth and even higher inflation: which will impact everyone.

At the most basic level, inflation means a rise in the general level of prices of goods and/or services over a period of time. When inflation occurs, each unit of currency buys fewer goods and services. Inflation results in a loss in the value of money and purchasing power. We will all be impacted by this.

Stagflationis essentially a combination of stagnant economic growth, high unemployment, and high inflation. When you think about it …. this combination probably shouldn’t exist: prices shouldn’t go up when people have less or no money to spend. This could be a place where things are trending…

Farmland might perform well during stagflation but we don’t own any.

Instead, I own some “defensive stocks” including some in key economic sectors like consumer staples, healthcare and utilities in my low-cost ETFs that should be able to weather a prolonged disruption. I also consider a few selected stocks we own as defensive plays: waste management companies. At the time of this post, both Waste Management (WM) and Waste Connections (WCN) we own have held up very well and provided stellar returns over the last 5+ years that I’ve owned them.

WM is up almost 100% in the last 5-years.

WCN is up over 100% in the last 5-years.

We’ll see what the future brings and my low-cost ETFs are a great diversifier: regardless.

Approach #2 – Staying global while keeping cash

Beyend certain sectors, investors should always consider holding a well-diversified stock portfolio across different sectors and different economic regions to reduce the long-term reliance on industries directly affected by tariffs.

While I have enjoyed a nice tech-kicker return from owning low-cost ETF QQQ for approaching 10 years now, and I will continue to hold some QQQ in my portfolio, I could see technology stocks tanking near-term. To help offset that, I own some XAW ETF for geographical diversification beyond the U.S. stock market. Thankfully.

Times of market stress are however times to buy stocks and equity ETFs.

Near-term and long-term investing creates buying opportunities for disciplined investors. A well-structured, diversified global mix of stocks including those beyond the U.S. could provide some decent defence against a very toxic, unpredictable economic and political agenda.

For new and established readers on this site, you might be aware I’ve mentioned that our investing approach could be considered a “hybrid approach” – a structure that was established about 15 years ago as follows:

We invest in a mix of Canadian stocks in our taxable account: to deliver income and some growth, and

Beyond the taxable account, we own a bunch of low-cost ETFs like QQQ and XAW inside our registered accounts: inside our RRSPs, TFSAs and my LIRA for extra diversification.

I like the hybrid approach, the process and the results to date.

At the time of this post, I just don’t see how I should be making any significant changes to our equity portfolio.

Beyond our portfolio of stocks and equity ETFs we keep cash/cash equivalents.

Cash savings remains a good hedge for a very uncertain near-term future. We have a mix of Interest Savings Accounts (ISAs) / High Interest Savings Accounts (HISAs), along with Money Market Funds (MMFs) in particular in our registered accounts. Generally, plain-vanilla savings accounts offer very low interest rates. So, if you want to earn more on your savings deposits (rather than simply using your savings account) then consider an ISA or HISA.

The greatest appeal of ISAs and HISAs for taxable savings IMO is liquidity, while earning interest, and member financial institutions of Canada Deposit Insurance Corporation (CDIC) insure savings of up to $100,000. It’s good business for banks and institutions as well since money deposited generates interest by allowing the bank to access those funds for loans to others. There are usually no fees for these accounts and while interest rates have come down in recent months, ISA and HISA interest rates are consistently north of 2% at the time of this post.

I believe some form of savings account / ISA / HISA remains the cornerstone of everyone’s personal finance portfolio since 1. your money is saved for future expenses or ready for emergencies, 2. it is safe/low risk, 3. it is liquid, and 4. you still earn returns.

Let your equities do as they wish after that.

Approach #3 – Shop local, buy local, and avoid U.S. travel

We are fortunate to live in an area in Ottawa where we can shop local and buy from local farmers. We will continue to do that.

For those that want to shop more in Canada and buy more Canadian goods visit here:

We’ve been fortunate to save up some money in our “sunshine fund” as I call it for some future travel. I/we have no near-term plans to spend our money in the U.S.

I’ve been fortunate to visit many, many U.S. States over the years but given this recent trade war initiated by this current U.S. Administration I hardly have any desire to spend my money in a country whereby that government talks about annexing us.

It’s that simple for us.

I encourage other Canadians who can and do travel, to consider the same – avoiding the U.S. – not because of its citizens but the U.S. Administration decisions. Continue Reading…

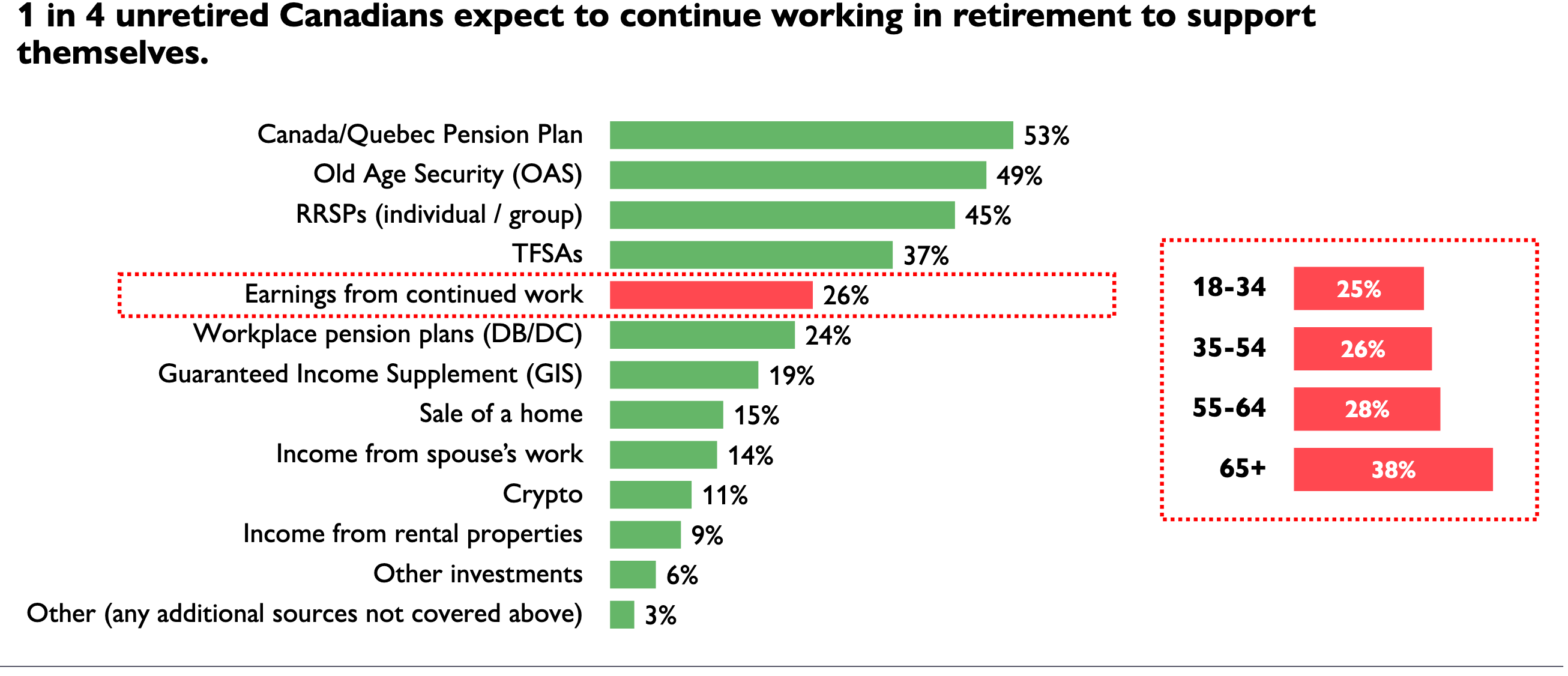

Even before the Tariffs threats emerged under Trump 2.0, Canadian seniors were starting to find the economic uncertainty and rising living costs to be unmanageable. No surprise then that many seniors approaching Retirement Age are delaying their exit from the workforce.

According to a report by HealthCare of Ontario Pension Plan, 28% of unretired Canadians aged 55-64 say they expect to continue working in retirement to support themselves financially. Here’s a screenshot from the HOOPP survey:

The Healthcare of Ontario Pension Plan (HOOPP) commissioned Abacus Data to conduct its sixth annual Canadian Retirement Survey in the spring of 2024. The latest survey finds “persistent high interest rates and a rising cost of living continue to have a significant negative impact on Canadians’ ability to save and manage the cost of daily life, threatening their retirement preparedness.” While all Canadians are struggling, “women and those closest to retirement are especially hard hit with lower savings and higher levels of financial stress.”

While most Canadians are struggling to save amidst a high cost of living, HOOPP finds women are particularly affected. Half (49%) of all Canadian women have less than $5,000 in savings and almost a third (28%) have no savings (compared to 33% and 17% of men, respectively), similar to the 2023 results

The MoneySense column also looks at more recent Retirement surveys that also reveal anxiety about rising costs of living. One is from Bloom Finance Co. Ltd., conducted by founder Ben McCabe after Trump’s Tariffs started to kick in this year.

A Bloom study conducted with Angus Reid found 46% of Canadians thinking of working part-time in Retirement. That’s in line with a Fidelity survey in 2024 that found half of Canadians plan to delay Retirement. According to the Bloom Report [in March 2024], 67% of Canadian homeowners over 55 were concerned their savings would not sustain their quality of life through retirement. Only 29% considered downsizing or alternative living situations to access their home equity earlier than expected. 59% of the same cohort agreed accessing micro-amounts of their home’s equity would help maintain their desired living standard. Continue Reading…

Many people like to say that passive investing doesn’t exist. However, these people make a living from active forms of investing and are just playing semantic games to distract us. Active fund managers and advisors who recommend active strategies are the main people I see claiming that passive investing doesn’t exist, but what they say isn’t true.

There is a continuum between passive and active investing; they are not absolute properties. We can reasonably call an investment approach passive even if it involves some decisions, just as we can call a person thin even if their weight isn’t zero. We may disagree on the exact threshold between passive and active investing, but the concept of passive investing still has meaning.

By “passive investing,” most people mean some form of broadly-diversified index investing with minimal trading. Although passive investing usually requires substantially less work than active investing, passive investors still have decisions to make. They need to choose an asset allocation, funds, accumulation strategy, rebalancing strategy, decumulation strategy, etc. The term “passive” comes from the fact that there is no need for day-to-day or even week-to-week decisions. It’s possible for passive investment to run on autopilot for a year without adjustment. In contrast, more active strategies need closer attention.

Threat to Active Fund Management

The rise of passive investing is a threat to active fund management. Even factor-based investing that leans toward the passive end of the continuum is threatened by more passive forms of investing. It’s hard to argue against the success of broadly-diversified index investing with minimal trading. So, rather than trying to argue in favour of more active strategies, it’s easier to meander into a pointless discussion about how passive investing doesn’t really exist. Continue Reading…

To apply this approach, at the end of each year, you pick the 10 stocks with the highest dividend yields from the 30 stocks that make up the Dow index.

You then invest an equal dollar amount in each of these 10 stocks and hold them for one year. You repeat the selection process and re-jig the portfolio at each year-end.

In theory, these stocks should outperform the market (the DJIA or the S&P 500).

2. The Small Dogs of the Dow Approach

In another variation, you pick the 10 highest dividend-yielding stocks, then select the five with the lowest stock price. Invest an equal dollar amount in each of those, hold them for a year, and repeat. This variation is known as the Small Dogs of the Dow, or simply The Dow 5.

Here’s a Dogs-of-the-Dow ETF

The ALPS Sector Dividend Dogs ETF (symbol SDOG on New York) follows its own version of the Dogs-of-the-Dow strategy. It picks five stocks with the highest dividend yields from each of the 10 sectors of the S&P 500 index. These sectors are consumer discretionary, consumer staples, energy, financials, health care, industrials, information technology, materials, telecommunication services, and utilities.

Each holding begins with roughly the same dollar value, so every company starts out with a similar influence on the ETF’s total return. The end result is a portfolio of 50 large-cap stocks.

Currently, the fund now holds a number of stocks we recommend as buys for subscribers of our Wall Street Stock Forecaster advisory. They include AT&T, Verizon, Kraft Heinz, Snap On, 3M, Newmont Mining and IBM. However, the ETF also holds a lot of stocks we don’t recommend.

Should you Follow the Dogs of the Dow Approach?

One best-selling book of the early 1990s advised investors to buy the Dogs of the Dow: the lowest-priced, highest-yielding Dow stocks. Followers of the approach made money. Of course, anybody who bought stocks in the early 1990s made money.

The Dogs of the Dow strategy worked well in the 1990s because interest rates were going down. This tended to raise all stock prices. But high-yielding stocks were affected more than most because they attracted bond investors who were switching into stocks.

That’s how things work with most formulaic approaches: Sometimes they seem to add value, because they happen to lead you to invest in stocks that were likely to go up for some reason other than the formula’s actual focus.

Of course, you also need to keep in mind that high yields can signal danger, rather than a bargain.

All in all, we don’t recommend the Dogs of the Dow strategy.

Here’s why high yields can be a danger sign

To reiterate: a high dividend yield may be a danger sign. It may mean insiders are selling and pushing the price down. A falling share price makes a stock’s yield goes up (because you still use the latest dividend payment as the numerator to calculate yield: but the denominator, the price, has dropped). But when a stock does cut or halt its dividend, its yield collapses. Continue Reading…