Last thing I remember

I was running for the door

I had to find the passage back

To the place I was before

“Relax, ” said the night man

“We are programmed to receive

You can check out any time you like

But you can never leave”

Hotel California, by The Eagles

By Noah Solomon

Special to Financial Independence Hub

I recently met with an acquaintance who does investment due diligence and manager research for a wealth management firm. During our conversation, he told me about a bond fund which had been garnering substantial assets from investment advisors.

After the meeting, I investigated the fund. Unsurprisingly, the fund had delivered very strong returns, outpacing almost any competitor. Upon digging deeper into the fund, the saying “Not all that glitters is gold” came to mind. The fund’s portfolio consists largely of high-yielding, lower-quality, relatively illiquid corporate bonds. Notwithstanding its strong performance, I determined that the fund is not particularly attractive. As I will explain, this determination was based on the simple reason that the fund is unlikely to serve the primary function of bonds within investors’ portfolios.

Plumbers, Electricians and Bonds

In my view, the crucial function of bonds is to mitigate overall portfolio losses during equity bear markets. While some bonds have low correlations to equities and can therefore offset stock losses in bear markets, others lack this critical feature.

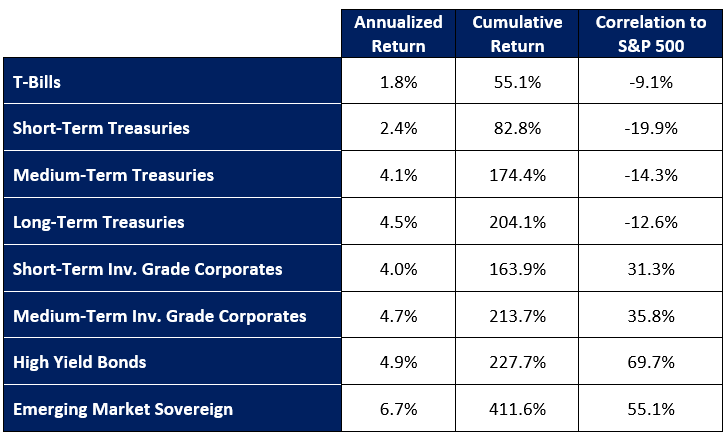

Return vs. Correlation to Stocks by Bond Type: 2000 – 2025

At one end of the spectrum, U.S. Treasury bonds tend to be least correlated to stocks. In the middle of the pack lie investment-grade corporate bonds, which tend to move in tandem with equities. At the other end of the spectrum lie high-yield and emerging-market sovereign bonds, which have the greatest correlation to stocks and thus offer no ability to serve as a shock absorber during bear markets.

Investors don’t hold bonds to achieve strong returns: stocks are much better at that, especially over longer time horizons and even more so once taxes are considered. Owning higher-return bonds that are more correlated with stocks is akin to calling an electrician to fix a plumbing issue. Not only would an electrician fail to rectify the issue, but they might even make matters worse. Similarly, not only can corporate bonds fail to diversify portfolios at critical junctures but can contribute to portfolio losses in bear markets.

Don’t get me wrong. All else being equal, higher returns are better than lower ones. Although bonds with higher correlations to stocks have delivered higher returns than those with lower correlations, this is insufficient compensation for their inability to diversify equity exposure. Bonds are first and foremost portfolio diversifiers, not return generators. If given the choice between a bond portfolio with higher returns that is more correlated to stocks and one with a lower return that is uncorrelated, I would choose the latter every time.

Corporate Bonds: A Fairweather Friend

English Poet Alfred, Lord Tennyson wrote “So vanish friendships only made in wine.” This saying can be applied to corporate bonds, which seem like a great idea in good times and anything but in tumultuous markets. When it comes to their higher returns and their ability to offset stock losses in bear markets, corporate bonds are a fairweather friend: they can abandon you in difficult times.

The correlation of corporate bonds to stocks tends to become more pronounced during times of market stress, which can result in unpleasant surprises when, rather than offsetting stock declines in bear markets, they become part of the problem. Alternatively stated, their diversification powers vanish when they are most needed. While this is the case with corporate bonds in general, it is particularly true of lower-quality high-yield bonds.

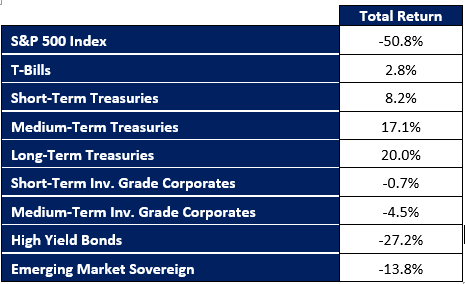

Global Financial Crisis: Performance by Bond Type

During the global financial crisis, while Treasuries of all durations provided some ballast within balanced portfolios, other segments of the bond market failed to do so, with high yield and emerging market bonds suffering substantial losses.

Forbidden Fruit and the Hotel California

There is no shortage of bond managers who strive to outperform by eating forbidden fruit, which entails holding portfolios with more credit risk and a higher correlation to stocks than their benchmark indexes.

This tactic works until it doesn’t. During “normal” markets, such managers will deliver higher returns than their benchmarks. Moreover, their higher correlation to stocks is of no concern when stock prices are rising. However, when bear markets materialize (which sooner or later they always do), their outperformance turns into underperformance. Perhaps more importantly, their higher correlations to equities render ineffective in mitigating stock losses exactly when you need them to. Rather than being a solution they become part of the problem! You might just as well own low-volatility stocks: if you’re not getting any diversification benefit you should at least reap a better after-tax return. Continue Reading…

By Dale Roberts, Retirement Club/cutthecrapinvesting

Special to Financial Independence Hub

It appears to be an overlooked part of retirement planning. While we should always invest within our risk tolerance level we should also match our investment portfolios to the retirement cash flow plan. The plan gives the marching orders for each account. If you create a portfolio-to-plan mismatch, you could increase the risk of depleting an account too soon. On the other side if you are too conservative where an account has the time horizon to run, you create opportunity cost. You missed the opportunity to create significantly more wealth over time.

As always the following is not advice.

We can look to the Canadian asset allocation ETFs for a lesson on risk and asset allocation. In that post that tracks the performance of the asset allocation ETF providers, you’ll find this key table.

Source: Dale/ETF providers. Keep in mind there is no guarantee of returns for any period

We can see that when our time horizon is short we create conservative portfolios with lots of bonds and cash. When we have a longer time horizon of 10 years and more, we can be more aggressive perhaps even holding an all-equity portfolio. But once again, risk tolerance permitting.

I recently discussed risk and common mistakes on the BMO ETF Insights YouTube channel.

In the accumulation stage we might pay attention to this chart if you are saving for a home and plan to buy within the next two years. If would be very risk to hold those home down payment funds in an all equity (XEQT-T) portfolio. Your $100,000 could quickly be turned into $50,000 in a severe bear market.

Sequence of returns risk in retirement

Risk gets flipped in retirement. In the accumulation stage if you have 20 years to go before retirement and we enter a severe bear market, “great”. You can now buy your companies/equities at fire-sale prices. Over time that can generate a boost to your wealth creation. You own more of those great companies. Continue Reading…

This summer does not seem to be shaping up to be one that those nearing Retirement can take a long vacation and forget about the markets.

Global macroeconomic headwinds like the ongoing on-again, off-again Iran war continues to impact the price of oil and thus aggravate inflation fears already stoked by high government borrowing levels.

Add to that growing trepidation of a fast-expanding AI Bubble that skeptics warn may burst at any moment, the often-parabolic moves of now-trendy chip and memory stocks and it seems a time to retrench and rebalance. And if that were not enough, Canadian investors need to worry about the ongoing Tariff and global trade wars ignited by the deranged Tariff Man in the White House, and repeated signals that the CUSMA/USCMA negotiations may result in no free trade deal at all.

For this blog — which is being published precisely half way through 2026 — I once again reached out to Linked In and Featured.com, which recently changed its name to Connectively, to get expert opinions from financial advisors, investment executives, business owners and other experts to get their views and suggestions for getting through this summer of investor ennui.

Here’s how the question was posed at Connectively:

How cautious about their investments do you think those in or near Retirement need to be this summer, in light of the ongoing Iran war and impact on inflation; increased nervousness about an AI Bubble and volatile chip and memory stocks, and finally global trade uncertainties in light of the negotiations of CUSMA/USCMA? Suggestions for rebalancing or hedging, role of commodities in preparing for higher inflation.

Out of almost 100 responses, we have picked 19 shown below. As usual, the complete responses are accompanied by the sources’ head shots and bio links to their respective web sites. We have added subheadings to speed readers to the content that seems relevant to particular readers.

Capital preservation deserves equal attention to growth

Investors approaching or living in retirement face a particularly challenging environment this summer. Geopolitical tensions in the Middle East, persistent inflation risks, AI-driven market exuberance, and ongoing trade negotiations have created a backdrop where capital preservation deserves equal attention to growth. Research from the Federal Reserve shows that inflation remains one of the greatest threats to retirement income because rising costs can erode purchasing power over time. At the same time, concentration risk has become more pronounced, with a small group of AI and semiconductor stocks accounting for a significant share of recent market gains.

A prudent approach often involves broad diversification rather than attempting to predict short-term market movements. Exposure across dividend-paying equities, high-quality bonds, inflation-protected securities, and select commodities can help reduce portfolio volatility. Gold and other commodities have historically served as partial hedges during periods of geopolitical uncertainty and inflationary pressure, though excessive concentration in any single asset class may introduce new risks.

Retirement portfolios generally benefit from maintaining adequate liquidity, regularly rebalancing allocations, and ensuring that investment decisions align with income needs rather than market headlines. In uncertain periods, resilience tends to outperform speculation. — Arvind Rongala, CEO, Edstellar

Retirees should focus first on Iran and its Inflation spillover

Retirement timing matters enormously here. I’ve worked with clients who looked fully prepared on paper but had nearly everything exposed to the same macro headwinds you’re describing: trade disruption, energy price shocks, and concentrated tech positions all hitting simultaneously.

The Iran situation and its inflation spillover is where I’d focus first for near-retirees. In April 2025, we watched gold hit nearly US$3,500/oz and money market funds absorb record inflows precisely because investors needed somewhere to park cash when equities wobbled. A deliberate cash buffer covering 12-18 months of withdrawals changes your emotional decision-making completely: you’re not forced to sell equities into a bad market.

On the AI bubble concern specifically, the Nasdaq entered bear market territory earlier this year largely on tech concentration. If you’re holding broad index funds, a target-date fund, and individual chip or memory stocks, you likely have far more AI exposure than you realize. Run a simple overlap check across every holding before assuming you’re diversified.

For commodities as an inflation hedge, I’d think about it sequentially rather than reactively: energy-linked assets and real assets like REITs behave differently depending on whether inflation is demand-driven or supply-shock-driven. With CUSMA/USMCA renegotiation creating genuine input-cost uncertainty for North American manufacturers, agricultural and metals exposure makes more structural sense right now than chasing whatever commodity headline is hot that week. — Daniel Delaney, Owner, Seek & Find Financial

Cut back on concentrated tech holdings and replace with a proportion of your money in short-duration TIPS and I-Bonds

If you’re approaching retirement age in the next few years, this is a particularly critical summer to be proactive. Here’s what I tell folks at MintWit: The problem is not the potential for picking the wrong stock. The risk lies in having been entirely too heavy in equities such that, come a simultaneous geopolitical shock, an AI-driven stock price correction and an inflation spurt triggered by trade war, all three can come crashing down at once before you even have the chance to catch your breath.

The prudent response here is to run your current allocation through a stress test of chip stocks falling 30% while energy prices surge owing to a crisis in the Middle East, and rising costs due to renegotiation of CUSMA terms for North American goods. The reason why you’re losing sleep over it is because you may well be too heavily exposed to growth equities with too little hedging against inflation.

As far as your reallocations, my recommendation is to cut back sharply on concentrated tech holdings and replace with a proportion of your money in short-duration TIPS and I-Bonds, in order to build up that buffer for the likelihood of sticky inflation. I would also recommend a small investment (say 5-10%) in commodities – especially energy and agriculture-related ETFs – to cover your inflation exposure, rather than speculative trades in commodities. As ever, gold continues to function as a geopolitical hedge, although you want to remain disciplined about it.

In sum, the most important thing for those close to retirement at this juncture is optionality. Make sure you have enough of your assets in low-risk, liquid investments so that when the worst-case scenario strikes the market, you don’t end up selling your stocks at rock bottom. — Scott Brown, Founder, MintWit

Chasing every new trend or algorithm change just doesn’t work

I work in tech, but I’ve learned to be cautious. Chasing every new trend or algorithm change just doesn’t work. The steady approach wins every time. I think retirees should treat their money the same way. Don’t panic over headlines. Make small, gradual adjustments to your investments instead. Keeping some money in commodities can help with inflation, and regular check-ins ensure your savings match your life, not the market noise. — Vlad Ivanov, CEO, Search GAP Method

Be cautious but don’t panic … take a barbell approach

I’d be cautious, but I wouldn’t panic. The S&P 500 is now so concentrated in the Magnificent-7 that those names effectively drive the whole index. Off the March low, the Nasdaq-100 ran up roughly 20%, and at points was going nearly parabolic. With renewed tensions and conflict involving US and Iran, we’re now seeing that move cool off with both profit taking and sector rotation into more defensive areas.

On the surface that looks scary. But if you step back to the technicals, we still haven’t broken the 50-day moving average or the 10-week moving average, so there’s real support underneath this market for now.

Volatility like this is genuinely uncomfortable, though, so for someone in or near retirement I’d lean into a barbell approach. Keep some of your high-growth exposure, but balance it with quality dividend payers that cushion the ride and pay you while you wait.

Off the top of my head, two names that fit the stable, income side of that barbell are THG, The Hanover Insurance Group, and PSTL, Postal Realty Trust, a REIT that leases almost exclusively to the US Postal Service, so its rent is effectively government-backed. Neither is a rocket ship. They grow slowly, pay a dividend, and hold up better when the high-flyers wobble. That dividend income is also what helps offset paper losses in a drawdown, so you’re not forced to sell your growth positions at the worst possible time.

These are just examples of the type, not recommendations, but the principle holds is that in a summer like this, you want both ends of the barbell. — Adrian Rosebrock PhD, Chief Investment Officer & Founder, WheelMetrics

Early signs of Stagflation in major economies worldwide

The ongoing Iran conflict is beyond energy deficiency. You could see early signs of stagflation in the major economies worldwide. The volatility is pressuring retirees and the ones approaching retirement with underwhelming returns. According to the latest research by Goldmann Sachs, the uncertainity imposes lower returns on equities and bonds for a brief 1.5-2 years approximately.

With the AI bubble, the tech-heavy portfolio takes the backseat by default. CUSMA renegotiations including currency fluctuations and supply chain instability, navigating pitfalls collectively. All the factors compound to an inflation scenario. Rebalancing is safeguarding the assets and materials, ensuring protection of the equity before inflation wears down.

The average retirement portfolio is leaning more towards innovation but with less focus on the practical inflation scenarios. Last minute-hassle is not going to help in navigating the situation this summer. Portfolio review has become more vital with ongoing fluctuations. — Ankit Sarawagi, Curator, CFO Matrix

Trim the Sails, don’t abandon the Boat

If you’re close to retirement or already in it, the headlines this summer can feel pretty scary. Conflicts overseas, shaky tech stocks, trade deals up in the air, it’s a lot. But here’s what I’d tell anyone in that season of life: don’t let the noise push you into a panic move.

The real risk for retirees isn’t market swings. It’s making emotional decisions that lock in losses or leave you without income when you need it most. If your money is set up right with a solid base of guaranteed income and some protection built in, short-term chaos shouldn’t shake your foundation.

That said, this is a good time to take a closer look at your mix. With inflation still a concern, partly because of oil and energy tied to what’s happening overseas, it makes sense to have some exposure to real assets like commodities. Gold, energy, and other hard assets have historically held up better when prices rise. They’re not glamorous, but they do a job.

If you’re heavy in tech or growth stocks right now, some rebalancing could reduce your risk without pulling you out of the market entirely. Think of it like trimming the sails, not abandoning the boat. The goal at this stage isn’t to chase gains. It’s to protect what you’ve built and make sure it lasts as long as you do. That’s what smart financial planning for this chapter of life is really about. –– Paul Mauro, Founder & Author, Smart Financial Lifestyle

The biggest risk is being overly concentrated in assets that have performed well recently

For investors who are in or approaching retirement, I believe caution is warranted, but not panic. The biggest risk is often not a war, an AI bubble, or trade negotiations themselves, but being overly concentrated in assets that have performed well recently. Retirees generally have less time to recover from significant market declines, so preserving capital becomes increasingly important. If a portfolio has become heavily weighted toward high-growth technology or AI-related stocks, this may be a sensible time to rebalance and lock in some gains rather than relying on a single investment theme to drive future returns.

I would focus on diversification across asset classes, including quality dividend-paying stocks, investment-grade bonds, and a reasonable cash reserve. Commodities can also play a useful role as an inflation hedge, particularly energy and precious metals, but I view them as a supporting allocation rather than a core holding. The goal is not to predict whether inflation will rise or whether technology stocks will correct, but to ensure the portfolio remains resilient under multiple scenarios.

The most successful retirees I have seen are not those who accurately forecast every market event. They are the ones who build portfolios that can withstand uncertainty. In today’s environment, disciplined rebalancing and risk management are likely more important than trying to predict the next geopolitical or economic headline. — Bowen He, Director, Webzilla Digital Marketing Continue Reading…

Nearing financial independence? Growth stocks alone may leave gaps. Find out how a broader, more diverse portfolio can support income and stability.

Adobe Stock: Kiattisak

By Dan Coconate

Special to Financial Independence Hub

As you move closer to financial independence, understanding why your portfolio needs more than just growth stocks can help you make clearer decisions.

Growth stocks often attract attention during strong markets because investors expect future earnings to increase over time.

While that potential can be valuable, these investments can also experience drastic declines when market conditions change. A portfolio that includes different sources of return may provide a steadier experience and help support your goals through a wider range of economic environments.

Growth Stocks do not always Lead

Growth stocks often perform well when investors are optimistic about the future and willing to pay more for expected earnings. The challenge is that market leadership shifts over time, and periods of strong growth-stock performance are often followed by stretches when other investments take the lead.

As you approach Financial Independence, relying too heavily on one investment style can increase your exposure to timing risk. If market conditions turn negative just as you begin making withdrawals, you may be forced to sell investments at lower prices than expected.

Income adds more Breathing Room

Many Canadians pursuing Financial Independence want their investments to do more than simply grow in value. They also want their portfolio to support everyday spending needs without requiring constant asset sales. Investments that generate income can play an important role in creating that flexibility.

Rather than depending entirely on future appreciation, a diversified portfolio can offer a combination of growth potential and ongoing cash flow. This approach may help you feel more comfortable during market downturns.

Inflation Changes the Picture

Inflation directly affects your lifestyle by gradually increasing the cost of living. Even modest inflation can reduce purchasing power over a long Financial Independence journey. For that reason, some investors explore additional ways to diversify their portfolios.

Discussions around real assets and investing in commodities often arise because these investments may respond differently to inflationary pressures. The goal is not to own everything, but to understand whether your portfolio has enough variety to handle changing economic conditions.

Risk feels Different near Financial Independence

Risk takes on a different meaning once you are no longer relying on employment income to support your financial goals. During your working years, market declines may feel temporary because new contributions continue to flow into your accounts.

Near Financial Independence, however, a significant downturn can have a larger impact because withdrawals may begin at the same time. A broader mix of investments can help reduce the influence of any single market trend and provide a more resilient foundation for the years ahead.

A Wider Mix builds more Confidence

You do not need a complicated investment strategy to make meaningful progress toward Financial Independence. In many cases, a simple and diversified portfolio can provide a stronger foundation than one built entirely around growth stocks. Understanding why your portfolio needs more than growth stocks encourages you to think beyond returns alone. A wider mix of assets can help stabilize your finances and make it easier to stay committed to your plan.

Dan Coconate is a local Chicagoland freelance writer who has been in the industry since graduating from college in 2019. He currently lives in the Chicagoland area where he is pursuing his multiple interests in journalism.

By Dale Roberts, Retirement Club/Cutthecrapinvesting

Special to Financial Independence Hub

Bonds may be the adult in the room, but they are certainly afraid of inflation. Bonds usually do their thing: they go up when stock markets get hit hard. They provide ballast. During periods of expected high inflation, or during rising inflation bond prices go down. That can create and contribute negative returns. The bonds can contribute to a portfolio decline.

But not all bonds are the same. Ultra-short bonds carry no price risk, while long-term bonds can carry extreme price risk. It’s crucial that investors understand the ‘types of bonds.’ To intermediate- and long-term bonds, inflation is Kryptonite. How do we battle that force?

Too funny, a rare case when Cut The Crap Investing actually ranked high on search.

Inflation up. Bonds down.

Bond yields rise during inflation primarily because investors demand higher returns to compensate for the reduced purchasing power of future fixed interest payments. Furthermore, inflation often prompts central banks to raise interest rates, which directly drives up yields, while existing bond prices fall to align with new, higher-yielding securities.

As interest rates rise due to inflation, new bonds are issued with higher coupon rates to attract investors. Existing bonds, which pay lower interest rates, become less attractive and must drop in price to remain competitive, which simultaneously increases their yield.

We’ve had some recent experience with the inflation scare of 2021 and into 2022. The bond market (XBB-T) experienced one of its worst performances in 2022, losing around 11% or more as inflation surged, reversing a four-decade bull market in fixed income.

In the above chart we see that bonds provided no ballast. Quite the opposite. That said, we have to keep in mind that bonds have done their thing in every major recession. They stink the joint out, one time, and investors turn on them.

Traditional global stock and bond portfolios have delivered wonderful returns …

Asset Allocation ETF Page – to the end of December 2025

If you have dedicated inflation fighters in the portfolio you’re not too worried about bonds delivering negative returns. We know that stocks don’t always go up. It’s the same for bonds.

In the following chart, we’ll start in 2021. Markets think ahead, of course, and enough investors loaded up on inflation-fighting assets as inflation storms gathered in 2021. The Purpose Real Asset ETF (PRA-T) is a nice one-stop inflation-fighting shop.

PRA-T was up 23.5% in 2021 and 15.9% in 2022.

Add 20% PRA-T to 80% XBAL-T and we have annual returns over 10% with no negative years from 2021 through 2023.

Continue on into 2026 and it gets even better. PRA-T is up almost 16% in 2026.

Go short and clip the inflation price risk

Ultra-short-term government bonds (CBIL-T) do not carry price risk: they are cash-like. In fact, they will provide greater and greater income as inflation expectations and yields rise. Continue Reading…

Last thing I remember

Last thing I remember