No doubt about it: at some point we’re neither semi-retired, findependent or fully retired. We’re out there in a retirement community or retirement home, and maybe for a few years near the end of this incarnation, some time to reflect on it all in a nursing home. Our Longevity & Aging category features our own unique blog posts, as well as blog feeds from Mark Venning’s ChangeRangers.com and other experts.

“Can you believe it, honey? Friday’s my last day at work! Time sure flies. I can’t wait to start spending all of our free time together!”

Did this thought warm your heart, or get your pulse racing in panic? That probably depends on whether you’ve given some good thought to what you’re doing after retirement.

But what do you actually want to do after you stop working? Your retirement income goals will depend much on your answer to that question, as your financial adviser is apt to tell you.

We’re living longer — and that’s a good thing, if you plan for it

‘Retirement’ wasn’t really a thing, until recently. You lived, you worked, you died … and the world kept turning as youth picked up the baton of life’s track meet. That’s partly the reason pension age was set at 65: few were expected to live long enough to claim it! When the USA passed their Social Security Act in 1935, American men were expected to live to about 58.

But with our longer life spans, you could still be shuffling around decades after you’ve stopped working. According to Statistics Canada and the 2016 Census, “there were 5.9 million seniors in Canada, which accounted for 16.9% of the total population. In comparison, there were 2.4 million seniors in 1981, or 10% of the population.”

There are more retirees than ever! So, our question is a practical one: how do you retire and still fill 40 hours a week?

What Canadian retirees are already doing with their time

Does this all seem inspiring … or overwhelming? Is the room spinning at the prospect of playing shuffleboard and doing yard work for the next two or three decades? Fortunately, we’ve picked up an important idea from doing retirement income planning with countless clients. Continue Reading…

Have you ever thought about seasonal work in retirement? My friend, Kirk, recently leveraged seasonal work to experience something for the first time in his life. He became a cowboy, through a seasonal job at a Dude Ranch.

At Age 58!

You may remember Kirk, he’s visited with us before (including his thru-hike on the Appalachian Trail, his broken foot on the Pacific Crest Trail and the story of breaking his ribs when he Lived Life At The Limits on a mountain bike ride with yours truly). This Fall, he’s heading to Nepal to do some trekking around Mt. Everest. Interesting guy, my friend Kirk, and we can all learn something from the way he lives his life in retirement.

Today, he tells us the story of doing seasonal work in retirement at a Dude Ranch, which he did in the Spring of 2018.

The old military and corporate guy became a cowboy. Well, that may be a bit of an exaggeration, but he did “wrangle horses” for 6 weeks at a Dude Ranch. How cool is that?

Here’s his story…

Working On A Dude Ranch

Kirk. A “FIRE Guy In His Prime”

I promised myself I would write three “potential” blog posts for my friend this year covering what could possibly be my most adventurous year since my retirement began 2 ½ years ago. Caution: I am not the spectacular writer that Fritz is; however, here is my latest adventure …

(Note from Fritz: I don’t know about my writing skills, but I do know that Kirk lives life more “on the edge” than anyone I personally know. Nepal, really? That Kirk guy is nuts!)

When I retired roughly 2 ½ years ago I decided to do away with my “LinkedIn” account. I was cleaning up some old things from my work years and didn’t think I would need a resume in my retirement life. As I started checking off things in my Dump Truck List (Buckets are no longer big enough) I started realizing that I had some skill gaps. Ultimately, I wanted to be a wrangler for a cattle drive in Montana but realized that wasn’t going to happen if I didn’t have some experience handling a horse.

I researched some possible jobs through www.coolworks.com and drafted a list of the qualifications for some of the wrangling jobs which interested me. Much to my surprise, I met them all with one exception:

I had no experience in riding a horse.

Having grown up on a farm really prepared me well for many aspects of the job, but we never had horses. How could I learn to ride a horse, handle the tack, teach the ranch’s customers, etc. if I didn’t know how to handle horses myself? While I suppose I could have paid for the experience — I am FI [Financially Independent], after all — there was something in me that kept gnawing in the deep recesses of my mind.

Thoughts which whispered, and thoughts that led to my decision to pursue seasonal work in retirement:

You have been so frugal all your life to get to FI, is this really how you want to spend your money?

Would you really be able to buy this experience or is this something you have to spend time acquiring skill, talent, and familiarity?

What other experiences do you need now in order to pursue the future adventures of your dreams?

(Note from Fritz: I like how Kirk thinks several moves ahead. Dream for your tomorrow, and identify what you should be doing Today in order to achieve your dreams. Move your life from Good To Great).

After much thought, I decided to venture out to an unknown area for me and listen to the younger crowd who said many of their wonderful experiences were as “Workaway” people. Workaway is simply a web service that connects people who are looking for experience with people that are looking for help. The Workaway people generally work 4 – 5 hours per day, 5 days per week in exchange for room/board and experience. Given that I have plans to travel through Asia in the coming years, this approach could help with some international options as well. I looked into the site http://www.workaway.info and decided to give it a try.

It was somewhat difficult to determine where I would go to gain this experience. I wasn’t sure how it would all work out, so I decided to minimize my risk by choosing a location that:

had good/great reviews by those who participated

was close so if it was horrible I could bail

had more than just myself as a workaway so I could learn from the experience of others

I ended up selecting a Bed and Breakfast Dude Ranch in upstate NY, only an hour away from where I grew up and where my mother still lives. If it was a horrible experience I had a solid Plan B. I would simply bail out and stay with my mom, working around her house to complete some things on her “To Do” list. It would also afford me the opportunity to spend time with some aunts, uncles, and cousins which I had not seen in far too long. Continue Reading…

Did you know a looming Bear Market Crisis is approaching?!

I just read it on the internet, so it’s got to be true!

To make matters worse, I just retired a month ago.

Uh Oh! (Am I screwed?)

Today, some reality about Bear Markets, along with 6 steps to consider as you structure your retirement portfolio.

A Looming Bear Market

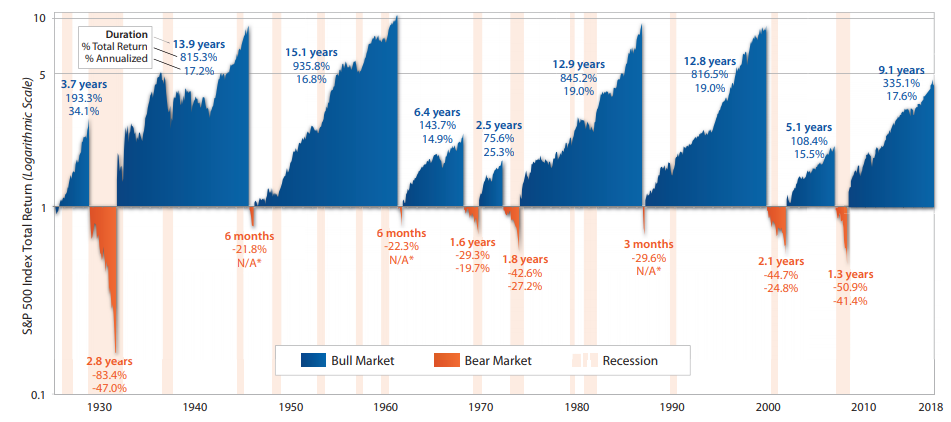

Ok, I’m having a bit of fun with the “read it on the internet” line, but the reality is that a Bear Market WILL happen. I’m not being prophetic, just stating the facts. Since before the days of the tulip mania in 1637, bear markets have always been will us, and they always will. We’ve benefited from a very nice bull run. We’re being naive if we think that it will never end.

Since 1900, we’ve had 32 Bear Markets, defined as a correction of 20% or more. Do the math, and that averages out to a Bear Market every 3.7 years. The average bear market lasts 367 days (the longest was 34 months!). Here’s what they look like graphically:

The Looming Bear Market Will Drive A Retirement Crisis

“A recession could decimate even substantial retirement portfolios.”

Further, the author goes on to say that Social Security and Medicare, and the resulting increase in taxes, increase in eligibility age and reduction in benefits “would be a disaster” for those dependent on the safety net.

Add to that the Voices Of Worry over the global debt pile up and the underfunded status of many state & local pension funds and things could get really, really ugly.

Maybe I shouldn’t have retired early.

Too late now, I guess I’d better get to work on building a Bear Market Crisis Prevention Plan.

The Looming Bear Market Crisis

We all know a Bear Market is coming. It’s been an increasing theme in the blogosphere, with even the esteemed Financial Samurai taking risk off the table. America’s wealthy are moving to cash. Ben Carlson of A Wealth of Common Sense has 36 Obvious Investment Truths to remind folks that you should protect yourself.

I’m not a panic-driven investor, screaming a scare tactic headline to drive traffic (tho, if you’re reading this, I guess it worked, right?). Rather, I’m reminding folks of the reality of how the markets work and encourage you to think about it as you develop your retirement portfolio strategy. Yes, stocks have historically outperformed over the long-term, and will likely continue to do the same. Just recognize that the road can be bumpy, and plan accordingly to avoid getting bitten by a bear when you can least afford it.

A Bear Market Crisis Contingency Plan

The reality is that bear markets have always been with us, and always will. Unfortunately, we never know when that snake is going to strike, so it’s best to wear snakeproof boots along the path of retirement. Following are some steps I’m taking, as an early retiree, to defend our portfolio against the risk of a bear attack. View them as suggestions, and pick and choose as appropriate for your situation.

You want to retire soon. How should you set up your retirement income?

You talk with some friends, read about it on the internet, and talk with a financial advisor. Are you actually getting good advice?

When it comes to retirement income, most financial advisors rely on a few rules of thumb handed down from one generation of advisors to the next. The rules appear to be common sense and are usually accepted without question.

Before giving clients this advice, I tested them with 150 years’ history of stocks, bonds and inflation. I wanted to see if these rules were reliable for a typical 30-year retirement. (The average retirement age is 62. In 50% of couples that reach their 60s, one of them makes it to age 92.)

These five rules are the “conventional wisdom” – the advice typically given to seniors:

“4% Rule”: You can safely withdraw 4% of your investments and increase it by inflation for the rest of your life. For example, $40,000 per year from a $1 million portfolio.

“Age Rule”: Your age is the percentage of bonds you should have. For example, at age 70, you should have 70% in bonds and 30% in stocks.

“Sequence of returns”: Invest conservatively because you can’t afford to take a loss. You can run out of money because of the “sequence of returns.” You can’t recover from investment losses early in your retirement.

Don’t touch your principal. Try to live off the interest.

Cash buffer: Keep cash equal to 2 years’ income to draw on when your investments are down.

The results: NONE of these rules of thumb are reliable, based on history.

Let’s look at each to understand this.

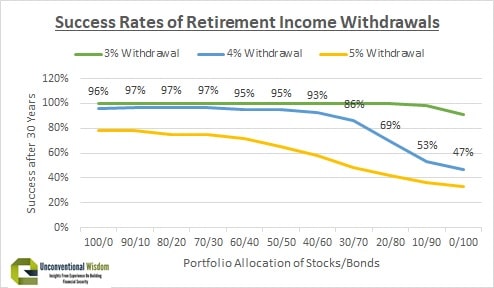

1.) “4% Rule”: Can you safely withdraw 4% of your investments plus inflation for the rest of your life?

Based on history, the “4% Rule” was safe for equity-focused investors, but not for most seniors.

In the results shown in the graphic at the top of this blog, the blue line is the “4% Rule,” showing how often in the last 150 years a 4% withdrawal plus inflation provided a reliable income for 30 years.

The “4% Rule” only works with at least 50% in stocks.

The “4% Rule” worked only if you invest with a minimum of 50% in stocks. Even safer is 70-100% in stocks. It is best to avoid a success rate below 95% or 97%. They mean a 1 in 20 or 1 in 30 chance of running out of money during your retirement.

Most seniors invest more conservatively than this and the 4% Rule failed miserably for them.

A “3% Rule” has been reliable in history, but means you only get $30,000 per year plus inflation from a $1 million portfolio, instead of $40,000 per year.

These results are counter-intuitive. The more you invest in stocks, the safer your retirement income would have been in history.

To understand this, it is important to understand that stocks are risky short-term, but reliable long-term. Bonds are reliable short-term, but risky long-term. Why? Bonds get killed by inflation or rising interest rates. If either happens during your retirement, you can easily run out of money with bonds.

The chart below illustrates this clearly. It shows the standard deviation (measure of risk) of stocks, bonds and cash over various time periods in the last 200 years. Note that stocks are much riskier short-term, but actually lower risk for periods of time longer than 20 years.

Stocks are more reliable after inflation than bonds after 20 years.

Ed’s advice: Replace the “4% Rule” with “2.5% +.2% for every 10% in stocks Rule.” For example, with 10% in stocks, use a “2.7% Rule.” If you invest 70% or more in stocks, then the “4% Rule is safe.

2.) “Age Rule”: Your age is the percentage of bonds you should have. For example, at age 70, you should have 70% in bonds and 30% in stocks.

There may be as many as 26 distinct sources of income a retired couple may encounter, estimates Ian Moyer, a 40-year veteran of the financial industry and creator of the Cascades program described in the article.

When he started to plan for his own decumulation adventure, five years ago, he felt there was very little planning software out there that was both comprehensive and easy to use. So, he hired a computer programmer and created his own package, now called Cascades.

While the main focus of the FP article is on Cascades, (available to financial advisors for $1,000 a year; do it yourself investors can negotiate a price directly), the article also references a couple of other programs we have looked at previously here on the Hub: Doug Dahmer’s Retirement Navigator and BetterMoneyChoices.com, the latter currently nearing the end of beta testing.

Dahmer has been writing guest blogs on decumulation here at the Hub almost since this site’s founding in 2014. See for example his most recent one, or the similar articles flagged at the bottom: Top 10 Rules for Successful Retirement Income Planning.

Dahmer says he’s pleased that others are waking up to the need for tax planning in the drawdown years: “Cascades provides a very good, easy-to-use introduction to these concepts.”

Planning for peaks and valleys in spending

Retirement Navigator’s Doug Dahmer

However, Dahmer would like an approach that doesn’t assume yearly spending remains relatively static: his Better Money Choices(available on line for $108 a year) allows for the “peaks and valleys” of spending as retirees pass through their Go-go to their slow-go and finally their “no-go” years. Most retirees have to plan for sporadic large purchases like renovations or replacement of roofs or furnaces, plus of course vacations with widely varying price tags. Each spending peak represents a tax challenge, while the valleys are where the tax planning opportunities exist. Dahmer likens Better Money Choices to a gym monthly membership and Retirement Navigator to a personal trainer.

Personally, I found going through both firm’s programs a fascinating exercise, very much like putting together a jig saw puzzle. For me, Better Money Choices helps you visualize the final picture you’re trying to assemble, showing how much money you’ll need and when you’ll need it. Cascades provides vivid yearly snapshots of your year-by-year progress in putting the pieces together.

By Tea Nicola

By Tea Nicola