No doubt about it: at some point we’re neither semi-retired, findependent or fully retired. We’re out there in a retirement community or retirement home, and maybe for a few years near the end of this incarnation, some time to reflect on it all in a nursing home. Our Longevity & Aging category features our own unique blog posts, as well as blog feeds from Mark Venning’s ChangeRangers.com and other experts.

One of the chief concerns regarding senior citizens, especially those who live alone or in assisted living facilities, is boredom. Experts in senior care know that when a person is bored or feels unstimulated this can escalate to depression, which is already another concern among the senior population.

While the lack of activity could be due to a physical ailment that prevents the person from doing things they loved to do — such as walking, running, or other highly physical activities — in many cases it’s simply that a little nudge and some positive guidance is needed. A caregiver can be instrumental in this role and encourage their client to be more active, mentally or physically.

If you work with or know a senior citizen who needs to be challenged, adding a hobby to their daily routine can make a world of difference in their mood and ultimately their overall health. These are just a few hobbies that are fun, challenging, and can help lift mood and energy levels.

Art

Art is one of the easiest hobbies to introduce because it comes in so many forms. From painting with watercolors to adult coloring books, art brings a sense of freedom and independence as there is no right or wrong way to do it; art is subjective.

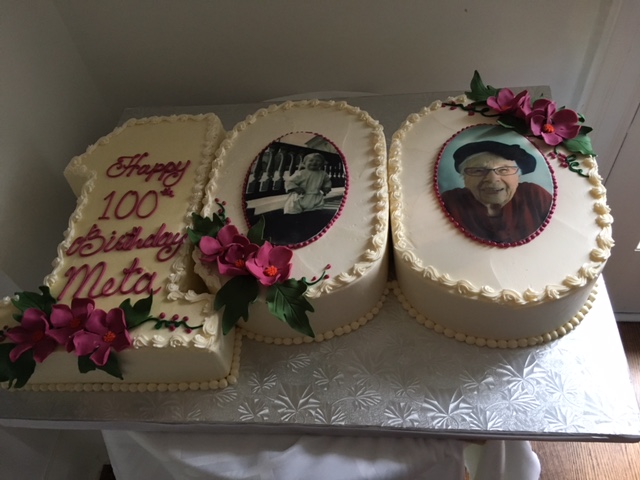

The piece is based on a recent Seniors’ Luncheon hosted by the Toronto church I attend and as you will read, I was struck by how the experiences of these seniors — who ranged in age from 82 to 100 — reinforced the theme of my recently released co-authored book, Victory Lap Retirement.

In short, every senior at the table believed in continuing to work in some fashion even in their looming old age. Including 100-year-old Meta, pictured. While I changed the names of the other seniors in the article, Meta is a real name and used there and here with her permission.

Here’s the thing. Until she suffered a hip injury earlier this year, Meta was still working one or two half-days a week at a nearby printing firm. And at her 100th birthday celebration earlier this month, this continued work connection meant several of the people celebrating with her were from work, as well as the church, neighbours and various other circles.

And now that the din over her 100th birthday milestone has subsided, Meta told me last week that she wanted to return to work one day a week, because she misses her co-workers and she likes to get out of the house (she lives in the top floor of a house overlooking Lake Ontario, and has been there since the 1960s. The last thing she would want would be to move to an institution catering to seniors.)

The danger of retiring “too soon”

As for the senior men I chatted with that day, one regretted having voluntarily retired “too soon” at the tender age of 58: Kevin (not his real name) said he did so because he had a good teacher’s pension but when his wife passed away soon after, found himself with too much time on his hands.

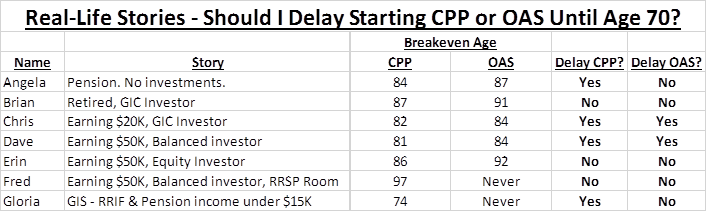

Here you will see that the single most important factor in deciding whether to delay CPP after age 65 is: Will you withdraw more from your investments if you delay starting?

A quick review of the facts:

Delayed CPP Rules

The maximum CPP benefit in 2016 at age 65 is $1,092.50 per month, or $13,110 per year.

You can delay starting up to age 70 and you get 8.4% more for every year after age 65. If you start at age 70, you get 42% more for life, so the maximum is $18,616 per year.

New rules in 2012 allow you to start CPP even if you are still working.

If you are over 65 and still working, you can choose whether or not to pay into CPP.

Your 8 lowest earning years since age 18 (plus years when you had kids under age 7) are “dropped out” in calculating how much CPP you get.

Delayed OAS Rules

The maximum OAS benefit in 2016 at age 65 is $578.53 per month, or $6,942 per year.

You can delay starting up to age 70 and you get 7.2% more for every year after age 65. If you start at age 70, you get 36% more for life, so the maximum is $9,442 per year.

“We’re on a bit of a crusade to change the way our society thinks about retirement.” — Jonathan Chevreau & Mike Drak

Mike Drak and Jonathan Chevreau, co-authors ofVictory Lap Retirement(published, October 2016) are not the first to head out on this crusade. Apart from the material on the larger subject of aging and longevity, in my library I must have at least 19 books, in addition to the stacks of reports, studies and new models on the subject of Retirement.

Over the twenty years in the career services industry, where I worked directly with business executives in their later life transitions – leaving the corporate crow’s nest, as I call it, I can appreciate where Mike and Jonathan are coming from in their take on this. I have produced three retirement programs since 2001, and in the process suffered from metaphor madness, developing novel ways of reframing the concept of retirement and our later life journey.

However, this Drak & Chevreau volume is a welcomed new addition to this crusade. The book, by way of its novelty, weaves the conversation from the threads of a concept called Findependence, as the cornerstone of aVictory Lap Retirement. So here we go. Rather than a traditional book review, here in this blog post, I present views of the authors as shared through interview questions with them in late October.

Authors Interview

Mark’s Q: Your co-authored book, early on, takes a shot across the bow at the “financial media & financial services industries” in the way they persist to push “Retirement” as if it were some final destination. (There seems little shift between the 1970’s London Life’s Freedom 55, to Prudential’s 2016 Race for Retirement campaigns for example.) What one new key message should marketers take from reading Victory Lap that could become a differentiator in their marketing?

Mike: The industry is using the same commercials that they used 40 years ago. The only difference is that they are now in color. The world of retirement has changed significantly over the years and most people cannot afford nor do they want to live the lifestyle portrayed in their commercials.

Banks assume more money equals better retirement, which is wrong thinking. Banks are good with the investment piece but they need to become more involved with the lifestyle piece. How can you ever know if you have enough if you do not have a firm handle on what type of retirement lifestyle you want in retirement and what that lifestyle will cost?

Mark’s Q: At one point in Chapter 3, you make the point that: “Compounding the problem is the lack of financial education our children receive in school.” You also say in Chapter 4 that the importance of financial independence is a prerequisite to the new stage of life you call “Victory Lap Retirement.” Let’s play here. What do you think about an opportunity for you to design/deliver a “Findependence” course relatable to high school teenagers that didn’t use the word Retirement? What then would the main message sound like to them?

Subsequent to that, my latest MoneySense Retired Money blog looks at the topic of estate planning as it related to Tax-free Savings Accounts (TFSAs). To access the full blog, click on the highlighted text here: Why your TFSA needs a Successor Holder.

We had mentioned in an earlier blog that TFSAs were excellent vehicles for estate planning and minimizing tax of families as a whole. See How TFSAs can aid your Victory Lap.

We also said that it’s by far preferable for couples to name each other Successor Holders on their respective TFSAs. Otherwise, things get pretty complex, which is what the MoneySense blog goes into in some depth.

TFSA succession planning often not well understood

Sandy Cardy

The blog is based largely on input from Mackenzie Investments and a brochure it published entitled What happens to your TFSA at the time of death?, which you can access in full by clicking on the link. It also quotes regular Hub contributor Sandy Cardy, who was the head of tax and estate planning at Mackenzie when that brochure was published. In that role, she was responsible for educating the financial advisors who sell mutual funds on estate planning, including its role in TFSAs. As she notes in the MoneySense blog, this topic of TFSAs at death is not well understood even by some financial professionals.

By Cher Zevala

By Cher Zevala