By Fritz Gilbert, TheRetirementManifesto

Special to Financial Independence Hub

I’m fortunate to have saved aggressively in my company’s 401(k) since I started my career at Age 22.

It’s what allowed me to retire at Age 55.

And yet, like many folks my age, those savings were predominantly in “Before-Tax” accounts in my company’s 401(k) plan. Sure, I got the tax break while working, and I felt like a genius. Besides, we didn’t have the option of investing in a Roth, so the decision was easy.

I knew those taxes would come due when I “got old,” but I’d worry about that later.

Later has arrived.

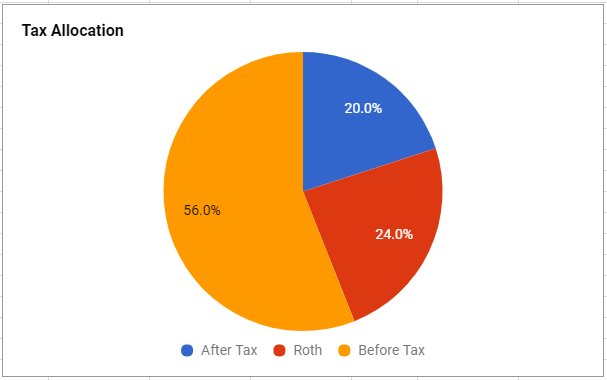

As I shared in my Retirement Drawdown Strategy, when I retired, we had 56% of our retirement savings in Before-Tax accounts, as shown below:

The Golden Age of Roth Conversions

Now that I’m retired, I’ve been laser-focused on doing annual Roth conversions to reduce that Before-Tax balance. As I wrote in The Golden Age of Roth Conversions, it makes sense to do Roth conversions in your early retirement years (be careful if you’re getting ACA subsidies, and ugly Aunt IRMAA can be a problem if you’re 63 or older). I won’t rehash the arguments for why; you can read about it in the linked article.

My goal is to manage the taxes on my terms, rather than being “forced” into whatever the Required Minimum Distributions rule requires in my 70s. I’d also like to get as much of that money converted into a Roth for the benefit of my wife, in the event I die early (she’d pay higher taxes as a single tax filer vs. our current “Married Filing Jointly” status). For now, I’m playing the tax bracket “stuffing” game (topping off my selected tax bracket with Roth conversions) and trying to be smart about minimizing the taxes I pay throughout my retirement.

The Bad News: The Roth conversions are not making as much of a difference as I had hoped.

My Biggest Surprise in Retirement: It’s Hard to reduce your Pre-Tax Account Balance!

We’ve all heard about the power of compounding and how valuable it is in personal finance. If you want a refresher, check out my post, “The Most Powerful Force in the Universe.”

What I didn’t think about, and only realized after I retired and started doing Roth conversions, is the fact that compounding makes it difficult to reduce your pre-tax account balance.

Despite doing aggressive Roth conversions, our pre-tax balance isn’t coming down like I expected!

In fairness, part of that “problem” is driven by above-average returns since my retirement in 2018. First world problem, I know. But it’s still been a big surprise.

Let’s do a hypothetical example to demonstrate the point.

To make the math easy, let’s say you have $1M in your pre-tax account, and your first full year of retirement is 2019. If you had that entire $1M in stocks, here’s what would have happened without doing any Roth conversions (S&P 500 returns from ycharts, including dividends):

In this example, a $1M portfolio would have grown to $2.6M in 6 short years. That’s the power of compounding. Amazing!

Let’s modify the above example, and say you’re doing an annual Roth conversion of $50k.

How much impact would Roth conversions make? Not much…

Despite doing annual Roth conversions of $50k, the pre-tax value has still doubled, to $2.15 M!

A More Realistic Scenario – $500k

Ok, I hear you. No one has $1M in their pre-tax account. I got your attention, though, right?

Fair enough, let’s assume the starting balance is $500k (which compares nicely with the average 401(k) balance of $573k for folks in their 60’s):

The problem remains.

With a $500k starting balance and $50k annual Roth conversions, the account has still grown by $357k (to $857k), or 71%.

Bottom Line: It’s difficult to reduce your pre-tax account balance due to the power of compound interest.

In fact, the only way to reduce your pre-tax account is to do annual Roth conversions in excess of the annual return generated by the pre-tax portion of your portfolio. Sticking with the $500k example, an average annual Roth conversion of $89k would have been required to maintain the pre-tax balance at $500k, as shown below:

(Note: you could argue about my $0 Roth conversion in a down year, but it’s just an example. Quit whining and do your own math – wink.)

What About A 60/40 Portfolio @ $500k?

No one has a 100% stock portfolio in their pre-tax accounts, right? Let’s see what things look like if our retiree had a 60/40 stock/bond allocation in their pre-tax accounts. We’ll use the S&P 500 for stocks, and Vanguard’s Total Bond Market Index Fund (VBMFX) for bonds, we can find their annual returns here.

Without any Roth conversions, the account would have grown from $500k to $990k, as shown below:

Add in our $50k/year of Roth conversions, and the ending balance is $609k, an increase of 22%:

Bottom Line: Even with a 40% bond allocation, it’s difficult to reduce your pre-tax balance via Roth conversions.

We’ve done aggressive Roth conversions every year, yet I continue to be frustrated by how little we’ve moved the needle. In full transparency, we’ve reduced it, but only by 15% of its starting value. That’s far less than I would have expected, given the size of the conversions we’ve done. Continue Reading…