Flexibility without stock-picking: Sector ETFs offer diversified access to industries like tech, health care, and energy, without the need to select individual companies.

Diversification and precision: Broad ETFs provide market-wide exposure, while sector ETFs let you overweight specific industries based on your market view.

Tactical or strategic: Use sector ETFs for short-term tactical calls or long-term structural tilts (e.g., overweighting defensive sectors for cash flow).

By Michelle Allen, BMO ETFs

(Sponsor Blog)

There are many strategies investors can use in their portfolios. One of the most popular strategies is making tactical tilts with sector ETFs.

Sector ETFs – like the new BMO SPDR Select Sector Index range – allow investors to focus on the parts of the market they believe will outperform, such as health care, financials, technology, or industrials.

These ETFs make it simple to increase exposure when certain sectors are expected to perform strongly or dial it back to buffer portfolios when economic conditions change, and are available in both unhedged1 and hedged-to-CAD2 versions.

In this article, we explore how sector behaviours shift across different economic environments, and how tactical tilts using sector ETFs can help investors pursue outperformance.

What is tactical investing?

Tactical investing refers to the process of adjusting portfolio allocations in response to market conditions or economic signals.

While a long-term investor might stick to a static asset allocation, tactical investors“tilt” or increase their exposure toward sectors or asset classes that they believe are poised to outperform over shorter time frames.

Sector ETFs are ideal tools for tactical investing. They allow investors to quickly and easily overweight specific sectors without the need to pick individual stocks. At the same time, they can also be used to create more balanced portfolios as they can be used to diversify portfolios that are concentrated in certain industries.

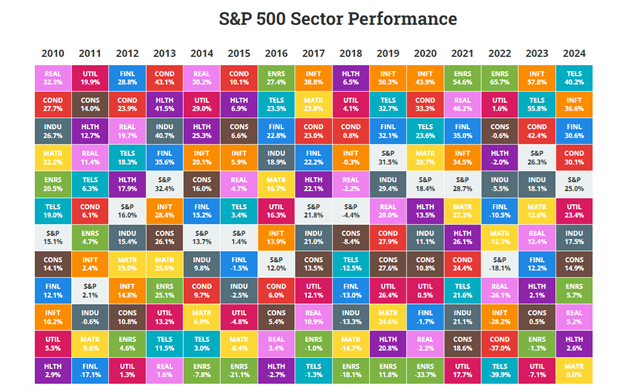

Sector performance can change dramatically each year

Sector performance often mirrors the dynamics seen across different asset classes and individual stocks: the top performers tend to change from year to year as shown in the table below3.

Over the past five years, we’ve seen sectors like information technology, consumer discretionary, and communication services lead the market in 2020 and 2021, only to become some of the worst performers in 2022. That year saw a massive rotation into energy, a sector that had significantly lagged in 2020.

Chart 1 – S&P 500 Sector Performance

Table 1 – S&P 500 Average Sector Returns

Source: Novel Investor (as at March 31, 2025)

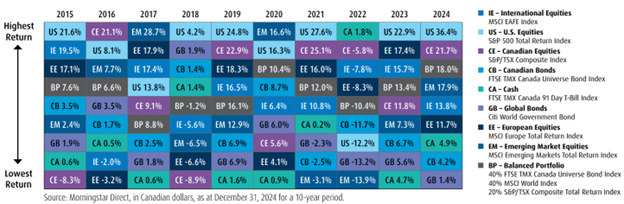

Chart 2 – Asset Class Returns

Index and sector returns do not reflect transactions costs or the deduction of other fees and expenses and it is not possible to invest directly in an Index. Past performance is not indicative of future results.

What drives these rotations? One of the key concepts is the economic cycle, which typically moves through four broad phases:

- Recession: A period of economic contraction marked by falling gross domestic product and weak demand.

- Recovery: Growth begins to rebound as consumer and business confidence, and spending, return.

- Expansion: Economic activity strengthens, employment rises, and output reaches new highs.

- Slowdown: Growth decelerates, signaling a potential shift back toward recession.

S&P 500 sector performance during phases

Understanding how sectors behave during different phases of the economic cycle is key to making informed tactical tilts. Here’s a snapshot of average S&P 500 sector performance across the four main stages of the U.S. business cycle (based on historical data from 1960-2019)4: Continue Reading…