By Dale Roberts, cutthecrapinvesting

Special to Financial Independence Hub

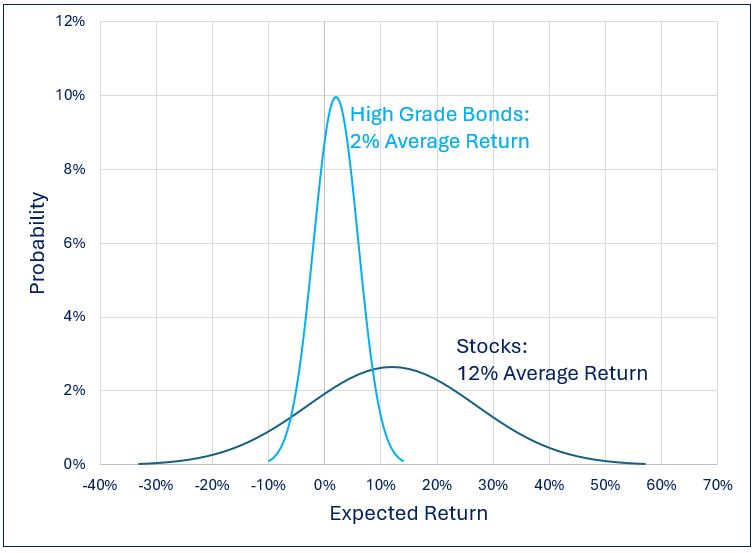

The utility sector is known for its defensive qualities, providing a stable investment option in times of market uncertainty. By overweighting defensive sectors, investors can lower the volatility (risk) of their portfolios. Many will refer to Canadian utilities as ‘bond proxies’ due to their steadiness. However, the true strength lies not in the dividends they offer but in the inherent defensive nature of these companies. Utility stocks are considered defensive because they tend to perform well during economic downturns. Consumers continue to need electricity, water, and other essential services even when the economy is struggling. So here we’ll take a look at Canadian utility stocks and ETFs.

There are a few reasons for an investor to embrace the utilities sector. They may want a portfolio that is less volatile. A retiree can witness a real financial benefit as a portfolio that experiences lesser drawdowns in recessions can create greater and more durable income over time.

Defensive sectors

In this post, the Defensive sectors for Retirement, the three defensive sectors were almost twice as good as a traditional balanced stock and bond portfolio. That is to say, the portfolio moved through the financial crisis of 2008-2009 and left the retiree with a portfolio almost twice as large as the traditional 60/40 balanced portfolio.

Keep in mind past performance does not guarantee future returns. That said, consumer staples, utilities and healthcare have a long history of offering greater portfolio stability.

Canadian utility stocks and ETFs

That above posts looks to U.S. staples, utilities and healthcare stocks. There’s no better place to find multinational consumer staples and healthcare stocks. The healthcare sector is non-existent in Canada. Our consumer staples sector in Canada (XST.TO) is very good, but is mostly domestic. More on that later.

In the Globe & Mail Rob Carrick offered an article (sub required) on Canadian utility ETFs. Rob noted that the fees for these ETFs are quite large compared to market index-based ETFs. The fees are in the 0.32% to 0.61% range. That said, that is the norm for ‘specialty’ or sector ETFs. Rob looked at three Canadian utility ETFs …

The two high-fee funds are the BMO Equal Weight Utilities Index ETF ( ZUT-T), with assets of $500-million and 14 total holdings; and the iShares S&P/TSX Capped Utilities Index ETF ( XUT-T) with assets of $379-million and 15 holdings.

A third fund, the Global X Canadian Utility Services High Dividend Index ETF ( UTIL-T) will on March 4 reduce its current MER of 0.61 per cent to an estimated 0.32 per cent. UTIL has assets of $379-million and 15 holdings.

Core utilities or extended universe?

One key decision that an investor will make is: what types of utilities do you want to own? You can stick to the traditional power/electricity producers, or you can include pipelines and the modern utilities known as the telcos.

ZUT.TO and XUT.TO are traditional power utilities. They are very similar, except the BMO ZUT is equal-weighted while the iShares XUT is cap-weighted (the largest companies get the greater weighting within the index). I’d give the edge to the BMO ETF. Continue Reading…