By Anthony Damtsis

Special to Financial Independence Hub

Expectations of the future shape how we behave today, especially when it comes to planning for retirement. When people overestimate or underestimate where their retirement income will come from, it can affect how they save, how they plan, when they retire, and how financially secure they feel over time.

That sounds simple enough. But retirement has a way of making simple things complicated.

Recent research from CAAT Pension Plan shows a clear gap between what working Canadians expect retirement to look like and what retirees actually experience.

The retirement we picture

Nearly one in four working Canadians expect personal savings to be their primary source of income in retirement. In reality, only about one in seven retirees rely on personal savings as their primary source of income.

At the same time, working Canadians appear to underestimate the role of workplace pensions. Among working people with a pension, only 10% expect it to be their primary source of income in retirement. But among retirees with a pension, 23% say their pension is their primary income source.  Pensions are a foundational source of income for many. Retirees with pensions report approximately $2,750 more in average monthly household income than retirees without pensions.

Pensions are a foundational source of income for many. Retirees with pensions report approximately $2,750 more in average monthly household income than retirees without pensions.

For many Canadians, that is the difference between getting by and living well. Defined Benefit [DB] pensions can provide a predictable stream of retirement income, reduce the burden of managing investments alone, and help protect against the risk of savings running out.

This expectation gap matters because expectations are not harmless. If people expect personal savings to carry more significance than they realistically will, they may delay planning, undersave, or assume they will have more time to catch up later. That can increase the risk of outliving savings, delaying retirement, or becoming more dependent on public supports.

The reality today is that 38% of Canadians without a workplace pension report taking little or no action toward saving for retirement. Among Canadians with household income below $50,000, that figure rises to 60%.

This can show up as delayed retirement. For Canadians, the average ideal retirement age is 60, while the average expected retirement age is 67. For many people, there is a meaningful seven-year gap between the retirement they hope for and the retirement they think is realistic.

There is a quiet lesson in that gap. When people do not have a clear path to retirement, they do not always change their savings behaviour today. Sometimes they change their expectations about tomorrow.

The pension habit

This research challenges the idea that pensions crowd out personal saving. Savings habits are an important building block in creating predictable income in retirement. Pensions can act as a foundation for those habits because they make saving structured, automatic, and easier to sustain.

This matters because good financial behaviour is often less about willpower than design. If saving depends on making the right decision every month, life has plenty of opportunities to get in the way. A pension changes the architecture of the decision. It turns saving from something people have to repeatedly choose into something that happens more reliably in the background.

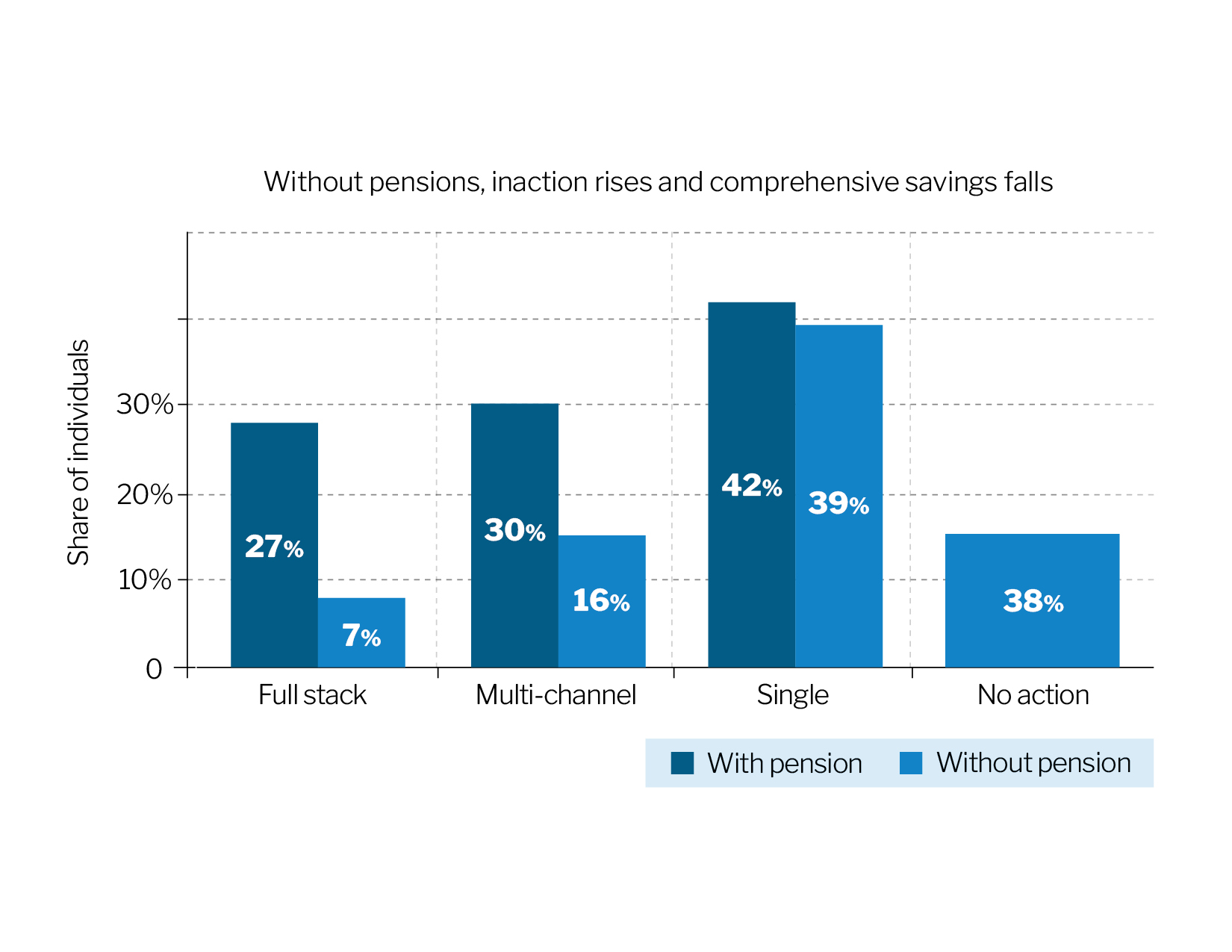

The research suggests this happens in the real world. Pension plan members are nearly four times more likely than non-pension plan participants to report using a full suite of retirement savings tools, such as TFSAs, RRSPs, and non-registered accounts. Specifically, 27% of pension members use a full suite of savings tools, compared with just 7% of those without a pension.

Canadians with workplace pensions are also more likely to use multiple savings approaches at the same time, 30% compared with 16% of those without a pension.

Access is the real barrier

Many Canadians want to save, but they do not always have access to the tools that make saving easier.

According to CAAT, more than half of non-retired Canadians, 58%, say the lack of a workplace pension limits their ability to save. Among retirees, 33% say the same barrier prevented them from saving earlier in life. And among retirees who do not have a pension, 68% wish they had been able to contribute to a pension plan earlier in life.

That matters because retirement planning asks a lot of individuals. People are expected to decide how much to save, where to invest, how much risk to take, when to retire, when to start drawing income, and how to make that income last for an unknown number of years.

Pensions help reduce that complexity. They turn retirement saving into a regular, structured process and, in the case of defined benefit pensions, can turn those savings into more predictable income.

Designing for reality

The bigger lesson from CAAT’s research is that pensions are more important than many people think. They shape retirement income, savings habits, financial confidence, and reveal something important about human behaviour. People do not always need more information. Sometimes they need better systems.

Pensions help provide those systems. They make saving easier, income more predictable, and retirement feel more achievable.

Anthony Damtsis is the director of Behavioural Analytics at CAAT Pension Plan. He leads a team that focuses on using analytics, survey research, and behavioural insight to better understand how the pension plan can serve members.

Anthony Damtsis is the director of Behavioural Analytics at CAAT Pension Plan. He leads a team that focuses on using analytics, survey research, and behavioural insight to better understand how the pension plan can serve members.