By Bradley Krom, WisdomTree Investments

By Bradley Krom, WisdomTree Investments

Special to the Financial Independence Hub

Year-to-date, more than US$32 billion has flowed in to emerging market (EM) exchange-traded funds (ETFs) in the U.S.1 As a consequence, EM equities, bonds and foreign exchange (FX) markets are outperforming most developed markets by a sizable margin. Despite a proliferation of choices over the last several years, WisdomTree continues to advocate a multiasset approach to EM. Below, we contrast the various risks and drivers of return for EM FX, equities and the fixed income market.2

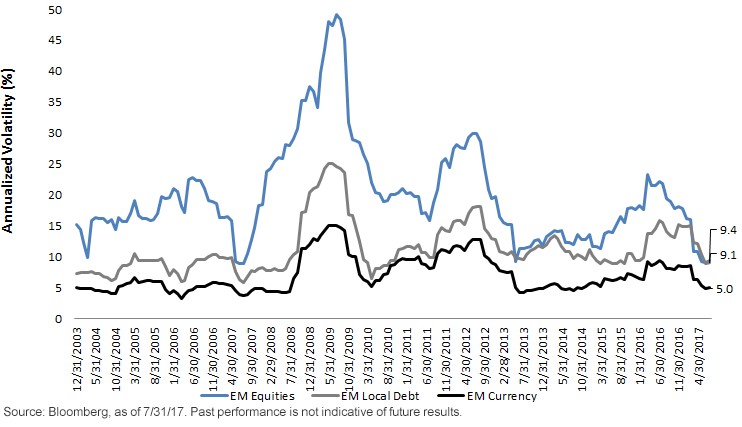

How much risk (Volatility)?

One of the more puzzling issues for global investors is the general lack of volatility across major asset classes. Emerging markets are no exception. As the chart below shows, returns have been strong and volatility has generally been declining, similar to other markets. In the case of EM equities, volatility has fallen to levels not seen since 2007.

Rolling 12-Month Volatility (%)

While we are not in the camp that says low volatility implies that a market correction is imminent, it is notable that EM equity volatility has dipped below EM local debt over the last 12 months. This is attributable to several factors, most notably the underlying currency exposure difference between the equity index and bond index.

Equities: More In Asia with lower FX volatility, Fixed Income more in Latin America with higher FX volatility

Due to underlying macro conditions, currencies in Asia tend to be less volatile than currencies in Latin America. EM equities have over 72% of their exposure in EM Asia compared to the EM local debt,3 which only has a 23% weight.4 Therefore, even though the underlying asset of equities may be higher than bonds, the overall exposures may not always tell the same story.

The last time volatility converged in this way was 2013 during the “taper tantrum.” For the 12 months ending June 30, 2013, returns between EM local debt and EM equities were similar (1.32% versus 2.87%). However, in the next 12 months ending June 30, 2014, EM equities outperformed EM local debt by over 1,000 basis points while maintaining comparable volatility. With volatility particularly difficult to forecast, we would continue to advocate EM equity risk over rate risk in the low-volatility, low-interest rate environment.

Drivers of Return

While investors have generally been rewarded for allocating to EM assets en masse YTD, examining the likely drivers of return going forward can be instructive. From 2011 to mid-2015, EM currencies depreciated by approximately 7% per year.5 In our view, while a rebound will likely not be a straight line, we feel comfortable increasing our exposure to EM FX given current prospects for growth.

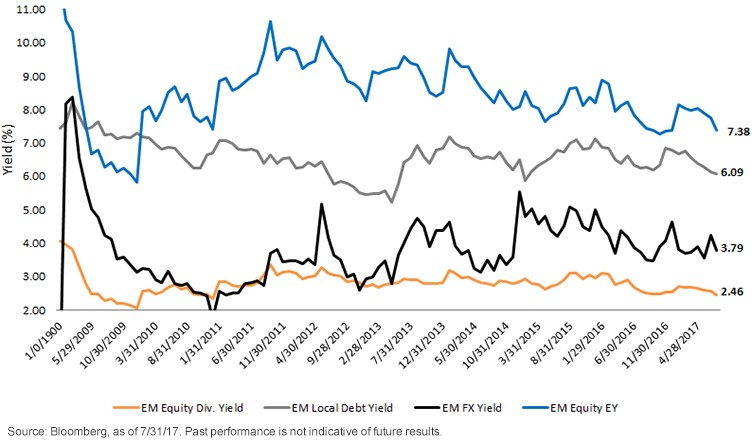

Despite strong returns since early 2016, EM FX remains in the bottom third of its historical range. In addition to spot FX appreciation, investors are able to derive additional carry from EM FX in exchange for taking on risk. While short-term interest rates peaked in late 2014, they still offer a yield of nearly 3.8% versus the U.S. dollar.6

Similarly, EM local debt also provides investors the opportunity to capture yields in excess of 6%. For this asset class, investors should be conscious of three separate drivers of return: FX, the direction of EM interest rates, and income. While the U.S. may continue its path of interest rate hikes into 2018, many EM central banks are in the process of cutting rates to help stimulate growth. In fact, every major country in Latin America is forecast to cut rates at least once in 2017. Some countries, including Brazil, aim to cut rates aggressively as inflation continues to fall.7 Shifting focus to EMEA, both Russia and South Africa are expected to cut rates to help the economy offset weakness due to geopolitical tension. In EM Asia, most central banks are expected to remain on hold through the end of the year. While some investors may worry about EM countries cutting rates in the face of U.S. Fed rate hikes, we believe that the potential for better economic growth should counteract a majority of any FX depreciation pressures.

For EM equities, technology and consumer discretionary stocks have led the market higher YTD on the back of very strong earnings growth. With earnings yields of nearly 7.4% on the broad market, EM equities remain among the cheapest segments globally. While U.S. earnings are currently tracking at nearly 10% for the year, most analysts have recently revised their broad EM earnings forecasts higher to nearly 20%.8 In our view, the rebound in EM growth and earnings appears to be much earlier in its cycle than most developed markets.

Dividend Yield vs. Earnings Yield vs. Yield Maturity (%)

In sum, we believe emerging markets represent some of the most compelling opportunities for returns over the next several years despite strong flows and performance YTD. EM FX represents an opportunity to gain exposure to higher carry at historically undervalued spot prices. EM fixed income should continue to deliver strong returns on account of rate cuts from central banks and high carry relative to other forms of non-core fixed income. Finally, with economic momentum and earnings accelerating, EM equities have the potential to continue their already strong year-to-date performance.

1Source: Bloomberg, as of 8/24/17.

2As measured by the J.P. Morgan Emerging Local Markets Index Plus (ELMI+), MSCI Emerging Markets Index and J.P. Morgan Government Bond Index – Emerging Markets

3As measured by the J.P. Morgan GBI-EM Global Diversified Index.

4Source: Bloomberg, as of 7/31/17.

5Source: Bloomberg, for the period 7/31/11–6/30/15.

6Source: JPMorgan, as of 7/31/17.

7Source: Bloomberg, as of 8/24/17.

8Source: Goldman Sachs, as of 8/21/17.

Bradley Krom, Associate Director of Research, joined WisdomTree as a member of the research team in December 2010. He is involved in creating and communicating WisdomTree’s thoughts on global markets, as well as analyzing existing and new fund strategies. Prior to joining WisdomTree, Bradley served as a senior trader on a proprietary trading desk at TransMarket Group. Bradley is a graduate of the Wharton School, University of Pennsylvania.

Bradley Krom, Associate Director of Research, joined WisdomTree as a member of the research team in December 2010. He is involved in creating and communicating WisdomTree’s thoughts on global markets, as well as analyzing existing and new fund strategies. Prior to joining WisdomTree, Bradley served as a senior trader on a proprietary trading desk at TransMarket Group. Bradley is a graduate of the Wharton School, University of Pennsylvania.

Commissions, management fees and expenses all may be associated with investing in WisdomTree ETFs. Please read the relevant prospectus before investing. WisdomTree ETFs are not guaranteed, their values change frequently and past performance may not be repeated. Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates. “WisdomTree” is a marketing name used by WisdomTree Investments, Inc. and its affiliates globally. WisdomTree Asset Management Canada, Inc., a wholly-owned subsidiary of WisdomTree Investments, Inc., is the manager and trustee of the WisdomTree ETFs listed for trading on the Toronto Stock Exchange.