By Alyssa Furtado, RateHub.ca

Special to the Financial Independence Hub

Interest rates in Canada have rarely seen such lows, which makes borrowing money to buy a home pretty attractive. But when you start looking around for the best mortgage rates, homebuyers face a choice of going with a variable-rate or a fixed-rate mortgage.

So what’s the difference? A variable-rate mortgage follows interest rates as they move up and down. And a fixed-rate mortgage is locked in for a certain term. Sounds simple, but deciding which option works for you can depend on a number of factors. Here are some essential pros and cons:

Fixed-rate mortgages

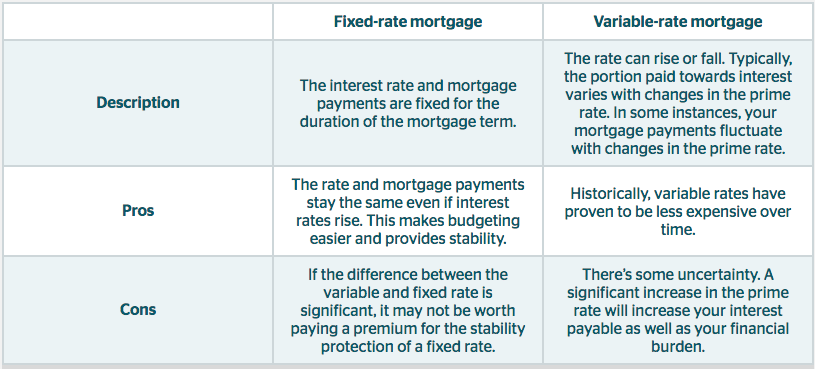

Pro: Added security

You don’t have to worry about whether your payments will change because of economic factors you can’t control during the mortgage term. This makes long-term financial planning much easier.

Say you get a five-year fixed-rate mortgage, with a 2.5% interest rate. Regardless of whether interest rates go up or down elsewhere, the rate will stay at 2.5% for the entire five-year period. This allows you to set it and forget it until it comes time to renew your mortgage, at which point you’ll need to renegotiate your rate. At this point your rate could be higher or lower.

Con: Added expense

The luxury of knowing your rate will remain the same will likely cost you, as fixed rates tend to be higher overall.

Variable-rate mortgages

Pro: You can save a bundle

Although by no means guaranteed, historically borrowers save more money over time with this method. Your rate is correlated to the prime lending rate, which can fluctuate. Your rate is quoted as the prime rate plus or minus a certain percentage, such as prime minus 0.4%. In this instance, if the prime rate is 2.7%, your mortgage rate will be 2.3%. Such a small percentage might not look like it will affect your payments, but the savings will add up significantly over time.

Con: Rates can always go up

The variable-rate option comes with a certain risk. If your bank’s prime lending rate changes, the interest moves up or down in conjunction with it. The amount you actually pay your lender on a regular basis (biweekly, monthly, etc.) won’t necessarily change. If the interest rate goes down, more money from your payment will go toward paying down the principal. If the rate goes up, more of the payment will be eaten up by interest, and sometimes your regular payment can also rise.

Digging deeper

Tools like a mortgage payment calculator can show you what each of these scenarios would look like, in advance.

What do most people choose? A recent Mortgage Professionals Canada report found that in 2016, 68% of all mortgage holders used fixed-rate mortgages, and that number jumps to 84% if you only count first-time buyers.

It’s no real surprise since rates are historically low, it could seem overly optimistic to expect them to go lower. After all, with rates available below 3%, it’s a dramatic difference from the 20% rates being paid by borrowers in the 1980s.

Rates have been trending down ever since so if you’re looking to bet on rates going even lower by using a variable-rate mortgage, it appears that history would be on your side.

Unfortunately, at the moment, that extra risk might not be worth it. Interest rates are already so low, there isn’t much room for the variable rate to go lower, so the savings could turn out to be minimal.

It’s possible to use a combination mortgage, whi allows the payment to be divided, with part based on a fixed interest rate and part on a variable rate. However, this option is much less popular.

Looking at the road ahead

The pros and cons of these two options are based on what is true of interest rates today. But since a mortgage is a potentially decades-long endeavour, it’s important to understand the factors that drive the underlying economic reality.

Variable-rate mortgages are affected when the Bank of Canada (BoC) changes rates to help control inflation. Rates go up when the BoC is trying to curb inflation, since higher rates discourage spending and borrowing. Rates go down when inflation is low and the BoC is trying to pump up economic activity by making borrowing and spending easier.

By adjusting the overnight lending rate — the rate at which banks can lend money to each other in the overnight market — the BoC affects others banks’ ability to lend money to everyone else, including you. This changes the prime rate, which variable-rate mortgages are directly related to.

Fixed-rate mortgages are most directly correlated with Government of Canada bond yields, which can be jostled by a number of economic factors. Therefore, a possibility remains that if your mortgage comes up for renewal after the term is up, the rate you’ll get may be different.

Choosing between a fixed-rate or a variable-rate mortgage can be difficult. A fixed rate will provide you with peace of mind in the event rates rise. But if rates fall, a variable-rate mortgage will be the better option.

Alyssa Furtado is a passionate entrepreneur, financial expert, digital marketer and educator, and founder of RateHub.ca, a website that compares mortgage rates, credit cards, high-interest savings accounts, chequing accounts, and insurance with the goal to empower Canadians to search smarter and save money.

Alyssa Furtado is a passionate entrepreneur, financial expert, digital marketer and educator, and founder of RateHub.ca, a website that compares mortgage rates, credit cards, high-interest savings accounts, chequing accounts, and insurance with the goal to empower Canadians to search smarter and save money.