My latest MoneySense Retired Money column, just published, looks at the role Guaranteed Investment Certificates (GICs) should play in the retirement portfolios of Canadians. You can find the full column by going to MoneySense.ca and clicking on the highlighted headline: Are GICs a no-brainer for retirees?

My latest MoneySense Retired Money column, just published, looks at the role Guaranteed Investment Certificates (GICs) should play in the retirement portfolios of Canadians. You can find the full column by going to MoneySense.ca and clicking on the highlighted headline: Are GICs a no-brainer for retirees?

(If link doesn’t work try this: the latest Retired Money column.)

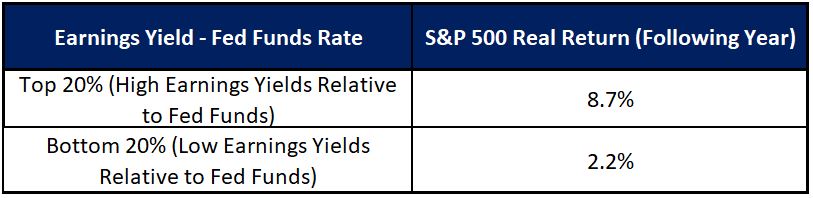

Now that you can find GICs paying 5% or so (1-year GICs at least), there is an argument they could be the bedrock of the fixed-income portfolios, especially now that the world is embroiled in two major conflicts: Ukraine and Israel/Gaza. Should this embolden China to invade Taiwan, you’re starting to see more talk about a more global conflict, up to an including the much-feared World War 3.

Of course, trying to time the market — especially in relation to catastrophes like global war and armageddon — generally proves to be a mug’s game, so we certainly maintain just as much exposure to the equity side of our portfolios.

I don’t think retirees need to apologize for sheltering between 40 and 60% of their portfolios in such safe guaranteed vehicles. Certainly, my wife and I are glad that the lion’s share of our fixed-income investments have been in GICs rather than money-losing bond ETFs: the latter, and Asset Allocation ETFs with heavy bond exposure, were as most are aware, badly hit in 2022. But not GICs; thanks to a prescient financial advisor we have long used (he used to be quoted but now he’s semi-retired chooses to be anonymous), we had in recent years been sheltering that portion of our RRSPs and TFSAs in laddered 2-year GICs. Since rates have soared in 2023, we have gradually been reinvesting our GICs into 5-year GICs, albeit still laddered.

The MoneySense column describes a recent survey by the site about “Bad Money advice,” which touched in part on GICs. Almost 900 readers were polled about what financial trends they had “bought into” at some point. The list included AI, crypto, meme stocks, side hustles, tech and Magnificent 7 stocks and GICs. Perhaps it speaks well of our readers that the single most-cited response was the 49% who said “none of the above.” The next most cited was the 16% who cited a “heavier allocation to GICs.” You can read the full overview here but I did find a couple of other findings to be worthy of note for the retirees and would-be retirees who read this column: Not surprisingly, tech stocks (FANG, MAMAA. etc. were the first runnerup to GICs, receiving 13.24% of the responses. Not far behind were the 10.55% who plumped for crypto and NFTs (Non-fungible tokens). AI was cited by 3.7%: less than I might have predicted; and meme stocks were only 2.81%.

As I said to executive editor Lisa Hannam in her insightful article on the 50 worst pieces of financial advice, GICs are at the opposite end of the spectrum from such dubious investments as meme stocks and crypto. (I’d put Tech stocks and A.I. in the middle).

GICs won’t grow Wealth for younger investors, aren’t tax-efficient in non-registered accounts

The GIC column passes on the thoughts of several influential financial advisors. One is Allan Small, a Toronto-based advisor who occasionally writes MoneySense’s popular weekly Making Sense of the Markets column. He is among GIC skeptics. He told me his problem with GIC is that they “don’t grow wealth. They can act as a parking lot for money for some people but over time there have been very few years in which people have made money with GICs, factoring in inflation and taxation.” Continue Reading…