By Dale Roberts, Retirement Club/Cutthecrapinvesting

Special to Financial Independence Hub

Bonds may be the adult in the room, but they are certainly afraid of inflation. Bonds usually do their thing: they go up when stock markets get hit hard. They provide ballast. During periods of expected high inflation, or during rising inflation bond prices go down. That can create and contribute negative returns. The bonds can contribute to a portfolio decline.

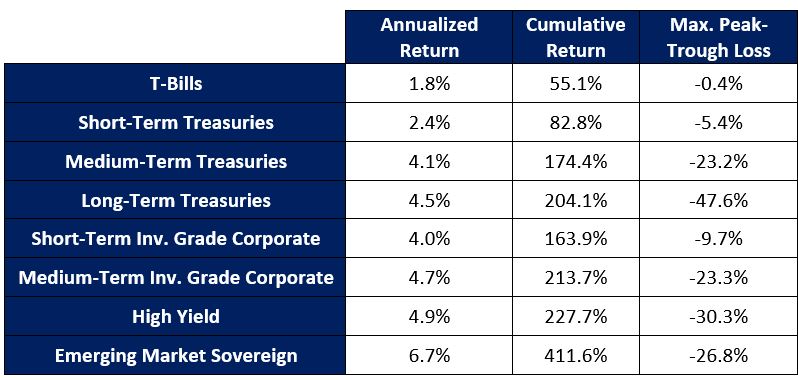

But not all bonds are the same. Ultra-short bonds carry no price risk, while long-term bonds can carry extreme price risk. It’s crucial that investors understand the ‘types of bonds.’ To intermediate- and long-term bonds, inflation is Kryptonite. How do we battle that force?

As always, the following is not advice.

As a refresher, be sure to have a read of: Stocks are the unruly kids. Bonds are the adult in the room.

Too funny, a rare case when Cut The Crap Investing actually ranked high on search.

Inflation up. Bonds down.

Bond yields rise during inflation primarily because investors demand higher returns to compensate for the reduced purchasing power of future fixed interest payments. Furthermore, inflation often prompts central banks to raise interest rates, which directly drives up yields, while existing bond prices fall to align with new, higher-yielding securities.

As interest rates rise due to inflation, new bonds are issued with higher coupon rates to attract investors. Existing bonds, which pay lower interest rates, become less attractive and must drop in price to remain competitive, which simultaneously increases their yield.

Join us at Retirement Club

We’ve had some recent experience with the inflation scare of 2021 and into 2022. The bond market (XBB-T) experienced one of its worst performances in 2022, losing around 11% or more as inflation surged, reversing a four-decade bull market in fixed income.

In the above chart we see that bonds provided no ballast. Quite the opposite. That said, we have to keep in mind that bonds have done their thing in every major recession. They stink the joint out, one time, and investors turn on them.

Traditional global stock and bond portfolios have delivered wonderful returns …

Inflation fighters and the all-weather portfolio

In mid-March we had a refresher on what works during inflation with: How do we defend against stagflation?

If you have dedicated inflation fighters in the portfolio you’re not too worried about bonds delivering negative returns. We know that stocks don’t always go up. It’s the same for bonds.

In the following chart, we’ll start in 2021. Markets think ahead, of course, and enough investors loaded up on inflation-fighting assets as inflation storms gathered in 2021. The Purpose Real Asset ETF (PRA-T) is a nice one-stop inflation-fighting shop.

PRA-T was up 23.5% in 2021 and 15.9% in 2022.

Add 20% PRA-T to 80% XBAL-T and we have annual returns over 10% with no negative years from 2021 through 2023.

Continue on into 2026 and it gets even better. PRA-T is up almost 16% in 2026.

Go short and clip the inflation price risk

Ultra-short-term government bonds (CBIL-T) do not carry price risk: they are cash-like. In fact, they will provide greater and greater income as inflation expectations and yields rise. Continue Reading…