The dramatic impact of longevity on organizations was predicted decades ago. Indeed, in 1961, President John F. Kennedy put a formal structure in place to ensure that Congress would be attentive to the opportunities and challenges increased life expectancy presented to existing programs and policies. Since science had added years to our lives, Kennedy’s vision was to ensure added life to our years.

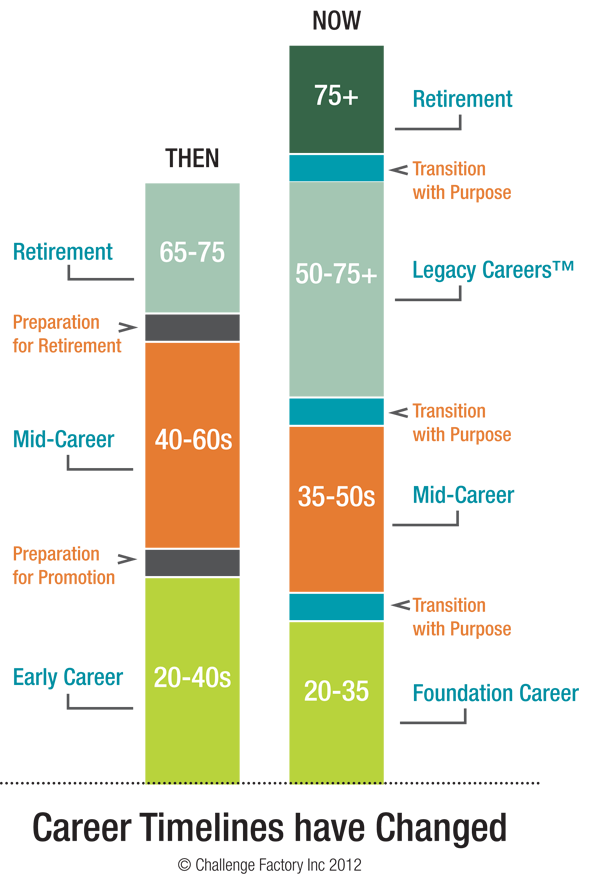

Longer life expectancy implies longer workspan

One corollary: increased life expectancy means longer work-life too. Continue Reading…

Are the Baby Boomers part of the Ageless Generation?

Many of us seem to act as if that were the case but there’s little doubt most of us feel younger than we appear. To me, the poster child for this ageless generation is Jane Fonda, whose famous workout videos appear to have held her in good stead in her personal twilight career.

(Technically, since she was born in 1937, Jane Fonda is not a post-war baby boomer but her spirit certainly seems to epitomize the zeitgeist of the generation that came soon after her).

If you get Netflix check out the recently released series Grace & Frankie, where Fonda plays a 70-year old recent divorcee: even though she herself is actually 77! Equally vibrant are her aging costars: Lilly Tomlin, Martin Sheen and Sam Waterston (best known as the prosecutor on Law & Order). Tomlin is 75 and the two male co-stars are 74.

Medical advances will transform the global economy

Amazon.com

The Ageless Generationalso happens to be the title of a recent (2013) book by Dr. Alex Zhavornonkov, director of the Biogerontology Research Foundation and founder of the International Aging Research Portfolio. It’s one of about a dozen books I read in recent months in preparation for a talk on Longevity that I gave on Monday to the National Elder Planning Issues Conference in Niagara Falls.

The book’s subtitle summarizes the gist of it: How advances in biomedicine will transform the global economy. Since the focus is on the United States, it will come as no surprise that Zhavornonkov believes breakthroughs in extending Longevity can only make a shaky Social Security and Medicare system that much more fragile in the United States, and by extension their equivalent programs in other advanced nations.

Regular Hub readers will know that if I had my druthers, the headline would read more like “Why Work won’t end after your Findependence Day.” (that is, the day you achieve Financial Independence).

I don’t view the terms Retirement and Financial Independence as interchangeable. By definition, Retirement (or at any rate, traditional full-stop Retirement funded with a generous Defined Benefit pension) means no longer working for money. Financial Independence (aka Findependence), on the other hand, can occur years and even decades before traditional Retirement and so seldom means the end of productive work.

This very web site — which just passed six months in existence — is dedicated to clarifying this distinction. And of course the site also constitutes a big element of my own personal Encore Act: next Tuesday will be the one-year anniversary of my own Findependence Day. In my case, I define that as no longer working as an employee of a giant corporation or government entity, and having the financial resources to work if I choose to, and not if I don’t.

Finance Minister Joe Oliver (Department of Finance/Flickr)

By Jonathan Chevreau

Journalists and financial experts will be entering a “Lock-up” this morning in Ottawa, getting roughly a six-hour head start on the rest of us on the contents of the 2015 federal budget.

Even so, a combination of leaks and informed speculation give us a pretty good idea about the contents, which will gush forth within seconds of 4 pm, when the embargo is lifted.

Here at the Financial Independence Hub, we will be focusing on three main measures that if announced will do much to speed or improve our collective “Findependence.” Our hoped-for “trifecta” from Finance Minister Joe Oliver (pictured above) includes the much-delayed promise of a doubling of annual TFSA limits, a lowering of minimum withdrawal limits for RRIFs, and lower tax rates for small business. Continue Reading…

So you and your spouse have decided to retire. At some point in your retirement planning you must ask yourself where you would like to spend your Golden Years. The following questions and insight should place you on the right path for finding just the location that suits your needs.

First things first

The first question you must ask yourselves is whether you want to stay in the home in which you are currently living or would like to move elsewhere. Retirement is a big step. Sometimes people feel more secure staying in familiar surroundings because it makes the transition to your new lifestyle smoother. Others, for financial reasons, a change of pace, health reasons, or for better weather, want to relocate. In this case, the next decision you must make is whether you want to stay in your home country or move overseas.

If you want to stay in your home country you must decide what sort of climate is most attractive to you. Do you want to experience the four seasons or have a more moderate, year-round climate? Do you like mountains or beaches? What size of city or town do you most enjoy? These questions are important because they automatically exclude places you won’t need to research. Knowing what you prefer in climate, city size and geographical configuration carries a lot of weight in terms of your happiness quotient.

Another thing to consider is that if you choose a town or small city, are there adequate medical facilities nearby? Larger cities tend to have a full range of medical care. Smaller towns generally have clinics and a variety of doctor’s offices, but perhaps not the equipment needed for complex medical situations.