Hi, it’s Dale Roberts here. You know me from Cut The Crap Investing. My blog posts are often shared on Findependence Hub.

Similar to Jonathan Chevreau I have a keen interest in helping Canadians prepare for retirement and make the most of retirement once they reach that wonderful stage in life.

Too many Canadians enter retirement with some sense of anxiety. They may fear that they will outlast their money. They might not have created the all important life plan.

More and more Canadians have self-directed their investment accounts. Now they need a resource that helps them set the course, and keep the course for a successful retirement.

Retirement Club is a community of like-minded Canadian retirees and near retirees.

A successful retirement starts with financial security. Let’s call that fiscal fitness. We cover the financial essentials, in jargon-free plain-speak with clear demonstrations. You’ll learn how to spend down your portfolios in an efficient fashion. You’ll learn how to use free-use retirement calculators that create optimal retirement cash flow plans. That is, how to spend from your investment accounts, working in concert with CPP, OAS, pensions, and other income.

The retirement portfolio will be discussed in detail. We need to align each account’s risk level to the task at hand: dictated by that retirement cash flow plan.

As you may know, at Cut The Crap Investing I’ve offered a unique approach to managing risk: using lower volatility and defensive equities (consumer staples, healthcare and utilities) in concert with traditional risk managers such as cash, bonds, GICs, gold, annuities and more. During the volatility of 2025, these defensive assets have been the top performers.

Of course the financial topics are numerous, from wills and estates, to insurance, tax tips, healthcare costs and more.

Retirement by design

Next comes the life plan. Each of us will decide on our level of travel and entertainment, family time, leisure and living life full of purpose. We’ll provide and share lifestyle inspiration. We’re doing it right when financial security enables a rich and rewarding lifestyle. We need to retire with vitality and purpose. How do we replace the ‘good stuff’ we got out of our working years?

How do we learn and connect?

At a minimum we’ll have …

A monthly one hour Zoom presentation (the next one is April 25th at noon).

A monthly newsletter

The Zoom presentations are lively and interactive. They start with a learning session but move on with Clubbers asking questions and taking part in break out sessions. We end with a 15 minute ‘after party.’ It’s a Club environment.

Discover the transformative power of financial independence as industry leaders reveal how it can redefine success and enhance mental health. This article delves into the pivotal role of autonomy over time, the serenity that comes with automating finances, and the decreased stress from a strategic career pivot. Gain exclusive insights from authorities in the field on how saying no, embracing failure, and prioritizing family can lead to a life of fulfillment and stability.

Success Means Control Over Time

Automating Finances Brings Peace

Switch to Consulting Reduces Stress

Freedom to Design My Life

Saying No Reduces Stress

Freedom to Pursue Joyful Opportunities

Control Over Time and Decisions

Family Time Over Career Goals

Focus on Long-Term Stability

Monetization Strategy Brings Happiness

Failures as Stepping Stones

Success means Control over Time

At the start of my career, I was obsessed with proving myself. I took on every case, worked ridiculous hours, and measured success by the number of wins I had under my belt. I thought the more I worked, the more successful I would be. But eventually, I hit a point where I was financially comfortable, and I realized I was still just as stressed as when I started. That was when I began prioritizing Financial Independence, and my definition of success completely changed. In the present time, I see success as having control over my time and my future.

A great example of this shift was when I started making decisions that were not just about revenue but about sustainability. I turned down high-stress cases that were not worth the mental drain, hired more attorneys to distribute the workload, and focused on building a firm that could function without me handling every single detail. That shift meant I no longer felt like I had to be on call 24/7, and my stress levels dropped dramatically. — Gordon Hirsch, Founder and Managing Attorney, Hirsch Law Group

Automating Finances brings Peace

When I started my career, I defined success by wealth and status-what I could buy and show off. I believed the more I had, the more successful I’d be. But when I shifted my focus to Financial Independence, everything changed. I realized that true success isn’t about accumulating things; it’s about having peace of mind and long-term security.

A turning point for me was automating my savings and investments. Before that, I was constantly stressed about money. Once I set everything to run automatically, I no longer had to worry. That simple change gave me mental space, allowing me to live freely without financial anxiety. Now, success is about feeling in control of my future. This shift has significantly improved my mental health, bringing me a sense of calm I never had before. — Brian Staver, CEO, Net Pay Advance

Switch to Consulting reduces Stress

I used to define success almost exclusively in terms of career milestones, like job titles, salary increases, or the prestige of my workplace. After I started focusing on Financial Independence, I began measuring success by how much control I had over my time and decisions, rather than by external markers. This shift significantly reduced my stress levels because I no longer felt tied to an intense “always-on” mentality just to climb the corporate ladder.

Once I established multiple income streams and built a solid emergency fund, I felt empowered to switch to a part-time consulting role, which opened up space for personal pursuits, like volunteering and hobbies that I’d never made time for before. Having that buffer of financial stability made it easier to prioritize my well-being and mental health, rather than constantly chasing traditional measures of success. — Inge Von Aulock, Investor & Chief Financial Officer, Invested Mom

Freedom to Design my Life

Success used to mean chasing titles, climbing the corporate ladder, and hitting traditional milestones like bigger paychecks, promotions, and external validation.

But once I started prioritizing Financial Independence, my perspective shifted entirely. Now, success is not about how much I earn but how much freedom I have to design my life on my terms.

Instead of measuring success by status or salary, I now define it by:

Time freedom: Having control over how I spend my days.

Choice and flexibility: Not being tied to a paycheck or forced into decisions based on financial constraints.

Peace of mind: Knowing I have a safety net that allows me to take risks and say no to things that don’t align with my values.

Letting go of the pressure to constantly “achieve more” has been a huge relief.

Before, I felt trapped in an endless cycle of stress, overworking, and burnout, thinking that success meant sacrificing my personal well-being. Now, I feel more grounded, in control, and mentally at peace because my goals align with what truly matters to me.

A few years ago, I would have never considered stepping away from a high-paying job, fearing financial insecurity. But after working toward Financial Independence, I had the freedom to turn down a promotion that would have required longer hours and more stress.

Instead, I chose to focus on projects that align with my passions, knowing that my financial foundation gave me that choice.

The result? Less stress, more fulfillment, and a life I genuinely enjoy living.

Prioritizing financial independence has taught me that success is not about accumulating wealth but about having the freedom to live on your own terms. And that shift has made all the difference in my mental well-being. — Chinyelu Karibi-Whyte, Self-Care, Mindfulness & Resilience Advocate, Pheel Pretty

Saying “No” reduces Stress

When I first started in real estate, success was all about numbers: closing deals, growing revenue, and hitting milestones. I measured everything in dollar signs and transactions. But as I gained financial independence, my perspective shifted. Success became less about accumulation and more about impact-on my team, community, and well-being.

One of the biggest changes was learning to say no. Early in my career, I took on every client, every opportunity, afraid that turning something down meant losing ground. But once I reached a place where I wasn’t financially desperate for the next deal, I could be more selective. I could focus on working with people who aligned with my values and on projects that truly excited me. That shift reduced my stress dramatically. Instead of constantly feeling pressured to chase, I started making strategic and fulfilling decisions.

A clear example of this is Pepine Gives, my nonprofit focused on helping at-risk families. Years ago, I wouldn’t have had the bandwidth to pour energy into something like this because I was too busy trying to build stability. Now, I can invest time and resources into causes that matter because I’m not in survival mode. And that has brought me a fulfillment that no commission check ever could.

Financial Independence hasn’t made me work less: it’s made me work differently. My business is stronger because my priorities are clearer, and my mental health is better because I’m no longer tied to a definition of success that’s purely financial. Instead, success is about creating lasting change, lifting others up, and building a legacy beyond real estate. — Betsy Pepine, Owner and Real Estate Broker, Pepine Realty

Freedom to Pursue Joyful Opportunities

Success used to mean chasing milestones that felt like they were chosen for me: a high-paying job, owning the latest gadgets, or even maintaining a certain image of “having it all together.” Financial Independence rewired that definition entirely. Now, success isn’t about accumulation: it’s about freedom. It’s the ability to say “no” to things that don’t align with my values and “yes” to opportunities that spark joy or growth, even if they don’t come with a paycheck attached.

One example: I turned down a promotion that would’ve come with a significant pay bump because it demanded longer hours and constant availability. Ten years ago, I would’ve felt like I was throwing away an opportunity. But prioritizing financial independence allowed me to see it for what it was: a trade-off that would’ve cost me my time, health, and peace of mind. Instead, I used that time to start freelancing in a field I love, and ironically, I ended up replacing that lost income in a way that didn’t burn me out. Continue Reading…

An RBC poll finds Canadians believe they’ll need almost $850,000 to ensure an independent financial future

By Craig Bannon, CFP, MBA, TEP

(Special to Findependence Hub)

For many Canadians, Financial Independence is the ultimate goal: a future where they can live comfortably, support themselves and their families and enjoy their desired lifestyle without the constant stress of striving to make ends meet.

However, with ongoing market fluctuations, a higher cost of living, and overall economic uncertainty, reaching that milestone may feel more challenging than ever before. Many individuals find themselves trying to navigate a complex financial landscape, where saving for retirement and other financial goals requires careful planning and informed decision-making.

Findings from the recent RBC Financial Independence Poll indicate that Canadians believe they need an average of $846,437 to ensure an independent financial future : which they variously described as “having a nest egg large enough to enjoy my retirement,” “not living paycheque to paycheque” and being “debt free.” In some regions, that number is even higher: respondents in the Prairies, for example, estimate they’ll need an average of $958,535. Among generations, Gen X (aged 45 to 60) anticipates needing over a million dollars to achieve Financial Independence.

Investing a Key Strategy for Growth

With such ambitious targets, investing has become a crucial strategy for many Canadians. Nearly half (49%) of poll respondents say they invested in 2024, with Gen X and Millennials participating at similar rates. But concerns linger, with nearly half of all respondents (48%) calling out market volatility and investment performance as a key worry, with this concern jumping to over half (54%) for Millennials.

However, while markets fluctuate, one constant remains: the value of having a strong financial plan based on one’s goals, with a long-term investing strategy to implement, to help investors stay the course through market ups and downs. The encouraging news: 51% of Canadians say they have a financial plan, either formal or informal. Those with a plan report feeling more confident (42%) and reassured (30%) about their financial future.

Staying the Course and Seeking Professional Guidance

For those hesitant to re-start – or begin – investing, waiting for the ‘perfect’ moment to invest may mean missing out on valuable growth opportunities. Time in the market, rather than timing the market, is important. The sooner you can invest and the longer you can be invested, the greater the opportunity to potentially benefit from the gradual growth that markets and economies can experience over the long term. Continue Reading…

Over the years, I have come to really like the all-in-one ETFs from Vanguard and iShares. I like these ETFs because they are a simple way to diversify your portfolio across different sectors and countries. These ETFs also automatically rebalance regularly, making an investor’s life much easier.

Due to the popularity of the all-in-one ETFs, both TD and BMO also created similar ETFs. Which company offers the best all-in-one ETFs? Are TD ETFs better? Are iShares ETFs better? Are Vanguard ETFs better? Or are BMO ETFs better?

Let’s find out!

TD ETFs

TD has many different ETFs, including active ETFs, special focused ETFs, and broad market index ETFs that are well-suited for different investment strategies. When it comes to all-in-one ETFs, TD offers three different ETFs that were created in 2020:

All three of these TD all-in-one ETFs have a MER of 0.17%. This means if you have $1k invested in one of these ETFs, you effectively would pay $1.7 in fees every year, which is extremely cheap if you think about it.

Here are the historical performances of these three ETFs:

1 Yr

2 Yr

3 Yr

TCON

12.48%

9.63%

4.41%

TBAL

19.27%

14.96%

8.04%

TGRO

26.27%

20.16%

11.70%

You can buy and sell all three ETFs via online brokers. Since many brokers offer commission-free trades nowadays, you can buy one of these all-in-ones regularly and build up your portfolio.

Sign up with Wealthsimple using my referral code (or type in YDC3NA) and get a $25 reward for simply signing up.

Sign up with Questrade using my referral code (or type in 826124747428063) and get a $50 reward.

BMO ETFs

Like TD, BMO offers five different all-in-one ETFs (BMO calls them Asset Allocated ETFs).

VRIF has an MER of 0.29%, while the other five all-in-ones have an MER of 0.22%. VRIF probably has a slightly higher MER because of the fund structure. Interestingly enough, Vanguard all-in-ones have the highest MER out of the four fund companies (I said this because historically Vanguard has lead the way when it comes to lowest MER).

Here are the historical performances of the Vanguard all-in-one ETFs:

1 Yr

3 Yr

VCIP

8.90%

1.99%

VRIF

10.44%

3.08%

VCNS

13.61%

4.45%

VBAL

18.40%

6.90%

VGRO

23.39%

9.39%

VEQT

28.40%

11.83%

The best all-in-one ETFs for your investment portfolio

As you can see, all four fund companies offer all-in-one ETFs with different asset exposures. Which are the best all-in-one ETFs for your investment portfolio?

Well, that is totally dependent on your risk tolerance and your investment timeline.

If you are an investor who is approaching retirement or is already retired, you might want to invest in something more conservative. In other words, you don’t want to lose sleep whenever there’s a market correction. For you, a steady investment income and stable portfolio value growth is more important. Therefore, you probably will go with either a conservative all-in-one ETF or a balanced all-in-one ETF.

If you are younger with a longer investment time horizon, you want to aim for portfolio growth. Therefore, you’d probably go with either a growth all-in-one ETF or an all-equity ETF to maximize your return over the long term.

Best Conservative All-in-One ETF

As mentioned, if you are a conservative investor who needs a steady investment income with stable portfolio value growth, a conservative all-in-one ETF is probably the best choice for you.

The question is, which conservative all-in-one ETF is the best?

Let’s compare TCON, ZCON, XINC, XCON, VCIP, VRIF, and VCONs all of which are heavily exposed to fixed income.

Fixed income to equities Mix

MER

1 yr return

3 yr return

5 yr return

Yield %

TCON

70-30

0.17%

12.48%

4.41%

N/A

2.26%

ZCON

60-40

0.20%

13.94%

4.79%

4.87%

2.45%

XINC

80-20

0.20%

9.97%

2.81%

2.86%

2.70%

XCON

60-40

0.20%

14.38%

5.07%

5.35%

2.17%

VCIP

80-20

0.25%

8.90%

1.99%

2.11%

2.86%

VRIF

70-30

0.32%

10.44%

3.08%

N/A

3.55%

VCON

60-40

0.24%

13.61%

4.45%

4.71%

2.51%

Among ZCON, XCON, and VCON, which all have the same 60-40 mix, it’s interesting to see that XCON had the best returns consistently, but XCON has the lowest distribution yield.

Among TCON, XINC, VCIP, and VRIF, TCON has had the highest returns, most likely due to the lower MER fees.

Not surprisingly, ETFs with a higher exposure to stocks have had higher returns in the last five years. Continue Reading…

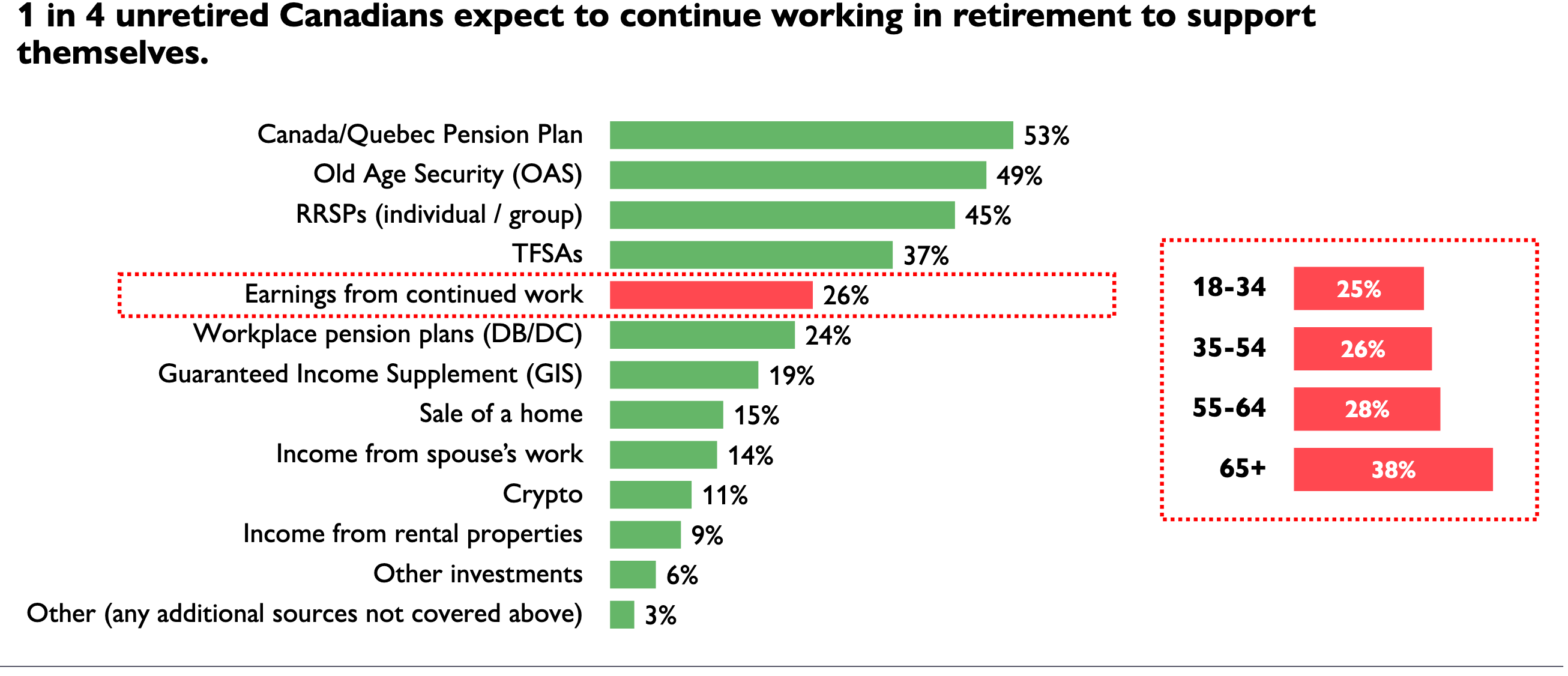

Even before the Tariffs threats emerged under Trump 2.0, Canadian seniors were starting to find the economic uncertainty and rising living costs to be unmanageable. No surprise then that many seniors approaching Retirement Age are delaying their exit from the workforce.

According to a report by HealthCare of Ontario Pension Plan, 28% of unretired Canadians aged 55-64 say they expect to continue working in retirement to support themselves financially. Here’s a screenshot from the HOOPP survey:

The Healthcare of Ontario Pension Plan (HOOPP) commissioned Abacus Data to conduct its sixth annual Canadian Retirement Survey in the spring of 2024. The latest survey finds “persistent high interest rates and a rising cost of living continue to have a significant negative impact on Canadians’ ability to save and manage the cost of daily life, threatening their retirement preparedness.” While all Canadians are struggling, “women and those closest to retirement are especially hard hit with lower savings and higher levels of financial stress.”

While most Canadians are struggling to save amidst a high cost of living, HOOPP finds women are particularly affected. Half (49%) of all Canadian women have less than $5,000 in savings and almost a third (28%) have no savings (compared to 33% and 17% of men, respectively), similar to the 2023 results

The MoneySense column also looks at more recent Retirement surveys that also reveal anxiety about rising costs of living. One is from Bloom Finance Co. Ltd., conducted by founder Ben McCabe after Trump’s Tariffs started to kick in this year.

A Bloom study conducted with Angus Reid found 46% of Canadians thinking of working part-time in Retirement. That’s in line with a Fidelity survey in 2024 that found half of Canadians plan to delay Retirement. According to the Bloom Report [in March 2024], 67% of Canadian homeowners over 55 were concerned their savings would not sustain their quality of life through retirement. Only 29% considered downsizing or alternative living situations to access their home equity earlier than expected. 59% of the same cohort agreed accessing micro-amounts of their home’s equity would help maintain their desired living standard. Continue Reading…

What is Retirement Club?

What is Retirement Club?