With economic uncertainty looming, taking control of your household finances is more important than ever. Preparing for potential downturns doesn’t mean drastic lifestyle changes: it means implementing smart, practical strategies that safeguard your financial well-being. By making a few savvy adjustments, you can create a solid buffer that shields your household from the effects of a recession while keeping your long-term financial goals on track.

Launch a Side Business

Starting a side business can be a powerful way to add extra income and recession-proof your finances. Whether you’re leveraging a hobby, tapping into a specialized skill set, or exploring new opportunities, a small business can provide a flexible, low-risk way to diversify your income. Consider ventures that align with your interests, such as freelancing, consulting, or offering home services, which tend to remain in demand even during tough times. By starting small and focusing on industries that offer consistent value, you can gradually build a side income that provides financial stability when it’s most needed.

Pay Down your Debt

Paying down debt is one of the most effective ways to strengthen your financial position ahead of a recession. High-interest debt, such as credit-card balances or personal loans, can quickly eat into your budget, making it harder to manage everyday expenses when the economy tightens. Focus on prioritizing payments to reduce or eliminate this kind of debt, starting with the highest interest rates. This not only frees up more of your income but also reduces financial stress. By becoming less reliant on borrowed money, you can better weather potential income fluctuations and maintain greater control over your finances.

Organize your Financial Records

Organizing your financial records can have many benefits, such as improved efficiency, better decision-making, and easier access to important information. Digitizing your documents can help you keep track of them more easily, save space, and add an extra layer of security to protect against theft or damage. After digitizing your records, try the process of splitting PDF content to break a document into smaller, more manageable files. Continue Reading…

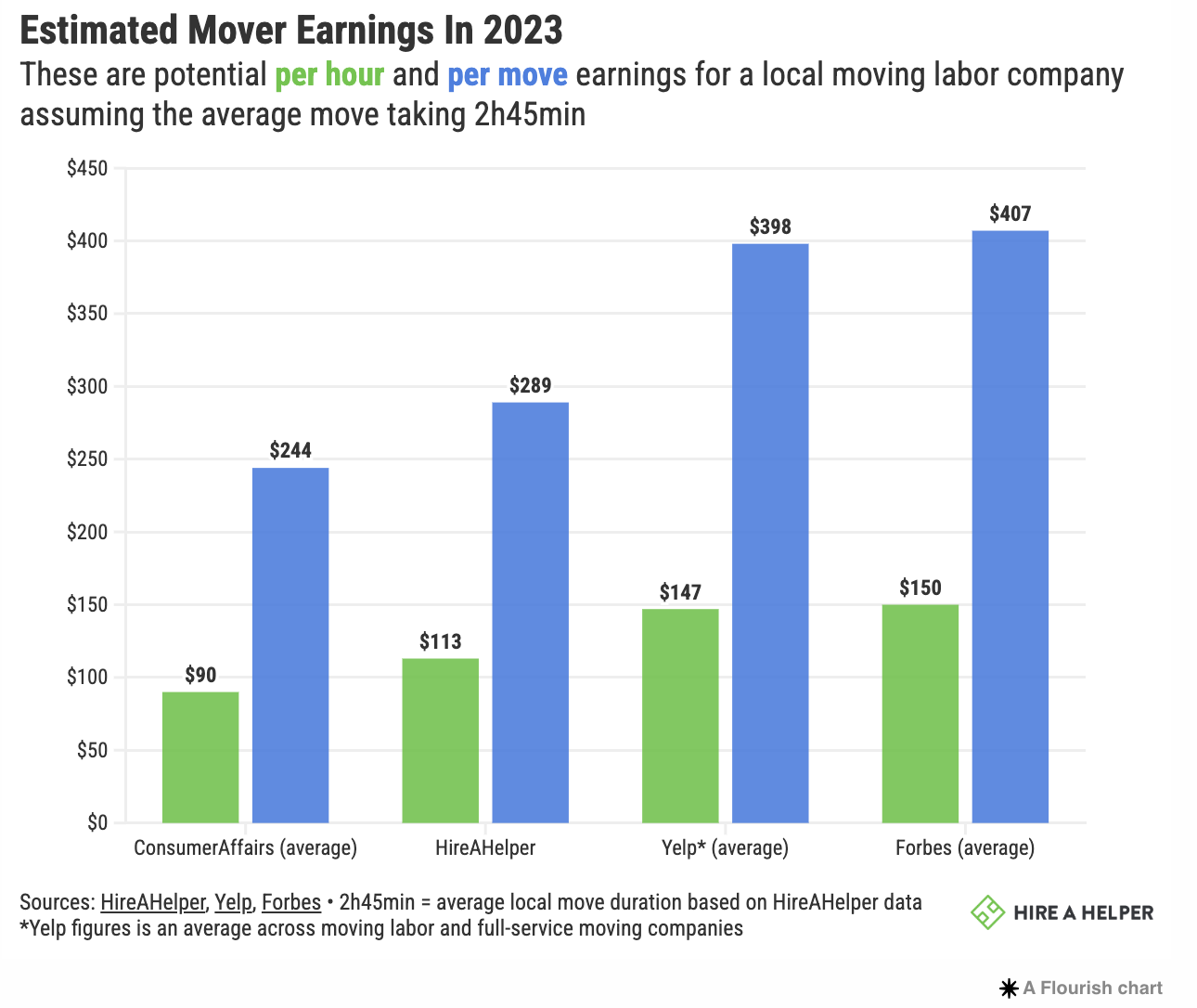

2023-2024 HireAHelper Moving Migration Report: Artwork by Esther Wu

By Volodymyr Kupriyanov

Special to Financial Independence Hub

When we released our last study of starting a moving labor company as a side hustle, it was a great time to get into the business. Home sales were at an all-time high, and the number of Americans who moved that year inched up for the first time in a decade.

However, after only one year, the housing market has cooled off. And even though sales of newly built homes are still up 6%, home sales as a whole aren’t as high as last year.

The cost of moving has also grown 4% in 2023 (ahead of inflation rates), and this is actually good news! It means movers’ earnings have most likely also increased. So if you’re interested in adding a side hustle to your income, starting a moving labor company is well worth considering.

Findings from 2023 Study on Moving Labor

In 2023, a typical moving company earns between US$90 and $150 per hour on average, or from $244 to $407 per move

Mover earnings in 2023 are highest in Birmingham, AL where average hourly earnings on a labor-only move reached $146

The state with the greatest demand is Mississippi, with 434 moves per moving company registered in the state

What is a Moving Labor Company, and can it work as a Side Hustle?

You can start a side hustle as a full-service mover. These are the huge van line companies, and they tend to offer the whole service package and charge significantly more. Moving labor companies are often responsible for loading, unloading, and, sometimes (though rarely), packing up people’s possessions.

Why is labor-only so profitable?

Here are a few more reasons why moving labor is a good choice for a side hustle:

You don’t require a special mover’s license in most states

No need to invest in your own truck or spend money on gas

With almost half (48%) of all moves taking place on the weekend, you can keep this side hustle alongside your main job or your studies

Fast Facts about Moving Company Earnings in 2023

Here are some estimates on moving marketplace earnings:

How much revenue do movers make per hour?

In 2023, the average amount a moving labor company earned on HireAHelper is $113 per hour (after fees). That rate is based on the service of two movers loading and unloading a customer’s belongings and does not include potential tips.

According to Forbes, local movers usually charge between $50 to $250 per hour in 2023. Continue Reading…

In the quest for Financial Independence, digital products stand out as a versatile and scalable source of income.

We’ve gathered insights from nine business leaders, including entrepreneurs, creators, and coaches, to share their success stories.

From pivoting to evergreen design templates to automating market gap solutions with your platform, discover how these professionals have created and monetized digital products.

Pivot to Evergreen Design Templates

Monetize Niche Books via KDP

Break Down Consulting to Manageable Engagements

Sell Bulk Online Training Programs

Create a Recurring Revenue Product

Offer Personalized Digital Journals with Subscriptions

Gamify a Toolkit Subscription

Develop Financial Tools for Entrepreneurs

Automate a Market Gap Solution with Your Platform

Pivot to Evergreen Design Templates

After burning out as a done-for-you service provider, I pivoted my web design expertise into strategic website templates that I created once and sold over and over again! Then, as I learned more about marketing and selling digital products, I went on to teach others how to package up their knowledge, processes, and shortcuts into paid digital products too. These days, I sell digital products directly from my website using a mix of evergreen and live-launch strategies, which make up more than my old service provider income! — Michelle Pontvert, Digital Product Coach & Creator, Michelle Pontvert

Monetize Niche Books via KDP

I’ve built a sustainable revenue stream by creating books through Amazon’s Kindle Direct Publishing (KDP) platform. Each book was tailored to the niche topics of my blogs, offering specific, useful insights to my audience.

As my blogs grew to over 50,000 monthly sessions, I strategically promoted these books within relevant articles, reaching readers already interested in the subject matter. This alignment between my content and products not only increased book sales but also played a key role in supporting my financial independence. — Alexander Weber, Founder, Axlek

Break Down Consulting to Manageable Engagements

We monetized our consulting services by quickly breaking them down into bite-sized, manageable engagements. This strategy helped us generate over $1M in services on platforms like Fiverr Pro. These platforms allow you to build a network and trust in a marketplace while continually testing new offerings.

The key is to take what you know, package it, and start selling. Start small and gradually add layers. The freemium model works well if you can convert digital downloads into meaningful actions that lead to a relationship, sale, or partnership. Always keep the end goal in mind: growing sales and building long-term value. — Mike Zima, Chief Marketing Officer, Zima Media

Sell Bulk Online Training Programs

As part of my training and coaching business, I created an online training program for managers called Manager Boot Camp. It’s a 23-lesson course delivered over 8 weeks to managers of all levels. The key to this program and how it adds substantially to my financial independence is that it is sold in bulk to companies. Bulk sales bring a higher revenue per transaction. Manager Boot Camp is currently 55% of my annual revenue.

Additionally, most online courses have very little overhead and administration required to run them, which boosts their profitability. Manager Boot Camp and other mini-courses have set me up to head into retirement with a ‘passive’ income stream that doesn’t require my time in person to train or coach clients. — Cecilia Gorman, Management Training Consultant, Manager Boot Camp

Create a Recurring Revenue Product

As the founder of Rocket Alumni Solutions, I’ve created digital products to build revenue and support my financial independence. Within our first year, we launched an interactive touchscreen wall of fame that provides schools and athletic organizations a modern way to recognize student achievement. The software generates over $2M in annual recurring revenue through 500+ subscribers.

To gain our initial set of clients, I spent 6 months cold-calling schools to understand their challenges in alumni engagement and student recognition. This research led to building a touchscreen solution to digitize their awards display. We started by offering free on-site consultations where I would showcase a custom demo and propose three package options at $3,000, $10,000, or $25,000 per year based on the school’s needs. Nearly every consultation resulted in a multi-year contract.

Once we had 50 schools signed up, I hired developers to build a scalable SaaS product. We now charge $5,000 to $50,000 per year, depending on the number of touchscreens and features. This shift to a subscription model has created a recurring revenue stream and high profit margins. The key was identifying a need, developing a solution, proving its value, then scaling through a tech-enabled product. My next venture will follow a similar strategy of leveraging digital tools to solve challenges and build passive income. — Chase McKee, Founder & CEO, Rocket Alumni Solutions

Offer Personalized Digital Journals with Subscriptions

When I was transitioning to financial independence, I turned my passion for storytelling into a profitable venture. I started by creating a series of themed digital journals designed to help people track their personal goals and creative ideas. Instead of going the usual route, I integrated interactive features that allowed users to customize their journaling experience based on their interests, from travel to fitness.

To monetize these journals, I adopted a subscription model where users paid a small monthly fee for access to new templates and features. I also offered premium packages that included personalized coaching and exclusive content. Continue Reading…

Over the last few years, discussions around personal finance have been louder – and more confusing – than ever.

Market volatility, rising interest rates, the high cost of living and global unrest have dominated headlines and made life increasingly complicated for most Canadians.

Today (October 9) is World Financial Planning Day, a time to dim the noise and focus on the basics: a financial plan, what it is and how it can help you feel financially prepared for your future. More importantly, it’s an occasion to recognize that working with a financial advisor on a personal plan has many benefits, including greater financial confidence and a higher quality of life.

A financial plan is not just an investment plan: in fact, it’s much more. An investment portfolio is certainly a component of a financial plan, but your investments don’t provide a clear direction for any life plans in the coming years. Your investments can indicate financial returns, but their value is not guaranteed at any point in time and investments alone cannot prepare you for the future.

A financial plan is a goals-based document that provides a road map for what you would like to achieve in the short- and long-term. The goals are not necessarily financial, but they need monetary support (like investment income) to be reached.

Goals within your financial plan may include:

When you want to retire, and the lifestyle you want in your golden years.

Affording major expenditures, including a home, vacations or post-secondary education for dependents.

Preparedness for untimely events, such as premature death, disability or critical illness.

Plans for your estate and the legacy you’d like to leave for your family and charities.

These goals are personal and involve answers to questions that address significant, and sometimes difficult, situations. It can be challenging to determine these responses on your own, so working with a financial planner can help you answer these questions, define your goals and create a strategy to achieve them. Your financial planner will get to know you on a personal level. Then, based on your aspirations, project what needs to happen and create a financial plan for your future. Continue Reading…

Cut The Crap Investing recently looked at the go-to chart on creating retirement income. The post looked at sustainable spend rates. The 4% “rule” suggests that you can start at a 4.2% spend rate, and then increase spending each year to adjust for inflation. That protects your spending power and lifestyle in retirement.

That said, the 4% rule is based on a very conservative 50/50 stock to bond allocation using U.S. assets. We might be able to boost the spend rate in retirement by adding more growth and more non-correlated assets.

In the above post and charts we see the challenges of a 5% or 6% spend rate with a traditional balanced portfolio.

Here’s a very good post that shows how we can potentially boost our spend rate. And the go-to table on boosting your retirement start date with gold, REITs, small cap value, and international stocks in the mix. The equity allocation is moved up to 70% as well.

From that post …

So instead of limiting your retirement portfolio to the S&P 500 and government bonds, think about diversifying with small-cap value and gold! If you don’t mind a little more complexity, go a step further with REITs, utilities, and international stocks. This level of diversification has done very well in the past. It includes at least one asset that does well in each type of economic situation.

That post offers a nod to the all-weather portfolio and utilities as a defensive asset. Readers will know I am a favour of both additions, especially the defensive sectors for retirement that includes consumer staples, healthcare and utilities (including pipelines and telco). I’m hopeful that the approach will allow us to boost our spend rate to the 5-6% range.

Canadian banks in 2024

At the beginning of the month we looked at investing in Canadian banks. I noted that it is difficult to pick the winners and there is a surprising variance in returns among the individual banks. Here’s the total returns in 2024. Continue Reading…