Every day, there are many companies experiencing significant price drops. There is a section on Yahoo Finance called “Day Losers” where the biggest losers of the day are highlighted.

Are those good buying opportunities?

Maybe.

All of our favorite Blue Chip stocks have been part of this list. Some of those stocks have recovered, while others continued their downward slide. The truth is that we never know for sure which stock will recover and which one will just disappear. Remember Nortel, Nokia, Kodak, BlackBerry, Blockbuster, RadioShack, Toys R Us? These were stock market leaders that never recovered.

On the other hand, for those investors who have bought the U.S. or Canadian index, they have always seen their money coming back after any major drop.

Instead of discussing the pros and cons of buying any individual stock, I think we should look at the big picture and talk about the difference between buying a basket of individual stocks when they are down versus buying the index.

The main difference between buying any individual stock and buying the index when they both go down is that, up until now, the index has always bounced back, while some of the blue-chip stocks that we have learned to love/trust might never recuperate. Kodak, Blockbuster and Nokia never recuperated. They slowly declined into the graveyard of market history.

Why? Because, unlike individual stocks, the S&P 500 is always changing.

S&P 500 from 1927 to 2023 from 20 to 4,090; a 17,620% gain.

Looking at this graph, you might think that you could have invested $20 in the most popular stocks of 1927 and just waited to get rich. But it doesn’t work out that way. The companies that represented U.S. stocks in 1927 are very different from the companies that represent U.S. stocks in 2023. Most of the original companies composing the S&P 500 no longer exist, but the S&P is still going strong.

Regardless of how quickly companies are moving in and out of the index, you can see that owning an index is fundamentally different from owning a basket of individual stocks. While your basket of individual stocks might remain the same over time, the index will not.

There are many benefits provided to index investors.

We get the highest returns and pay the lowest fees. Hundreds of analysts go on a hunt for the best stocks; they spend their time, money, and energy crunching numbers, buying the stocks that are going up and selling the stocks that are going down, and we get to reap the rewards.

According to the SPIVA Report, the S&P 500 index has outperformed 92% of money manager professional over the past 15 years, and the cost to us is usually 0.05%/year. There is no better deal in town.

Alain Guillot is a part time event photographer, part time Salsa teacher, and part time personal finance blogger. He came to Quebec as an immigrant from Colombia. Due to his mediocre French he was never able to find a suitable job, so he opened a Salsa/Tango dance school and started his entrepreneurship journey. Entrepreneurship got him started into personal finance and eventually into blogging. Now he lives a Lean FIRE lifestyle and shares his thoughts in his blog AlainGuillot.com. This blog originally appeared on his blog on Oct. 9, 2023 and is republished here with permission.

Occasionally, a friend or family member asks for help with their investments. Whether or not I can help depends on many factors, and this article is my attempt to gather my thoughts for the common case where the person asking is dissatisfied with their bank or other seller of expensive mutual funds or segregated funds. I’ve written this as though I’m speaking directly to someone who wants help, and I’ve added some details to an otherwise general discussion for concreteness.

Assessing the situation

I’ve taken a look at your portfolio. You’ve got $600,000 invested, 60% in stocks, and 40% in bonds. You pay $12,000 per year ($1000/month) in fees that were technically disclosed to you in some deliberately confusing documents, but you didn’t know that before I told you. These fees are roughly half for the poor financial advice you’re getting, and half for running the poor mutual funds you own.

It’s pretty easy for a financial advisor to put your savings into some mutual funds, so the $500 per month you’re paying for financial advice should include some advice on life goals, taxes, insurance, and other financial areas, all specific to your particular circumstances. Instead, when you talk to your advisor, he or she focuses on trying to get you to invest more money or tries to talk you out of withdrawing from your investments.

The mutual funds you own are called closet index funds. An index is a list of all stocks or bonds in a given market. An index fund is a fund that owns all the stocks or bonds in that index. The advantage of index funds is that they don’t require any expensive professional management to choose stocks or bonds, so they can charge low fees. Vanguard Canada has index funds that would cost you only $120 per month. Your mutual funds are just pretending to be different from an index fund, but they charge you $500 per month to manage them on top of the other $500 per month for the poor financial advice you’re getting.

Other approaches

Before looking at whether I can help you with your investments, it’s worth looking at other options. There are organizations that take their duty to their clients more seriously than the mutual fund sales team you have now. Continue Reading…

By Erin Allen, CIM, VP Online ETF Distribution, BMO ETFs

(Sponsor Content)

Asset allocation is one of the most critical investment decisions an investor can make. Studies, such as the influential Brinson, Hood and Beebower paper, “Determinants of Portfolio Performance,1” suggest that the long-term strategic asset allocation of a portfolio accounts for over 90% of the variation of its return.

According to the study, the portfolio’s strategic – or target – asset allocation will have a greater impact on its performance than security selection or any short-term active or tactical asset allocation shifts.

The first step when constructing a portfolio is to determine the appropriate asset allocation, based on your risk profile and investment objectives, and then select investments across each asset class.

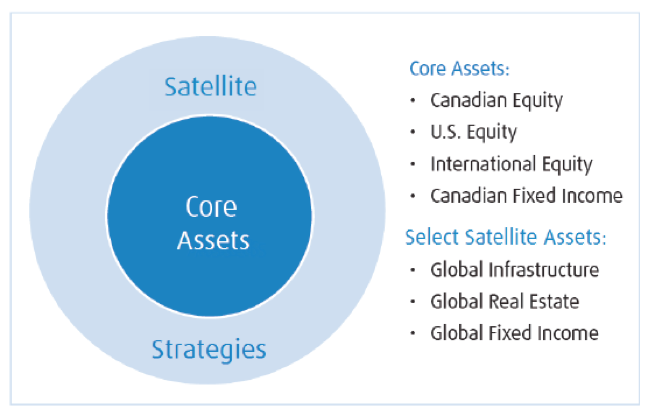

There are several approaches to constructing an investment portfolio. One such strategy is to adopt a core-satellite approach. Core-satellite investing involves using a core portfolio to anchor the portfolio’s strategic asset allocation, and adding satellite investments to enhance returns and/or mitigate risk.

Fundamentals of a core-satellite portfolio

A typical investment portfolio is comprised of traditional asset classes that represent the broad market, and generally include investment-grade fixed income securities and large-cap Canadian, U.S. and international equities, for example BMO S&P TSX Capped Composite Index ETF (ZCN), BMO S&P 500 Index ETF (ZSP), and BMO MSCI EAFE Index ETF (ZEA). These asset classes make up the portfolio’s “core” investments. Specific securities within each asset class will depend on the investor’s return objectives and risk tolerance.

In order to further diversify the portfolio, non-traditional asset classes – referred to as “satellite” strategies – are used to enhance returns and manage risk. Satellite strategies often have greater return potential than core asset classes, but may be considered higher risk (with greater volatility) when held on their own. However, they often have a lower correlation – a measure of the degree to which two investments move in relation to each other – to traditional assets classes. Satellite strategies can include asset classes or themes that can be used as either short-term, tactical investments, or held for longer periods of time. Combining investments with a low correlation can improve the risk/return characteristics of a portfolio.

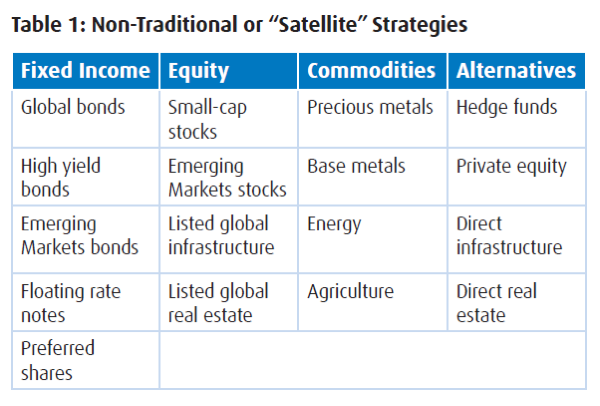

Examples of satellite strategies are shown in Table 1 [below]. By using one or more of these satellite strategies in tandem with a core portfolio, investors can further diversify their portfolio across additional asset classes, regions, sectors, market capitalizations, currencies and/or investment styles. For example, real assets such as commodities, infrastructure and real estate have a tangible value that can rise during periods of inflation.

Infrastructure and real estate can also offer a steady and predictable cash flow. Global fixed income securities provide Canadian investors with exposure to bonds in countries with different currencies and interest rate cycles, which can help reduce interest rate risk; while hedge funds, such as market neutral or multi-strategy funds, can actually lower volatility and improve a portfolio’s risk-adjusted performance.

Table 1: Courtesy BMO ETFs

Constructing a core-satellite portfolio

A core-satellite portfolio can be implemented by using:

Active strategies that seek to add value through security selection;

Passive strategies that seek to track the performance of an index representing a particular investment market;

A combination of active and passive strategies.

There is a fundamental investment theory that states markets are efficient and the price of any individual security already reflects all available relevant information, which makes it more difficult for active managers to outperform. Investors who share this view would generally purchase passive investments. Conversely, others believe markets are not efficient and do not always behave rationally, providing active managers with the opportunity to select undervalued securities and avoid overvalued securities – and increasing their potential to add value above the market and/or provide better risk controls and downside protection. While some studies show that the “average” active manager does not add value, well-selected managers have demonstrated the ability to add value and/or reduce risk over the long term.

One approach to constructing a core-satellite portfolio is to use passive investments for efficient markets and active investments for less efficient markets. Many traditional asset classes, such as the U.S. equity market, are considered to be very efficient, making it difficult for active managers to outperform. Non-traditional asset classes, such as Emerging Markets equities or high yield bonds, are often considered less efficient. Many of these asset classes may be more difficult to access, can be less liquid, and are not covered as broadly by research analysts, which can enable active managers greater potential to add value.

The most critical step

Determining the appropriate asset allocation (mix of stocks, bonds and other asset classes) is the most important step when building your portfolio. Whether you use a passive strategy, an active strategy, or a combination of both, the addition of one, or more, satellite strategies to a core portfolio can potentially enhance returns, reduce risk and provide a better return/risk profile for your portfolio.

Simple to use All-in-One Core Portfolio ETFs

BMO ETFs offers a range of all-in-one Asset Allocation ETFs you can select as your core investment portfolio, based on your risk tolerance and time horizon. These ETFs are a one-ticket solution where the asset allocation is determined by professional managers, and where the asset allocation is automatically rebalanced for you on a regular basis to ensure you are on track to meeting your goals. They are low cost, and there is no double dipping on the fees (all-in MER of 0.20%* includes the cost of the underlying ETFs). Examples include our BMO Balanced ETF (ZBAL), or BMO Growth ETF (ZGRO) and BMO All-Equity ETF (ZEQT). Click Here to learn more.

Erin Allen has been a part of the BMO ETFs team driving growth since the beginning, joining BMO Global Asset Management in 2010 and working her way through a variety of roles gaining experience in both sales and product development. For the past 5+ years, Ms. Allen has been working closely with capital markets desks, index providers, and portfolio managers to bring new ETFs to market. More recently, she is committed to helping empower investors to feel confident in their investment choices through ETF education. Ms. Allen hosts the weekly ETF Market Insights broadcast, delivering ETF education to DIY investors in a clear and concise manner. She has an honors degree from Laurier University and a CIM designation.

* Management Expense Ratios (MERs) are the audited MERs as of the fund’s fiscal year end or an estimate if the fund is less than one year old since the audited MER of the ETF has not gone through a financial reporting period.

Any statement that necessarily depends on future events may be a forward-looking statement. Forward-looking statements are not guarantees of performance. They involve risks, uncertainties and assumptions. Although such statements are based on assumptions that are believed to be reasonable, there can be no assurance that actual results will not differ materially from expectations. Investors are cautioned not to rely unduly on any forward-looking statements. In connection with any forward-looking statements, investors should carefully consider the areas of risk described in the most recent simplified prospectus.

Commissions, management fees and expenses (if applicable) may be associated with investments in mutual funds and exchange traded funds (ETFs). Trailing commissions may be associated with investments in mutual funds. Please read the fund facts, ETF Facts or prospectus of the relevant mutual fund or ETF before investing. Mutual funds and ETFs are not guaranteed, their values change frequently and past performance may not be repeated.

For a summary of the risks of an investment in BMO Mutual Funds or BMO ETFs, please see the specific risks set out in the prospectus of the relevant mutual fund or ETF . BMO ETFs trade like stocks, fluctuate in market value and may trade at a discount to their net asset value, which may increase the risk of loss. Distributions are not guaranteed and are subject to change and/or elimination.

S&P®, S&P/TSX Capped Composite®, S&P 500® are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”) and “TSX” is a trademark of TSX Inc. These trademarks have been licensed for use by S&P Dow Jones Indices LLC and sublicensed to BMO Asset Management Inc. in connection with the above mentioned BMO ETFs. These BMO ETFs are not sponsored, endorsed, sold or promoted by S&P Dow Jones LLC, S&P, TSX, or their respective affiliates and S&P Dow Jones Indices LLC, S&P, TSX and their affiliates make no representation regarding the advisability of trading or investing in such BMO ETF(s).The BMO ETFs or securities referred to herein are not sponsored, endorsed or promoted by MSCI Inc. (“MSCI”), and MSCI bears no liability with respect to any such BMO ETFs or securities or any index on which such BMO ETFs or securities are based. The prospectus of the BMO ETFs contains a more detailed description of the limited relationship MSCI has with BMO Asset Management Inc. and any related BMO ETFs.

BMO Mutual Funds are offered by BMO Investments Inc., a financial services firm and separate entity from Bank of Montreal. BMO ETFs are managed and administered by BMO Asset Management Inc., an investment fund manager and portfolio manager and separate legal entity from Bank of Montreal.

BMO Global Asset Management is a brand name under which BMO Asset Management Inc. and BMO Investments Inc. operate.

®/™Registered trademarks/trademark of Bank of Montreal, used under licence.

Regular blog readers know that I’m a big proponent of passive investing with low cost, globally diversified index funds and ETFs. Why? Low fees are the best predictor of future returns. Global diversification reduces the risk within your portfolio. Index funds and ETFs allow investors to hold thousands of securities for a very small fee.

Investors who eventually come to understand these three principles want to know how to build their own index portfolio. There are several ways to do this: pick your own ETFs through a discount broker, invest with a robo-advisor, or buy your bank’s index mutual funds.

Still, the amount of information can be overwhelming. There are more than 1,000 ETFs, thousands of mutual funds, a dozen or more discount brokerage platforms, and nearly as many robo advisors. The choices are enough to make your head spin.

Now, I’ll explain exactly how I invest my own money so you can see that I practice what I preach.

My Investing Journey

I started investing when I was 19, putting $25 a month into a mutual fund. When I began my career in hospitality, I contributed to a group RRSP with an employer match. The catch was that the investments were held at HSBC and invested in expensive mutual funds.

When I left the industry I transferred my money (about $25,000) to TD’s discount brokerage platform. That’s when I started investing in Canadian dividend-paying stocks. I followed the dividend approach after reading Norm Rothery’s “best dividend stocks” in Canada articles in MoneySense.

I later found dividend growth stock guru Tom Connolly (plus a devoted community of dividend investing bloggers) and started paying more attention to stocks with a long history of paying and growing their dividends.

Five years later I had built up a $100,000 portfolio with 24 Canadian dividend stocks. My performance as a DIY stock picker was quite good. I had outperformed both the TSX and my dividend stock benchmark (iShares’ CDZ) from 2009 – 2014. My annual rate of return since 2009 was 14.79%, compared to 13.41% for CDZ and 7.88% for XIU (Canadian index benchmark).

But something wasn’t quite right. I started obsessing over oil & gas stocks that had recently tanked. I had a difficult time coming up with new dividend stocks to buy. I read more and more opposing views to my dividend growth strategy and realized I was limiting myself to a small subset of stocks in a country that represents just 3-4% of the global stock market.

Furthermore, new products were coming down the pike – including the introduction of Vanguard’s All World ex Canada ETF (VXC). Now I could buy a tiny piece of thousands of companies from around the world with just one product.

So, in early 2015 I sold all of my dividend stocks and built my new two-ETF solution (VCN and VXC). I called it my four-minute portfolio because it literally took me four minutes a year to monitor and add new money. No more obsessing over which stocks to buy or worrying if a stock was going to go to zero.

Fast-forward to 2019 and another product revolution made my portfolio even simpler. Vanguard introduced its suite of asset allocation ETFs, including VEQT – my new one-ticket investing solution.

The next change to my investment portfolio was in January 2020 when I moved my RRSP and TFSA from TD Direct Investing over to Wealthsimple Trade to take advantage of zero-commission trading. Continue Reading…

Image courtesy MoneySense.ca/Unsplash: Photo by Ruben Sukatendel

My latest MoneySense Retired Money column looks at a trendy new investing approach known as “Direct Indexing.” You can find the full column by clicking on the highlighted headline: What is direct indexing? Should you build your own index?

Here’s a definition from Investopedia : “Direct indexing is an approach to index investing that involves buying the individual stocks that make up an index, in the same weights as the index.”

When I first read about this, I thought this was some version of the common practice by Do-it-yourself investors who “skim” the major holdings of major indexes or ETFs, thereby avoiding any management fees associated with the ETFs. It is and it isn’t, and we explore this below.

Investopedia notes that in the past, buying all the stocks needed to replicate an index, especially large ones like the S&P 500, required hundreds of transactions: building an index one stock at a time is time-consuming and expensive if you’re paying full pop on trading commissions. However, zero-commission stock trading largely gets around this constraint, democratizing what was once the preserve of wealthy investors. According to this article that ran in the summer at Charles River [a State Street company], direct indexing has taken off in the US: “ While direct index portfolios have been available for over 20 years, continued advancement of technology and structural industry changes have eliminated barriers to adoption, reduced cost, and created an environment conducive for the broader adoption of these types of strategies.”

These forces also means direct indexing can be attractive in Canada as well, it says. However, an October 2022 article in Canadian trade newspaper Investment Executive suggests “not everyone thinks it will take root in Canada.” It cast direct indexing as an alternative to owning ETFs or mutual funds, noting that players include Boston-based Fidelity Investments Inc, BlackRock Inc., Vanguard Group Inc., Charles Schwab and finance giants Goldman Sachs Inc. and Morgan Stanley.

An article at Morningstar Canada suggested direct indexing is “effectively … the updated version of separately managed accounts (SMA). As with direct indexing, SMAs were modified versions of mutual funds, except the funds were active rather than passive with SMAs.”

My MoneySense column quotes Wealth manager Matthew Ardrey, a vice president with Toronto-based TriDelta Financial, who is skeptical about the benefits of direct indexing: “While I always think it is good for an investor to be able to lower fees and increase flexibility in their portfolio management, I question just who this strategy is right for.” First, Ardrey addresses the fees issue: “Using the S&P500 as an example, an investor must track and trade 500 stocks to replicate this index. Though they could tax-loss-sell and otherwise tilt their allocation as they see fit, the cost of managing 500 stocks is very high: not necessarily in dollars, but in time.” It would be onerous to make 500 trades alone, especially if fractional shares are involved.

Ardrey concludes Direct indexing may be more useful for those trying to allocate to a particular sector of the market (like Canadian financials), where “a person would have to buy a lot less companies and make the trading worthwhile.”

A hybrid strategy used by DIY financial bloggers may be more doable

I would call this professional or advisor-mediated Direct Indexing and agree it seems to have severe drawbacks. However, that doesn’t mean savvy investors can’t implement their own custom approach to incorporate some of these ideas. Classic Direct Indexing seems similar but slightly different than a hybrid strategy many DIY Canadian financial bloggers have been using in recent years. They may target a particular stock index – like the S&P500 or TSX – and buy most of the underlying stocks in similar proportions. Again, the rise of zero-commission investing and fractional share ownership has made this practical for ordinary retail investors. Continue Reading…

Alain Guillot is a part time event photographer, part time Salsa teacher, and part time personal finance blogger. He came to Quebec as an immigrant from Colombia. Due to his mediocre French he was never able to find a suitable job, so he opened a Salsa/Tango dance school and started his entrepreneurship journey. Entrepreneurship got him started into personal finance and eventually into blogging. Now he lives a Lean FIRE lifestyle and shares his thoughts in his blog AlainGuillot.com. This blog originally appeared on his blog on Oct. 9, 2023 and is republished here with permission.

Alain Guillot is a part time event photographer, part time Salsa teacher, and part time personal finance blogger. He came to Quebec as an immigrant from Colombia. Due to his mediocre French he was never able to find a suitable job, so he opened a Salsa/Tango dance school and started his entrepreneurship journey. Entrepreneurship got him started into personal finance and eventually into blogging. Now he lives a Lean FIRE lifestyle and shares his thoughts in his blog AlainGuillot.com. This blog originally appeared on his blog on Oct. 9, 2023 and is republished here with permission.