When I’m asked for investment advice and I say “nobody knows what will happen to an individual stock,” I almost always get nodding agreement, but these same people then act as if they know what will happen to their favourite stock.

In a recent case, I was asked for advice a year ago by an employee with stock options. At the time I asked if the current value of the options was a lot of money to this person, and if so, I suggested selling some and diversifying. He clearly didn’t want to sell, and he decided that the total amount at stake wasn’t really that much. But what he was really doing was acting as though he had useful insight into the future of his employer’s stock.

He proceeded to ask others for advice, clearly looking for a different answer from mine. By continuing to ask others what they thought about the future of his employer’s stock, he was again contradicting his claimed agreement with “nobody knows what will happen to an individual stock.”

How a seemingly token amount can become a painful loss

Fast-forward a year, and those same options are now worth about 15 times less. Suddenly, that amount that wasn’t that big a deal has become a very painful loss. He has now taken advantage of a choice his employer offers to receive fewer stock options in return for slightly higher pay. It’s hard to be sure without seeing the numbers, but in arrangements I’ve seen with other employers, a better strategy is to take the options and just sell them at the first opportunity if the stock is far enough above the strike price. Again, he’s acting as though he has useful insight into the future of his employer’s stock.

The lesson from this episode isn’t that people should listen to me. I’m used to people asking me for advice and then having my unwelcome advice ignored. What I find interesting is that even if I can get someone to say out loud “I don’t know what’s going to happen to any individual stock,” they can’t help but act as though either they know themselves, or they can find someone who does know.

Michael J. Wiener runs the web site Michael James on Money, where he looks for the right answers to personal finance and investing questions. He’s retired from work as a “math guy in high tech” and has been running his website since 2007. He’s a former mutual fund investor, former stock picker, now index investor. This blog originally appeared on his site on Sept. 20, 2022 and is republished on the Hub with his permission.

Is it just me, or do investors have a knack for overcomplicating things?

Take the argument about active versus passive investing. We’ve known for more than 30 years that, after costs, the return on the average passively managed dollar must beat the return on the average actively managed dollar. Nobel laureate William Sharpe demonstrated this for us in his 1991 article, “The Arithmetic of Active Management,” and nothing has changed since then.

Despite that scary word, “arithmetic,” you don’t need to be a math major to accept Sharpe’s conclusions and invest accordingly. Still, you may want to see for yourself what he’s talking about. In the first episode of our Index and Chill video/blog series, we’ll show you why active investors (as a group) are destined to underperform passive investors.

Dividing and Conquering the Canadian Stock Market

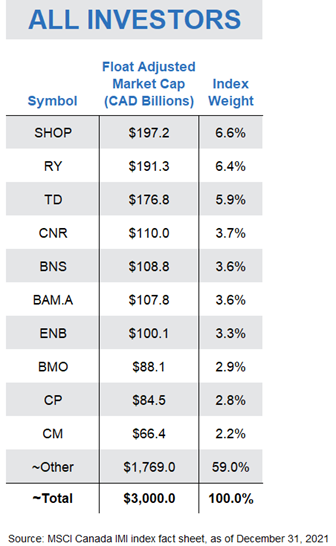

To demonstrate how Sharpe’s theory plays out in action, let’s illustrate his work using the Canadian stock market as our example. The Canadian stock market is made up of hundreds of companies, with a total value of around 3 trillion dollars. If we sort these 300 or so companies from largest to smallest based on the value of their shares available to regular investors, we find familiar names at the top of our list, including Shopify, Enbridge, and the Big Five banks.

Dividing each company’s value by the total value of the Canadian stock market provides us with a percentage weight for each, otherwise known as its “index weight.” For example, at the end of 2021, Shopify had the largest index weight, at around 6.6%, followed by RBC and TD, which made up 6.4% and 5.9% of the Canadian stock market, respectively. These weights guide index fund managers on how much to allocate to each company in their funds.

So, here’s where Sharpe’s work applies: At any point in time, investors as a group must hold all available shares of these companies. So, it stands to reason that, as a group, investors also collectively receive the total return of the Canadian stock market. In other words, if the Canadian stock market returns 10% this year, or around 300 billion dollars, everyone invested in the market will receive 300 billion dollars to divvy up amongst themselves.

Zero-Sum Games

Of course, some market participants will receive a higher return. But for each winner, there must be one or more losers.

This is the concept behind zero-sum game theory. The holdings of all investors in a particular market combine to form that market. So, if one investor’s dollars outperform the market over a particular period, another investor’s dollars must underperform, ensuring that the dollar-weighted return of all investors equals the return of the market.

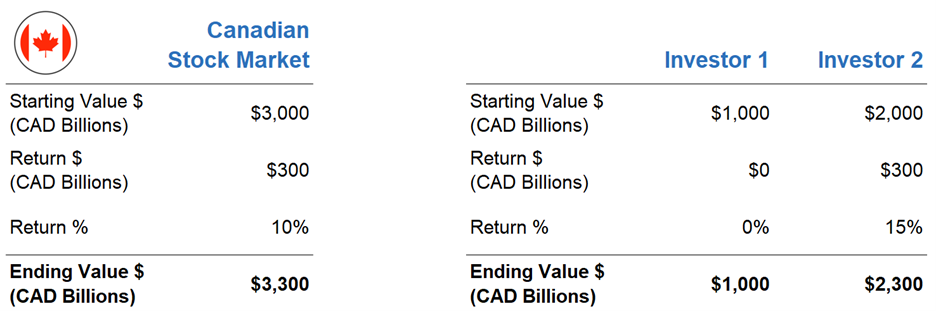

Let’s use a super-simplified example to illustrate this point. Sticking with our $3 trillion-dollar Canadian stock market, let’s assume there are only two investors in the entire market. Investor 1’s portfolio is worth 1 trillion dollars and Investor 2’s portfolio is worth 2 trillion dollars. Combined, they are the Canadian stock market.

Of course, Investor 1 and Investor 2 wouldn’t be much fun if they didn’t have different opinions about which stocks were going to outperform over the next year. Based on their preferences, they trade with each other until they are both relatively happy with their portfolio.

Over the next year, let’s say the Canadian stock market returns 10%, providing a total dollar return of 300 billion to our two investors. But Investor 1’s stock picks end up returning 0%, while Investor 2’s portfolio earns an impressive 15%, or 300 billion dollars. Investor 2 was able to earn an additional 100 billion dollars by “winning” this amount from unlucky Investor 1. But again, as a group, there was no way the pair could earn more than 300 billion dollars. In a zero-sum game, the winner’s gain comes at the expense of the loser’s loss, with zero “extra” money floating around unaccounted for.

Setting the Stage: Active vs. Passive Participation

Now, let’s look at how this zero-sum game stuff applies to active versus passive investing.

To illustrate, we’ll return to our $3 trillion Canadian stock market, and each company’s weighting within the total market.

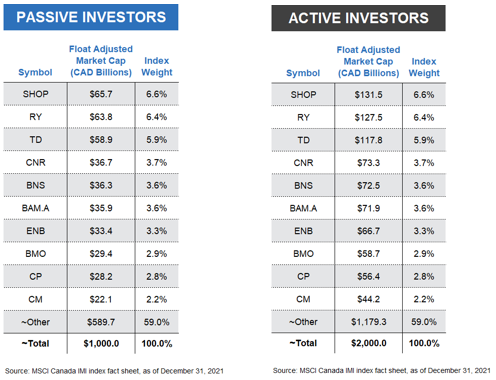

But instead of imagining Canada’s total market is divided between two active investors, let’s establish a slightly more realistic model. We’ll assume passive investors as a group hold one-third, or $1 trillion of all Canadian company shares, and active investors as a group hold the remaining two-thirds, or $2 trillion. We’ll once again assume the overall Canadian stock market returns 10% this year, but with one critical caveat. That 10% is before costs. As we know, extra investment costs can add up quickly from management fees, bid-ask spreads, commissions, and other tricks of the trade.

I want to also point out that the particular split between passive vs. active makes no difference to our exercise. Since these passive and active investors as a group are the total Canadian stock market, and since the passive group’s holdings have the same percentage weights as the overall market, the active group’s holdings must also have the exact same percentage weights. In other words, however you slice it up, the pie is the pie, with the same ratio of ingredients in the mix.

Passive Pursuits

Let’s now look at how our passive investors would have fared with their $1 trillion market share. With these assumptions, if the market returned 10%, the passive investor group would be expected to earn $100 billion, before costs.

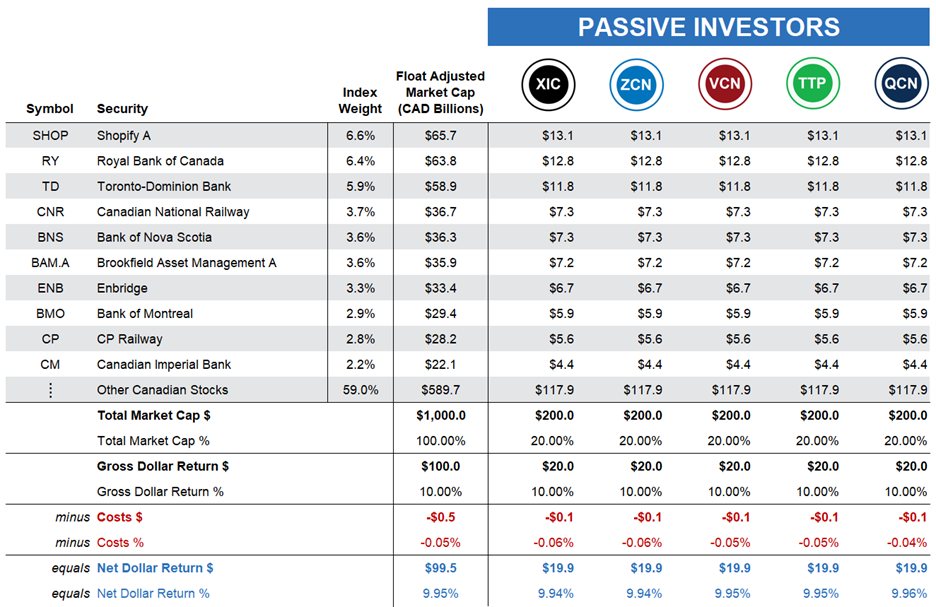

Now, suppose you are one of five passive investors in the Canadian market, with about $200 billion to invest — or one-fifth of the passive investors’ $1 trillion market share.

You don’t have a fancy business degree, and you’ve never even glanced at a company’s financial statements. You’d rather just buy and hold a low-cost index fund or ETF that tracks the broad Canadian stock market, so you invest your $200 billion in the iShares Core S&P/TSX Capped Composite Index ETF (XIC). XIC’s fund managers would use your money to purchase hundreds of Canadian stocks on your behalf, each according to its weight in the index. For example, they would purchase $12.8 billion of Royal Bank stock, or 6.4% of your $200 billion … and so on.

A year goes by, and in our illustration, you receive the stock market return of 10%, before costs. That’s $20 billion on your $200 billion investment. And because passive investing costs are low, your after-fee return will be around 9.94%, or just slightly less than the market return.

Your four fellow passive investors choose comparable broad-market Canadian equity ETFs that deliver similar after-cost returns. So, on average, the passive group earns around 9.95% after costs.

Active Adventures

Next, let’s turn to our active investors, who continue to hope or believe they can beat the market, even after costs. We’ll again assume there are only five investors in our active management group, and they all have the same $400 billion each to invest.

However, unlike our passive camp, our active investors do not all share a similar approach to investing; each will pursue a different tactic.

Our first active investor selects a portfolio of funds recommended by their favorite banker who is a so-called “closet indexer.” This banker is afraid of losing their job if their recommendations stray too far from the popular benchmarks, so their preferred funds closely follow a passive approach … but with a catch. Their fund management fees are a hefty 2.5%. As a result, our closet indexer earns the market return of 10% before fees, but their net, after-cost return shrinks to 7.5%. Continue Reading…

By now, you will have almost certainly heard a few stories about the folly of stock picking as a viable way to beat the market. The problem that high net worth (HNW) investors are disproportionately saddled with is they are bombarded with people who purport to be able to add value by doing things that, in aggregate, cannot possibly be true.

There are three basic equity building blocks investors might use to mix and match in their portfolio construction: individual securities, ETFs and / or mutual funds. Very few HNW investors use funds, but I will mention them for the sake of completeness and comparison. Mostly, funds are used as an example of what NOT to do.

To provide structure and consistency to this discussion, I should add there are a couple industry terms you might be somewhat familiar with that nonetheless need to be defined. They are:

Alpha – The pursuit of reliable, consistent and superior risk-adjusted returns; and:

Closet Indexing – The practice of masquerading as an active manager while holding a portfolio basket that nearly replicates the index it tracks.

No matter what vehicles are used, these two concepts need to be considered when assessing options.

Dreams versus Reality

There’s a simple way to think of them. They are, respectively, the dream and the reality of how most traditional mutual funds are managed.

Everyone wants Alpha at a micro (personal) level, but Alpha does not even exist on a macro (aggregate) level. A metaphor many use is that no matter how high anyone’s mark is, if everyone else in the class has a high mark, the class will have a high average, but it will be difficult to beat the average. This was simply explained by a Nobel prize winner named William F. Sharpe of Stanford, who wrote a paper about 30 years ago called “The Arithmetic of Active Management.”

In it, he showed the self-evident logic that any market is made up of active managers (traders) and passive managers (benchmark replicators). Any benchmark (such as the TSX) is merely the sum of all active and passive participants. Seeing as the passive people merely replicate the benchmark, their returns will equal the return of the benchmark minus their fees. It follows that the average return of all active managers will also equal the total benchmark minus fees. Since average active fees exceed average passive fees, it logically follows that the average passively managed dollar must outperform the average actively managed dollar. Continue Reading…

Many people advocate having a portfolio made up of mostly a core of low cost index funds along with a small “explore” part for taking concentrated risks on favourite investments. This can work well enough if you’re realistic about it, but most investors cross the line to self-delusion.

Ben Carlson does a good job justifying the existence of explore-type investments in his article The Case for Having a Fun Portfolio. After all, people are entitled to spend their money however they want. Not every expenditure has to be part of a logical long-term plan. We can buy a beer, or a motorcycle, or some favourite stock if we want. So what if the long-term expectation is that the explore part of people’s portfolios will underperform indexes.

All the logic makes sense up to this point. But just about every stock-picker I know can’t resist taking this a step further. “Besides, the stock I picked is going to do great.” In their hearts, they know their stock picks are going to outperform. Past results don’t seem to deter them. They wouldn’t bother with the explore part of their portfolios if they truly believed they would lose money over a lifetime of picking stocks.

All the evidence says that professional investors today set good relative prices so that individual investors who choose their own stocks are essentially making random picks. The odds are against the small guy, but hope springs eternal. I prefer to find hope in other pursuits.

Michael J. Wiener runs the web site Michael James on Money, where he looks for the right answers to personal finance and investing questions. He’s retired from work as a “math guy in high tech” and has been running his website since 2007. He’s a former mutual fund investor, former stock picker, now index investor. This blog originally appeared on his site on April 26, 2021 and is republished on the Hub with his permission.

A few readers have expressed concern about their recent investment performance. In most cases, these investors are holding a sensible, low cost, globally diversified portfolio of index funds ranging from conservative (40% stocks, 60% bonds) to balanced (60% stocks, 40% bonds). One reader said:

“Psychologically, it’s tough to put money in when returns have been so low.”

When you invest in a passive portfolio that tracks broad market indexes you can expect to earn market returns minus a small fee. This is far and away the best and most reliable way to invest for the long term.

But sometimes market returns can be disappointing in the short term. Investors might be experiencing that right now. In fact, if you’ve recently moved away from actively managed funds or stock picking to embrace a portfolio of passive index funds, you might be wondering if that was a wise decision.

Market returns have been dismal this year compared to returns from the previous two years. But context matters. FP Canada’s projection and assumption guidelines suggest future expected returns of approximately 4.78% per year for a global balanced portfolio.

Meanwhile, an actual global balanced portfolio represented by Vanguard’s VBAL and iShares’ XBAL returned about 15% in 2019 and 10.5% in 2020. Even a global conservative (40/60) portfolio returned about 12% in 2019 and 10% in 2020. This is highly unusual.

ETF Name

Ticker

YTD

2020

2019

Vanguard Conservative ETF

VCNS

-0.82%

9.41%

12.10%

iShares Core Conservative ETF

XCNS

-0.86%

10.33%

n/a

Vanguard Balanced ETF

VBAL

1.12%

10.24%

14.91%

iShares Core Balanced ETF

XBAL

1.41%

10.58%

15.19%

Vanguard Growth ETF

VGRO

3.11%

10.89%

17.84%

iShares Core Growth ETF

XGRO

3.01%

11.42%

17.96%

Vanguard Equity ETF

VEQT

5.56%

11.29%

n/a

iShares Core Equity ETF

XEQT

4.76%

11.71%

n/a

A reasonable investor adjusts his or her expectations of future returns. After all, a conservative or balanced portfolio certainly won’t continue to deliver double-digit annual returns forever.

Indeed, reasonable investors should accept market returns and not fuss over short-term fluctuations or periods of underperformance. Continue Reading…

Michael J. Wiener runs the web site Michael James on Money, where he looks for the right answers to personal finance and investing questions. He’s retired from work as a “math guy in high tech” and has been running his website since 2007. He’s a former mutual fund investor, former stock picker, now index investor. This blog originally appeared on his site on Sept. 20, 2022 and is republished on the Hub with his permission.

Michael J. Wiener runs the web site Michael James on Money, where he looks for the right answers to personal finance and investing questions. He’s retired from work as a “math guy in high tech” and has been running his website since 2007. He’s a former mutual fund investor, former stock picker, now index investor. This blog originally appeared on his site on Sept. 20, 2022 and is republished on the Hub with his permission.