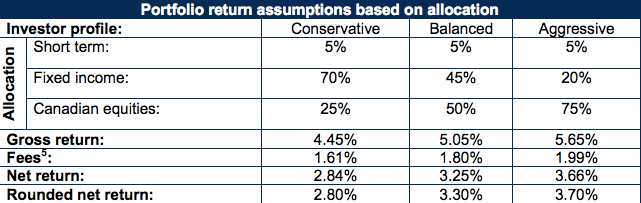

Here at the Hub we like to present all points of view. On Tuesday, we ran a guest blog by author and chartered accountant David Trahair about the new second edition of his book, Enough Bull, which explained why he is 100% in fixed-income vehicles like GICs. Today, we do the same thing with a guest blog by Scotia McLeod’s Robert S. Cable, who argues almost the polar opposite in his new book, Inevitable Wealth. We’ll review both books formally in the coming weeks. Meanwhile, over to Bob! – – JC

Stocks beat bonds, hands down

By Robert S. Cable

Special to the Financial Independence Hub

All of the research I’ve carried out since I began doing this in 1980 and every piece of research I’ve seen comparing stocks to bonds– every single time comes to the same conclusion — that is that stock returns don’t just beat the returns of bonds, stocks clobber bonds. It’s absolutely no contest.

In my book, Inevitable Wealth, I compare 40 years of returns, from 1975 through 2014. I show $100,000 invested in Government of Canada five-year bonds, with money reinvested every five years, to the same $100,000 invested in stocks by way of the TSX Composite Index.

In 1975, those bonds yielded 7.25% so your annual income started out at $7,250. Stocks paid somewhat less, $5,360. Advantage bonds—initially. However just four years later, the dividends paid on stocks had moved higher to the point where the dividends paid on stocks was greater than the bond’s income.

But check out these numbers. In 2014, your bonds paid an annual income of just $2,770, down from $7,250, 40 years earlier. Talk about taking a pay cut! Meanwhile in 2014, stocks paid dividends of $49,560. Your stock income was more than 17 times what bonds paid.

What’s really interesting though is this: while stocks paid a much superior and growing income, they really aren’t income investments. The dividend income paid is simply a by-product of these companies sharing their profits with shareholders.

But as they say, that’s only half the story. We’ve looked at the income stocks and bonds produced. But what about the value of each of these investments over those 40 years?

Stocks beat bonds by 17 to 1 over 40 years

Well, that $100,000 you invested in bonds back in 1975 is still worth right around the same $100,000. If you took inflation into account, your $100,000 would actually be worth more like $15,000. The $100,000 invested in stocks? Well, not including the dividends, at the end of 2014 your stocks would be worth a bit more, $1,732,060. Continue Reading…