On Friday, the Hub republished the first part of a two-part Question-and-Answer session between finance professor and author Dr. Moshe Milevsky and Gordon Wiebe of The Capital Partner [TCP]. This is the second and final instalment:

TCP: I wanted to turn to your Book, Longevity Insurance for a Biological Age. Your thesis is that we should be looking at our biological age and using that to calculate and project our income and how much we should be drawing from our savings.

M.M. And, more importantly than that, making decisions in our personal finances, right?

You know, somebody is trying to figure out at what age they should take C.P.P. Should I take it at 60? 65? 70?I don’t think they should use their chronological age to do that.

Trying to figure out when to retire? Stop using your chronological age.

I mean there’s a whole host of decisions that you have to make based on age and I’m saying we’re using the wrong age metric. It should be based on your biological age.

Now, at this point, biological age sounds like this funny number that comes out of some website, but sooner or later we’ll all have it. And, it’s going to be faster than you think. Your watch will tell you your biological age. And, then in a couple of years, people will stop associating themselves with their chronological age.

They will just stop using it.

And you’re going to sit down with your antiquated compliance driven forms that say, “I need to know my client’s age. Oh, you’re 62.”

And, the client says, “Ha, ha. That’s chronological age. We don’t use that anymore, buddy. I use biological age. Sixty-two, that’s not my age.”

It’s about preparing people for the world in which age is not the number of times we circle the sun.

TCP: What metrics do you think we’ll lean towards to measure biological age? Telemeres? Others?

M.M. There’s a whole bunch of bio-markers that can be used. Some people use telomeres or something called “DNA methylation” or epigenetic clocks. There are about fifty of them, but eventually they’ll all coalesce into a number called “biological age.”

There will be a consensus on how to measure it and you’ll go to your doctor and your doctor will say, “your chronological age is 50, but your biological age is 62.” You’re doing something wrong.

Then a financial advisor will use that information differently when you build a retirement plan.

TCP: That makes sense, but trying to achieve a consensus and getting everyone to use the same metrics from a compliance standpoint or trying to get pension plans and policy makers to agree would be a challenge, wouldn’t it?

MM: It would be. In fact, that’s exactly where I’m headed now. I’m giving a speech in Madrid and that’s exactly what regulators from a number of different countries want me to talk about.

They want to know, “is this feasible? We want to implement this in our pension system. We don’t want wealthy people retiring at the age of 65, they’re going to live forever and bankrupt our system. We want people to retire at a biological age.”

TCP: Let’s talk about that a little more. Advisors typically use a 4% draw on savings as a benchmark withdrawal rate. But, if we use our biological age, there would then be a range. I assume somewhere between 3-6%?

Adjusting the 4% Rule

M.M. You’re absolutely right. That’s where I would go with this. You have to use your biological age and the 4% rule has to be adjusted.

But, what I’m saying is more than that. That rule has to change. It’s not just about the number or percentage. It’s how the rule is applied.

I really don’t like the idea of fixing a spending rate today and sticking to it for the rest of your life no matter what happens. Your spending rate has to be adaptable.

What you have to tell people is, “look, this year we can pull out 6.2%. Next year, it really depends on how markets behave. If markets go down, we may have to cut back. If markets go up, we can give you a bit more.”

I think the 4 per cent rule is really what I call a one-dimensional rule. It’s not that four is one dimensional. Any one number is one dimensional: just telling them a per cent.

It’s got to be at least two dimensional. Meaning, this is what it is now, but next year if this is what happens we’ll do that. ..

Three dimensional is to go beyond that is to go beyond that and say let’s take a look at what other income and assets you have.

“Oh! You’ve got a lot more income from guaranteed sources, you can afford more than four per cent, this year.”

TCP: It’s a dynamic scenario, a moving target.

M.M. That’s the key word, dynamic versus static.

The threat of rising Interest Rates

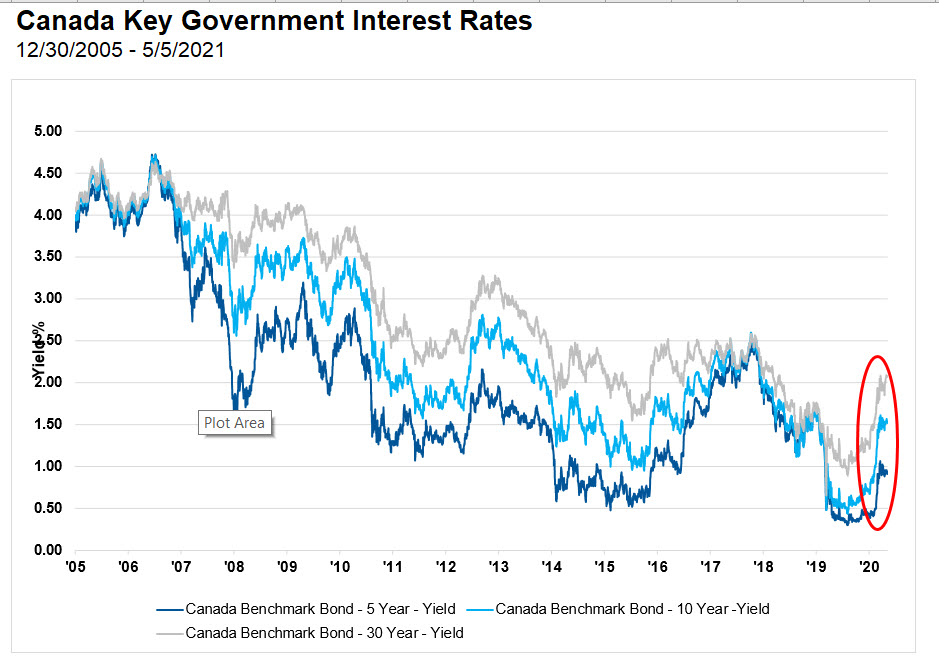

TCP: Canadian investors currently have over two trillion invested in mutual funds. Over half is invested in balanced funds or fixed income and we’re in a horrible position where fixed income is concerned. We’ve had declining rates for the past forty years. At best, bonds will stay flat. At worst, bonds could lose up to thirty per cent of their value.

You talk about the importance of the sequence of returns and how that affects income potential. Have you or your students run scenarios with higher interest rates and the impact it could possibly have?

M.M. I haven’t thought about it beyond what you’re noting. The obvious scenario is as interest rates move up, these things are going to take a big hit.

And, retirees who feel they’ve been playing it safe by putting funds in bonds will suddenly realize there’s nothing safe about bonds in a rising interest rate environment.

I think they’re confusing liquidity and safety with interest rate risk. It’s liquid and its safe. Government is not going to default but boy, can it lose its value.

We’ve become accustomed to this declining pattern. Anybody who is younger than forty doesn’t even understand what higher interest rates means. It’s never happened in their lifetime. They don’t believe it. Understand it. Never felt it. You show them graphs going back to the 1970s. That’s not how to convince them. They’re empiricists. They’ve never lived it themselves, they don’t believe you. Continue Reading…