The transformation of Federal Reserve (Fed) policy continues. What was viewed as a hawkish Federal Open Market Committee (FOMC) outcome at the December meeting has now morphed into a more dovish outlook. In fact, one could conclude the Fed is leaving March by “going out like a lamb.”

So far in 2019, Fed policy decisions have graduated to be less about an actual rate move to the question of what the blue dots are saying instead. Remember, these blue dots represent the policy makers’ own projections for the future Federal Funds Target Rate over a period of time. So, not moving the rate at an official FOMC meeting during the first half of this year is not necessarily of paramount importance, nor expected, for that matter. Instead, it has become all about their policy statement and Fed Funds forecasts.

With that in mind, the results of the March FOMC gathering were being anxiously awaited. Interestingly, fixed-income investors had become accustomed throughout 2017 and 2018 to the Fed essentially guiding the markets as to when a potential rate hike would be coming. While Fed-speak had led to expectations for no action at this latest policy gathering (the actual result on the Fed Funds Rates front), the uncertainty quotient was dialed up because investors were not as certain about the Fed’s blue dot path.

Overall, the voting members do envision some slowing in U.S. growth this year, but, to quote Chairman Powell, they still feel the economy is “in a good place.” This outlook was essentially confirmed in the March policy statement. In addition, the lack of inflation places no urgency on the Fed to contemplate a rate hike anytime soon, even though core measures are straddling the 2% threshold. Continue Reading…

The first Federal Open Market Committee (FOMC) meeting of 2019 is now in the books. While the result did not deviate from the market’s expectations on the rate front, the policy statement did provide further evidence that the Federal Reserve (Fed) is going about things in a different way than investors have been accustomed to over the last few years. Is this decision-making process the “new” normal? No, it is really just the “old” normal, or how the Fed typically conducts monetary policy when the Fed Funds Rate target is not zero.

Since the FOMC began raising rates in December 2015, and picked up the pace during the last two years, the plan was to move the Fed Funds Rate target away from zero, i.e., to normalize policy. Now, with the upper band of the policy rate target at 2.50%, or close to what is considered a neutral rate, the voting members have achieved their goal. So instead of raising rates in a somewhat gradual, but more importantly, predictable manner, further possible rate hikes will hinge upon upcoming economic data. In other words, monetary policy has become data-dependent. This is how the FOMC typically went about its business prior to the global financial crisis/great recession.

With inflation below the Fed’s 2.0% target, the policymakers can afford to be patient and, in the words of Chair Powell, “flexible” as well. Certainly, the decline in risk assets as 2018 came to a close created an environment of tighter financial conditions. The question now is whether that development had any visible, longer-lasting impact on economic growth.

Waters will be muddy for a while

So, where do things stand as the markets look ahead? Unfortunately, the waters will be muddy for a while. Due to the partial government shutdown, both the Fed and the bond market have not been receiving any fresh insights on the economy. The only exceptions have been the Bureau of Labor Statistics and private vendors. Continue Reading…

Despite Tuesday’s 3% plunge in US stock markets, Franklin Templeton money managers are optimistic most major asset classes will deliver positive if muted returns in 2019.

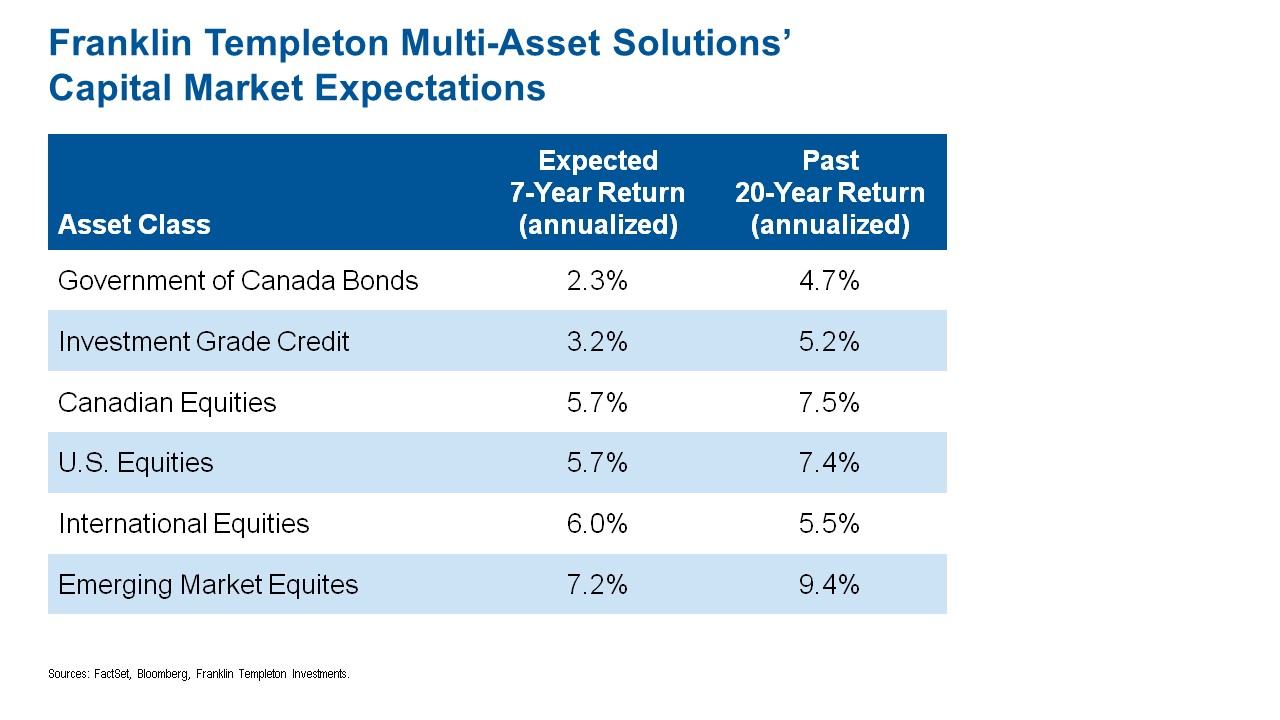

At the 2019 Global Market Outlook event in Toronto, William Yun, New York-based executive vice president for Franklin Templeton Multi-Asset Solutions, projected 7-year annualized returns for Canadian equities of 5.7%, compared to a 7.5% average the last 20 years [as shown in above chart]; 5.7% for U.S. equities (versus 7.4% historically), 6% for international equities (versus 5.5%), and 7.2 versus 9.4% for Emerging Markets. On the fixed income side, he is projecting 2.3% annualized 7-year returns for Government of Canada bonds (versus 4.7% historically the last 20 years), and 3.2% for investment grade corporate bonds (versus 5.2%).

All this is in an environment of continued desyncronized global growth (of 3%) and moderate inflation expectations. Long term, Yun is particularly optimistic about the long term growth of Emerging Markets equities, which at 5% is two-and-a-half times the 2% growth expectation for developed market equities. This optimism is based on positive population growth and labor productivity in Emerging Markets. Globally, inflation “remains muted” and “we don’t see many excesses in the global economy generally.” There are however, some excesses in the U.S. labor market.

More normalized interest rate environment

William Yun, Franklin Templeton Multi-Asset Solutions

Capital spending growth patterns are supportive and trending upwards since the 2016 US election, with the transition from very low interest rates post the financial crisis to a “more normalized interest rate environment.” The opportunity is to reinvest capital to more productive assets, as opposed to allocating to corporate share buybacks.

With respect to central bank balance sheets, markets are normalizing around the world, transitioning from excessive Quantitative Easing to Quantitative Tightening and shrinking balance sheets. Assets quadrupled at the Fed between US$1 trillion in 2008 to $4 trillion today as the Fed committed to buying bonds, with liquidity tapering off. He has similar expectations for the ECB, which has announced the ending of its QE programs, and it’s the same with Japan and China. “Central bankers are pulling back on Quantitative Easing.” There is a “restart of normalization in interest rate policy.”

Rising volatility

Even as the Dow Jones Industrial Average was in the process of tanking almost 800 points Tuesday, Yun predicted rising volatility after a period of relative calm. In that environment, “investing passively [in index products] has been the way to go but we anticipate volatility returning.” With higher interest rates and more volatility, it may be a time for active management, Yun said, acknowledging his own firm’s expertise in active security management.

Emerging Markets gross domestic product (GDP) continues to rise relative to the rest of the world, from 40% in 1990 to 60% in 2017, and Yun expects that percentage to move higher still. The trend is driven by rising consumption growth for the middle class, which benefits industries like consumer staples and consumer discretionary stocks, technology and even investment management.

Emerging Markets are showing reduced reliance on developed markets, which are slowing. Whereas in 2007 eight of the top trade markets were with the United States, in 2017-2018 China has supplanted the US, with 8 of the top 14 destinations.

In short, Yun sees a supportive global market for risk assets but lower returns: positive growth and moderate inflation, with increased volatility.

Ian Riach, Fiduciary Trust Canada

Ian Riach, Chief Investment Officer for Fiduciary Trust Canada and a senior vice president of Franklin Templeton Multi-Asset Solutions, says it makes sense in this environment to make some “dynamic” (i.e. tactical) shifts to long-term Strategic Asset Allocation. Currently, the firm is underweight Canadian equities and Canadian bonds, because the loonie has been getting weaker and Canada is facing a number of challenges ranging from trade to energy to a shrinking manufacturing base, all of which “affects growth going forward.” In the short term, Riach expects short-term interest rates in the United States will be higher than in Canada, “given that they are growing more quickly than us.”

Flat yield curve

Even after the recent rate back-up, “we think Government of Canada bonds are expensive, Continue Reading…

The new trade deal with our neighbours to the south will have wide-reaching effects across all areas of our economy, and housing is no exception. While the agreement is said to be good for our economy overall, it’s not necessarily good news for your ability to afford a home.

What is the USMCA?

Canada recently reached an agreement with the United States and Mexico to replace NAFTA, the decades-old trade agreement that has stood since it was signed by Brian Mulroney, Bill Clinton and Carlos Salinas de Gortari.

The new agreement looks much like the old one, with some changes. Key differences include changes to the way the three countries approach auto manufacturing, fewer restrictions on trade of dairy products, and stronger measures against counterfeiting and media piracy. Like NAFTA, the USMCA makes it possible for the three countries to exchange goods without barriers.

For now, the US, Mexico and Canada will continue trading under the rules of NAFTA. The USMCA will come into effect once it’s ratified by its members, a process that could take months. In the United States, congress won’t vote on ratification until some time next year due to that county’s mid-term elections. Here in Canada, the looming Federal election means that if the USMCA isn’t made official by June, it could be delayed until 2020.

How does this affect Canadian housing?

If you’re wondering how having access to American milk at your local Superstore can possibly affect how much mortgage you can afford, you’re not alone. The implications for home affordability are driven by the market’s reaction to the uncertainty of the negotiation period, the removal of uncertainty brought by a signed agreement, and the actual economic growth that’s expected to occur because of the USMCA once it’s in force.

When the Trump administration demanded to renegotiate “the worst trade deal” ever, the market got spooked. As the trade war intensified, the US threatened to (and did) impose significant tariffs on imports from Canada. With repeated threats from our largest trading partner, there was a real chance that the Canadian economy could be jeopardized. Even though our economy was growing during that time, the Bank of Canada (BoC) was reluctant to raise interest rates, which it would normally do in that situation. Continue Reading…

There was little surprise in the October 24 decision by the Bank of Canada (BoC ) to raise its overnight interest rate a quarter point to 1.75%. There hadn’t been a sell-side strategist on Bay Street prognosticating anything but that action. BoC governor Stephen Poloz’s stop-start hiking program reinforces what we have been saying for some time: even with this tepid pace of interest rate increases, Canada is still Number Two in the “hawkishness” rankings of developed market central banks.

More important than the actual rate move is Poloz’s signaling, especially given NAFTA’s recent reconfiguration into the U.S.-Mexico-Canada Agreement (USMCA) and October’s generalized stock market malaise.

With the NAFTA overhang quasi-resolved, and the realization out west that shipping LNG to East Asia is not only politically palpable but a matter of national security, Poloz and the Canadian public finally have some good economic news in what has been a tough year for the country.

For an idea of the BoC’s relative position, consider the actions taken (or not taken) by several other major central banks of late. After hiking to 0.75% in August, the Bank of England appears to have its hands tied. It is hard to see how the Brits can make any moves between now and March 2019, the deadline for the to-be-determined “soft” or “hard” Brexit. Even if Brexit goes well, the BoE would seemingly need to take a cautious approach next spring and summer, meaning GBP rates will likely be a full 100 bps or more south of CAD’s throughout 2019.

The European Central Bank is also in no hurry to do much regarding interest rates. Given the VIX’s recent spike to 231amid China slowdown fears and Italian budget risk, any forecasts of a one-off rate hike by the ECB next year must be called into question. That is truer now than at any time in the last year or so, as Italian bonds maturing in 10 years have gapped up to 3.60%, a striking 320 bps spread over 10-year German bunds (0.40%).

The fear in southern Europe is of a “doom loop.” In this scenario, Italian banks, which are heavy owners of Italy’s sovereign debt, see the country’s yields rise, which weakens the banks’ capital base. That, in turn, sends government bond rates higher. A dog chasing its tail.

Of interest to the BoC, the Toronto housing market has somehow managed to pull off the sweet-spot slowdown, at least for now. This has surprised us, given the rarity of asymptotic price surges giving way to post-peak gentle, sideways slopes. The Teranet National Home Price Index for Toronto has managed to curve ever so slightly downward since summer 2017, witnessing total price depreciation of just 3.8% from the peak to September 2018.

If Street consensus is correct, the BoC will bring the policy rate to 2.25% or 2.50% at the end of 2019. There are some observers out there with calls for 2.75% or 2.00% on both sides of the bell curve. In order to have the confidence to hike three or four times, Poloz will want to see GTA home prices continue to click sideways with each of the Toronto Real Estate Board’s monthly reports. And that means no big swoons in activity like in Vancouver, where buyers and sellers are engaged in a staring contest that is becoming disconcerting.

Aggressive BoC rhetoric

In the Monetary Policy Report, the central bank went heavy on USMCA references, opening with the trade deal and then coming back to it again just a couple of paragraphs later. They were keen to make mention of British Columbia’s natural gas pipeline announcement as a one-two punch for justifying a confident onslaught of 2% on the overnight rate.

We are focusing less on the BoC’s forecast of around 2% CPI inflation from now to 2020 and more on the bank’s assertion that the economy is operating “at capacity.” This is critical. The U.S. still has some room to challenge its capacity utilization precedent, set just short of 80 on the eve of the 2015–2016 China scare. But for all intents and purposes, American capacity utilization at 78 is a rounding error compared to its limit (the 80 area).

If Poloz believes Canada is “at capacity,” and it looks to us like the U.S. is there too, then this is the stuff of inflation scares. Of the forecasting outliers (those penciling in 2.0% or 2.75% for year-end 2019), we think the latter camp has a better chance of being proven correct, on account of our thesis that the global trade war concept is overblown and “priced in.”

Items to watch, next 6 to 12 months

While we would be foolish to not focus on “classic” central banking metrics such as inflation and employment a few other idiosyncratic issues are also critical: Continue Reading…