Now that interest rates have finally appeared to bottom, consumers are starting to worry about the prospect of rising rates and their impact on their personal finances.

Now that interest rates have finally appeared to bottom, consumers are starting to worry about the prospect of rising rates and their impact on their personal finances.

This is explored in my latest article, which is in Monday’s Financial Post (e-paper and online). You can access it by clicking on this self-explanatory highlighted headline: Only a quarter of Canadians have a rainy day fund, but more than half worry about rising rates.

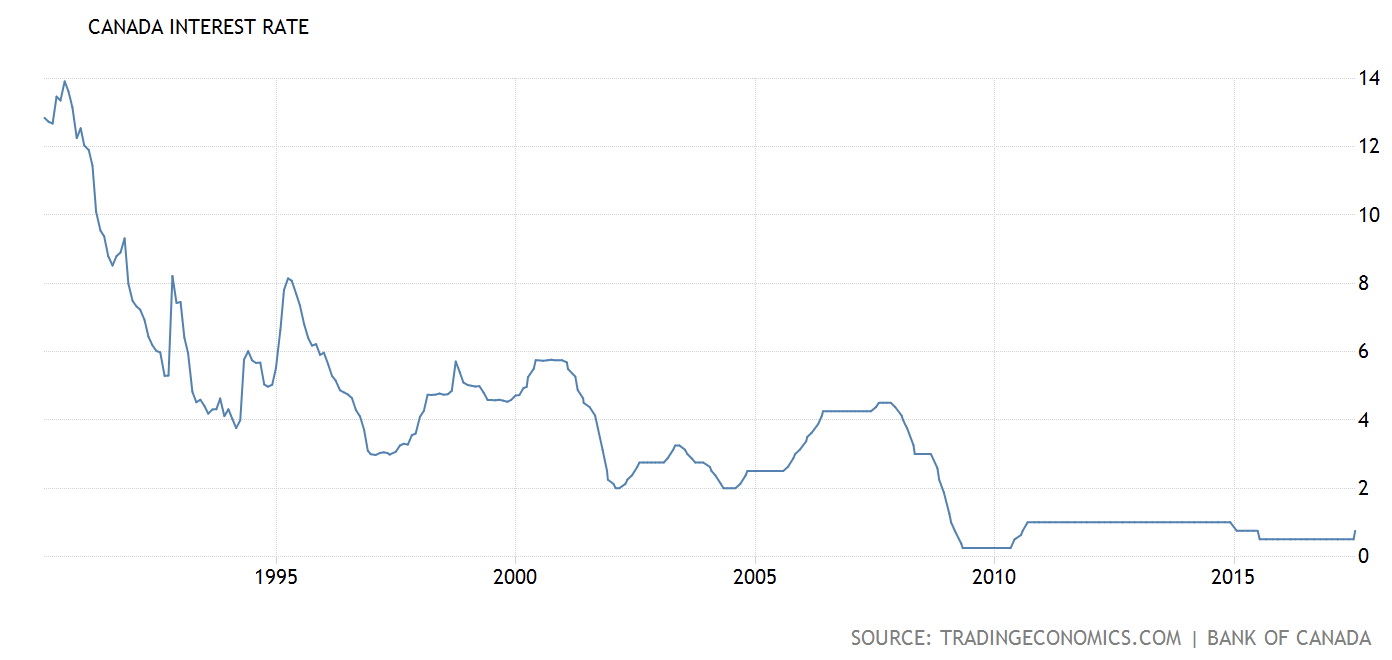

It describes a new Forum Research Inc. poll that shows more than half of Canadians (51%) fear rising rates will negatively impact their personal finances. The national poll of 1,350 voting-age adults was conducted after the Bank of Canada raised the prime interest rate from 0.75 to 1% on September 6th, which in turn followed an initial 0.25% hike in July.

After an amazing run of nine years of ultra-low interest rates, it’s clear consumers are starting to fret the party is over. Anyone with variable-rate mortgages might well be petrified that interest rates could again reach the high teens, as they did in the early 1980s. Little wonder that many homeowners are starting to “lock in” to fixed mortgages while rates are still relatively low.

Of course, as Credit Canada’s Laurie Campbell notes, for the longest time it’s paid to stay variable and flexible, whether with a variable-rate mortgage or a line of credit. It does cost a bit more to “lock in” to fixed mortgages, as Campbell notes, but the ability to sleep well at night in my opinion more than makes up for the difference.

While the poll asked specifically how consumers felt about the second hike, “they are worried more are coming,” Forum Research president Lorne Bozinoff told me. 12% say the negative effect will be extreme. However, 17% believe rate hikes will have some positive aspects: you’d expect debt-free seniors to welcome higher returns on GICs and fixed-income investments. Another 38% don’t think it will have an effect either way.

A quarter have no emergency savings at all

Bozinoff is more concerned that 26% of respondents have no emergency savings, and 40% have a cushion of a month or less: 9% have less than a month and 11% just a one-month cushion.

Financial planners generally recommend three to six months as a hedge against job loss or other setbacks. A minority do: 14% have two to three months, 9% four to five months, and 13% six months to a year. Only 15% have a year or more and predictably, 56% of the latter group are 55 or older. Continue Reading…