If there is one thing COVID-19 has not impacted, it’s RRSP season. March 1, 2021 is the deadline for contributing to an RRSP for the 2020 tax year. The question is, should you?

The basics: Anyone who files an income tax return can contribute 18% of earned income to a maximum of $27,230 for the 2020 tax year. If you have an employer-sponsored pension plan, your RRSP contribution limit is reduced by the Pension Adjustment (PA). Unused contribution room can be carried forward to use in the future.

Generally speaking, RRSPs make sense for anyone who wants and can afford to invest for the long term. Here’s why:

Pros

Contributions are tax deductible.

Earnings grow tax-sheltered within the plan.

You can defer tax on investment earnings and contributions to the future. This is particularly useful if you are a high-income earner and your marginal tax rate is likely to be lower in the coming years.

RRSPs can hold a wide range of qualified investments. For example, you can hold GICs, savings bonds, Treasury bills, bonds, mutual funds, Exchange Traded Funds (ETFs), equities (both Canadian and foreign), and income trusts in an RRSP.

Deciding what to hold in your RRSP really comes down to the same factors you have to consider when making any type of investment: your comfort level with risk, your investment objectives and your time horizon. For example, if your goal is to grow your wealth over time and market volatility doesn’t keep you up at night, then you may want to consider growth investments such ETFs, mutual funds and stocks. If you want income, then income-generating and interest-paying investments are worth looking into.

All of this said, RRSPs do have their drawbacks.

Cons

While you can withdraw funds from an RRSP before you retire, you will have to pay a withholding tax and you also have to report that money as taxable income to the Canada Revenue Agency.

The Government of Canada controls the amount of money that must be withdrawn annually once the RRSP matures. When you convert the RRSP to an Registered Retirement Income Fund, which must be done when you turn 71, you are required to withdraw a minimum amount each year starting at age 72 even if you don’t need the money.

RRSPs work best for people who can use a tax deduction and can afford to put money away for the future. Another consideration: Is your income in retirement (and therefore the marginal tax rate you’ll have to pay) going to be equal to or greater than it is during the years you can contribute to an RRSP? If this is the case, you won’t be achieving any tax savings by contributing to an RRSP. However, you could still benefit from deferring tax. The question then becomes, do you pay the income tax now or later? Continue Reading…

By Jeffrey Schulze, CFA, Director, Investment Strategist with ClearBridge Investments, a Specialty Investment Manager of Franklin Templeton

(Sponsor Content)

There are times to follow the herd and there are times to stray away from the pack. Investors must learn this lesson. Sometimes, it can be beneficial to follow a larger group, but there are moments when it can make sense to chart one’s own course. In the early and middle stages of an economic expansion, running with the herd can be a beneficial and safe proposition.

As the U.S. recovery unfolds, some investors may be tempted to break off, worried about the formation of a bubble. Indeed, many investors are concerned that the market may be overheating, based on metrics such as the forward earnings of the S&P 500 Index.

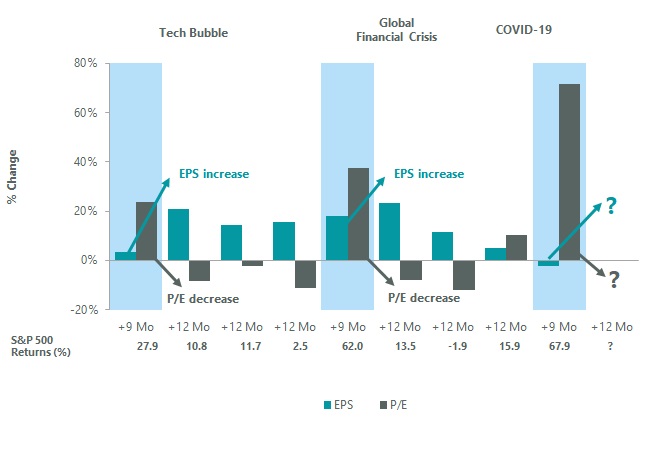

Importantly, an increase in equity multiples is not uncommon during the early stages of an economic expansion. Following recessionary troughs, market returns tend to be driven by price-to-earnings (P/E) multiples during the initial market rally (approximately nine months) as investors anticipate an eventual earnings rebound. As the recovery matures over the subsequent two years, the opposite dynamic occurs, with multiple compressions on the back of stronger earnings growth. Put differently, earnings typically make a significant contribution toward stock returns during this second phase of the rally and declining P/Es become a modest drag on returns (see Exhibit 1 below).

Exhibit 1: Multiples vs. Earnings Data as of Dec. 31, 2020. Source: JP Morgan.

As we move through 2021 and eventually into 2022, we expect this same pattern to unfold; however, multiples may remain elevated.

Higher multiples not uncommon early in Expansion

Valuations are elevated in part because investors correctly sniffed out the budding U.S. economic recovery. Unprecedented stimulus actions (both monetary and fiscal) short-circuited the typical bottoming process, as policymakers formulated a response that rapidly ended the economic crisis and fueled an upturn in financial markets.

ClearBridge Investments has been tracking the scope of this improvement, and we see an overall expansionary green signal since the end of the second quarter of 2020. In our view, it has become clear that a durable U.S. economic and market bottom has formed, with the S&P 500 up 67.9% from the lows and a third-quarter GDP rebound of +33.4%, as of December 2020. Continue Reading…

Lowrie Financial/UnsplashBy Steve Lowrie, CFASpecial to the Financial Independence HubSometimes, it takes years for key investment lessons to play out to the point we get to say, “See? Told you so.”Not so in 2020. Now that this excruciating year is behind us, we can at last appreciate the remarkable crash course it offered in nearly every principle inherent to successful long-term, goal-focused investing.

Where to begin? Let’s start with the power of planning.

Lesson #1: Planning beats reacting

“Short-term thinking repeated again and again doesn’t lead to long-term thinking.” — Seth Godin

You were there, so you probably remember: Major global stock markets declined from near all-time highs in mid-February to a low on March 23rd (34% in 33 days).

Few of us saw that coming. Fewer still might have guessed things would so abruptly reverse, to end 2020 with new highs, well into positive territory. The U.S. stock market reached new heights last summer, even as the pandemic and its economic devastations raged on. The Canadian stock market reached a new high recently on January 7, 2021. Europe and other global stock markets still have a way to go.

The lifetime lesson here, and my key, repeated observation for 2020, is simply this:

The economy can’t be forecast, and the market cannot be timed. Instead, have a long-term plan and stick to it during dramatic turning points.

Planning as opposed to reacting: this is your and my investment policy in a nutshell, once again demonstrating its enduring value. Consider these points:

Much ado about nothing: The velocity and trajectory of the equity market recovery nearly mirrored the violence of the February/March decline. For those who like to relate letters of the alphabet to economic or market performance charts, the 2020 stock market chart was a pretty pronounced V.

Patience is a virtue: In volatile markets, it’s tempting to “wait for the pullback” once a market recovery is underway, and/or wait for the economic picture to clear before investing. Either or both formulas are more likely to underperform compared to simply sticking with your disciplined plan.

Lesson #2: In investing, “shiny and new” often isn’t

“Modern portfolio management tools give today’s investors control over their own savings, insight into fees and performance, and the luxury of watching their money vanish in real-time when markets plunge.” — Tim Shufelt, The Globe and Mail

The most significant behavioural mistakes investors make (individuals and institutions alike) are panicking in a down market or getting caught up in the allure of a hot market fad. While both can be severely hazardous to your financial health, my experience is that chasing hot new trends is often the most damaging.

Today’s trends may be new, but the lesson is all too familiar: A hot new investment trend is wonderful and exciting … until it’s not.

For example, reading today’s financial news, I sometimes wonder if I have been asleep for the past 20 years, like Rip Van Winkle. Have I just woken up in the tech boom of the late 1990s, when there was more than an average number of hopeful investors trying to score big on the latest tricks of the trade? If you’ve been around as long as I have, you know that didn’t end well. A lot of investment portfolios were left woefully deflated once that bubble burst.

From the adventures of day-trading brokerage accounts, to chasing the latest hot IPO, to piling into large technology companies (regardless of their bloated valuations), the similarities between then and now are uncanny. Today, we could add record-busting bitcoins and blank-check SPACs to the mix.

Then and now, rising markets often tempt the uninitiated to abandon their well-diversified portfolios to chase after the “easy” money. Then and now, your best move remains the same: stay diversified. Concentrated bets on hot trends generate wildly unpredictable outcomes, which makes them far closer to being dicey gambles than sturdy investments.

Put another way, if investing were a school, the markets charge a steep tuition to those who don’t heed their history lessons. I wonder if 2021 could be an expensive year for those chasing the latest hype?

Lesson #3: Be selective in your media diet

“Wow. If I’d only followed CNBC’s advice, I’d have a million dollars today … provided I started with $100 million dollars. How do they do it!?” — Jon Stewart, The Daily Show

This is a topic for deeper discussion, but it’s worth including in our 2020 reflections: Investors should remember that popular and social media is much better at hyping extreme news than offering calmer views. Continue Reading…

Special to the Financial Independence Hub Many financial advisors, analysts and investing gurus alike argue in favour diversification.

That said, there are some experts who claim owning about 30-40 individual stocks, in various industry sectors, will provide modest diversification to mitigate portfolio risk.

Dedicated readers of this site will know I’m a fan of portfolio diversification myself, since I adhere to some personal rules of thumb when it comes to my DIY portfolio. Here are some of those rules of thumb:

I strive to keep no more than 5% value in any one individual stock.

I’m working on increasing my weighting in low-cost ETFs over time, more specifically, owning more of the U.S. market since I’ve had a long-standing bias to Canadian dividend payers in my portfolio.

Portfolio diversification aims to lower the volatility of my portfolio because not all asset categories, industries, nor individual stocks will move together perfectly in sync. By owning a large number of equity investments in different industries and companies, and countries, those assets may rise and fall differently; smoothing out the returns of my portfolio as a whole.

“There is a close logical connection between the concept of a safety margin and the principle of diversification.” – Benjamin Graham

As I contemplate semi-retirement in the coming years, this is what I’m considering for cash on hand to support any bearish equity markets or to ride out unfavourable market returns.

Diversification: applying some knowledge and lessons learned

With 2020 in the rear-view mirror, and a trying investing year for many to say the least (!), I decided to make a few portfolio changes so I could embrace diversification more while simplifying my portfolio as those needs for capital preservation draw nearer.

Today’s post outlines some of those changes, by account, and why.

1.)TFSA

I’ve admittedly been wrestling a bit for what to invest in, inside this account for the current 2021 contribution year.

I know I need some more U.S. and international exposure even with the recent comeback in many of my Canadian stocks since the market calamity began in March 2020.

In looking at my sector allocation to the oil and gas industry, I decided to cut complete ties in late-2020 with Inter Pipeline (IPL) after their dividend cut of 72% earlier in the year. You can see some of that dividend news I reported in this previous dividend income update.

I will use that money, along with new TFSA contribution room in 2021 to invest in some all-world ETF XAW amongst other investments.

XAW will provide far less yield inside my TFSA going-forward, which will impact the income generation machine that is my TFSA, but more importantly I think this fund will provide some much needed total return growth from ex-Canada.

Quite simply, as a fund of funds, iShares XAW is a simple, low-cost way to own U.S. international, and emerging market stocks.

I’ve long since listed XAW as one of the many great funds to own on my dedicated ETFs page. So, I’m eating my own cooking!

It’s the new year and you may have a couple of questions on how to use your TFSA account. The Tax Free Savings Account is one of the greatest additions to your investor tool kit. It is true to its name in that the monies grow completely tax free. When you take the monies out for spending there are no tax implications. We need only keep track of our contribution limits.

Out of the gate it’s important to know the contribution allowances. The program was launched in 2009 (the brainchild of then federal Finance Minister Jim Flaherty). The initial contribution limit was $5,000. There is also an inflation adjustment mechanism and that is why you will see the TFSA limits increase over time.

TFFA Limits History

The annual TFSA dollar limit for the years 2009 to 2012 was $5,000.

The annual TFSA dollar limit for the years 2013 and 2014 was $5,500.

The annual TFSA dollar limit for the year 2015 was $10,000.

The annual TFSA dollar limit for the year 2016 and 2018 was $5,500.

The annual TFSA dollar limit for the year 2019 was $6,000.

The annual TFSA dollar limit for the year 2020 was $6,000.

The annual TFSA dollar limit for the year 2021 is $6,000.

The total contribution allowance to date is $75,500 for 2021. You can carry forward any unused contribution space. Keep in mind that the eligibility for TFSA is based on age of majority. You would have had to have been 18 years of age or older in 2009 to qualify for that full amount. You would also have to be in possession of a Social Insurance card/number.

If you reached age of majority in 2018, that would be your first year of eligibility. To date your contribution limit would be …

Starting the TFSA in 2018

2018 – $5,500, 2019 – $6000, 2020 – $6,000, 2021 – $6,000 for a total of $23,500.

Of course we have to wait for January 1 or later to use that $6,000 for 2021.

Remember if you go over, you will be penalized by 1% per month, for the amount that you have overcontributed. Check with CRA for your contribution eligibility.

Reader question on over contribution

“Ooops, I over contributed in December of 2020.” If you recently jumped the gun and overcontributed by $6000 you would be charged 1% per month, meaning a $60 penalty. Thing is you earned another $6,000 in contribution space on January 1, 2021. You would only face one month of over contribution. You might as well sit tight. You would not be able to have that contribution reversed, even if you quickly move that money out of the TFSA account. If you move the monies in and out there will be no benefit, but you could created fees if it is stocks or ETFs.

If you ever make a more costly (but honest) mistake on over contribution, you can take that up with CRA and your financial institution. It’s possible that you might get some help from your institution or from the CRA. Good luck.

Calculating your TFSA after removing amounts

The formula or rule is quite simple. If you remove $12,000 in one year, you would add that full amount to next year’s contribution allowance. And of course that contribution allowance would also include that calendar year’s new room. For example if you took out $12,000 in calendar year 2020, you would add that $12,000 to the $6,000 allowance for 2021. Your 2021 contribution allowance would be $18,000.

Yes, you get to keep any contribution room gains you made in your TFSA if you sell. You lock in that space. Those investment gains can boost your total TFSA contribution room above the calendar year totals.

This event may be considered if you were looking to use or gift some monies next year. You might sell now and lock in that TFSA space. Obviously, if you’ve been investing those monies, your account is likely or should be at an all-time high.

Please note that if it is a stock or bond or ETF or mutual fund, the trade has to settle within the calendar year. Check with your discount brokerage or advisor on timing and settlement details.

Saving or Investing for your TFSA?

I am a big fan of using your TFSA for investing. There’s the potential or likelihood of much greater gains and hence much greater tax savings when you invest your TFSA dollars.

Also consider that interest rates are sooooo low you might have very modest ‘gains’ with any savings account. The benefit of the TFSA for savings is more muted in a low interest rate environment.

But of course, 2020 proved to many the importance of that emergency fund. You might hold an emergency fund that is 6 months of total spending needs as a starting point. Here’s my personal finance book, OK it’s a blog post …

And it can make sense to hold some cash as a portfolio asset. After all it’s an obvious hedge for any deflationary environment. The spending power of cash will increase in any deflationary period.

On that cash front you might consider EQ Bank where you can earn 1.5% in a savings account and 2.3% in registered account such as that TFSA. You may choose to hold some TFSA amounts in savings and some in higher growth investments.

On the mutual fund front you might have a read of this post from Jonathan Chevreau on the top mutual funds in Canada. I am a big fan of those funds from Mawer.

Beneficiary form – successor holder

Ensure that you fill out a beneficiary form for all of your registered accounts. For taxable accounts you might consider joint accounts. Continue Reading…

By Allan Small

By Allan Small