By Michael J. Wiener

There aren’t many financial gurus willing to call out financial companies by name for their bad behaviour, but Ramit Sethi is one of them. In his book I Will Teach You to be Rich, he promises “a 6-week program that works,” and he includes advice on which banks to use and which to avoid.

The book is aimed at American Millennials; Canadians will learn useful lessons as well, but much of the specific advice would have to be translated to Canadian laws, banking system, and account types. The book’s style is irreverent, which helps to keep the pages turning.

It may seem impossible to fix a person’s finances in only 6 weeks, but this is how long Sethi says it will take to lay the groundwork for a solid plan and automate it with the right bank accounts and periodic transfers. The execution of the plan (e.g., eliminating debt or building savings) will take much longer.

Sethi is rare in the financial world because he will say what he really thinks about banks. “I hate Wells Fargo and Bank of America.” “These banks are pieces of shit. They rip you off, charge near-extortionate fees, and use deceptive practices to beat down the average consumer. Nobody will speak up against them because everyone in the financial world wants to strike a deal with them. I have zero interest in deals with these banks.” For the banks he does recommend, “I make no money from these recommendations. I just want you to avoid getting ripped off.”

People have many reasons why they can’t save and are in debt, but Sethi sees them as just excuses in most cases. “I don’t have a lot of sympathy for people who complain about their situation in life but do nothing about it.” “Cynics don’t want results; they want an excuse to not take action.” He urges readers to “put the excuses aside” and get on with the business of making positive changes.

The Program

The first step in the program is to “Optimize Your Credit Cards.” I found it interesting that Sethi focused on credit card perks before he covered eliminating credit card debt. He wants readers to “play offense by using credit cards responsibly and getting as many benefits out of them as possible” instead of “playing defense and avoiding credit cards altogether.” This approach sets him apart from many other experts on getting out of debt. While he does teach methods of eliminating debt, his focus is more on building wealth steadily.

The second step is to open “high-interest, low-hassle accounts.” Interestingly, he wants readers to open a chequing account at one bank and a savings account at another bank. Among his reasons are that the psychology of a separation between accounts makes us less likely to raid savings. Some might think opening a savings account is pointless if they have no money to deposit, but Sethi insists that you need to lay the groundwork now for a better future, even if you’ve only got $50 to deposit.

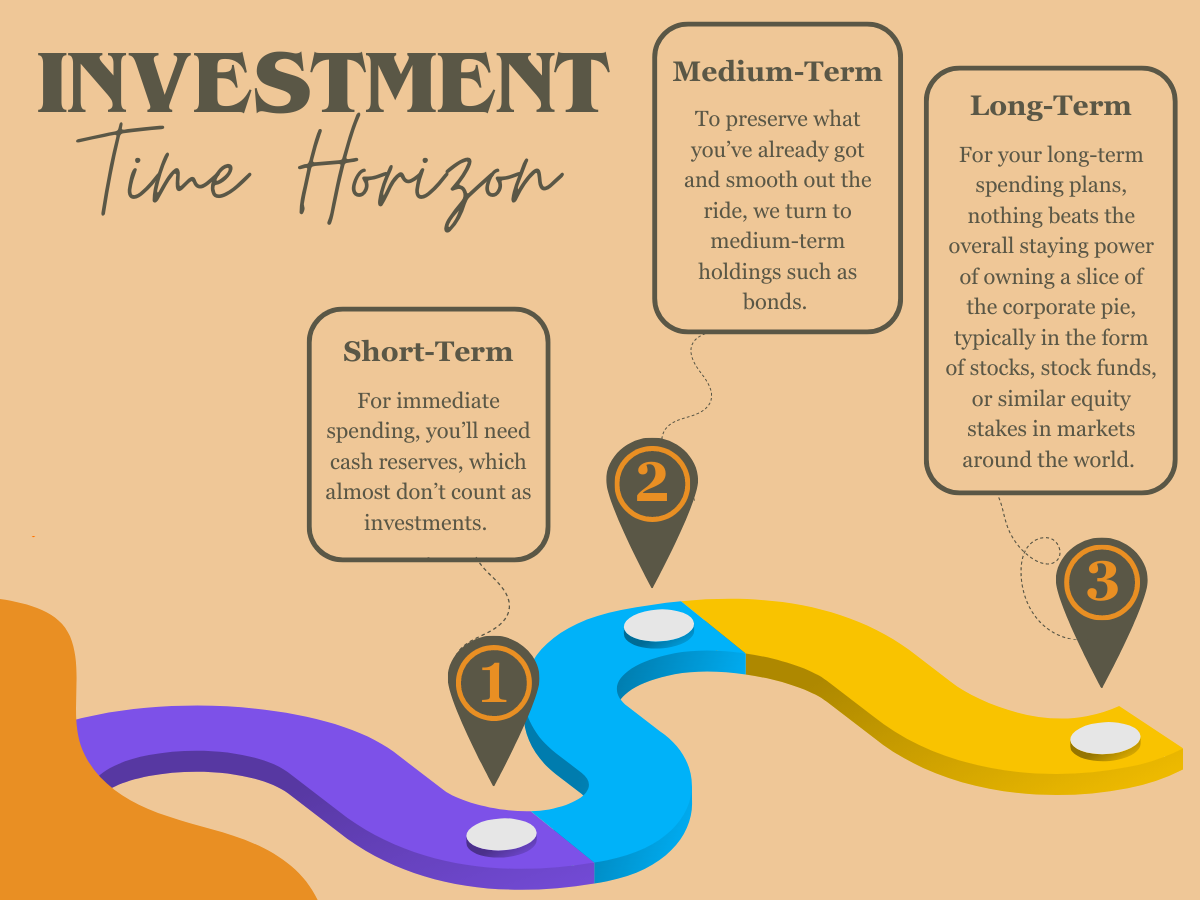

The third step is opening investment accounts. The author favours very simple investments, such as a Vanguard mutual fund account invested in a target date fund. “Don’t get fooled by smooth-talking salespeople: You can easily manage your investment account by yourself.” Unfortunately, Vanguard mutual funds are only available to Americans. Canadians can find one-fund solutions with certain Exchange-Traded Funds (ETFs).

To create the cash flow to reduce debt and invest, the fourth step is about “conscious spending,” which is “cutting costs mercilessly on the things you don’t love, but spending extravagantly on the things you do.” Achieving this involves tracking spending in different categories, but not traditional budgeting. Continue Reading…