By Dale Roberts, CuttheCrapInvesting

Special to the Financial Independence Hub

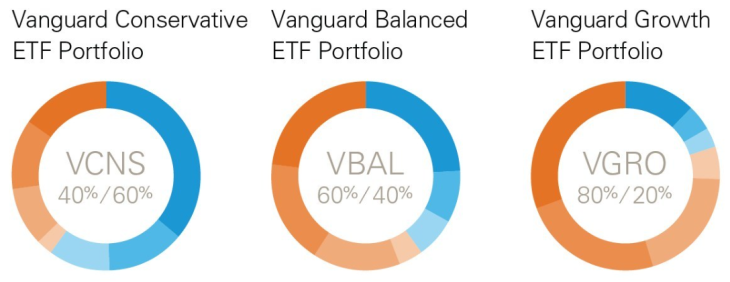

In February 2018 Vanguard Canada changed the investment game in Canada with the launch of complete Balanced Portfolios that you can purchase by entering one ticker symbol. For example, once logged into your discount brokerage account you would enter the symbol VBAL, and press buy to get a complete globally diversified Balanced Portfolio. The Portfolio is 60% Canadian, US and International stocks with 40% of those shock absorbers known as bonds.

Vanguard offers One-ticket Portfolios at five different risk levels. With an MER of .22% these portfolios are a game changer. (In the pie charts below, Orange shows equities and blue fixed income percentages).

iShares has also had One-ticket solutions available for several years. The asset allocation was ‘weird’ and the fees were not that low. considering the low fees on the underlying ETF assets. In response to Vanguard, iShares recently took the scrub brush to the funds, cleaned up the asset allocations and then cut the fees. In fact they undercut Vanguard just slightly with an MER of .20%. Here’s the link to the iShares product page; this will take you to XBAL, their Balanced Portfolio.

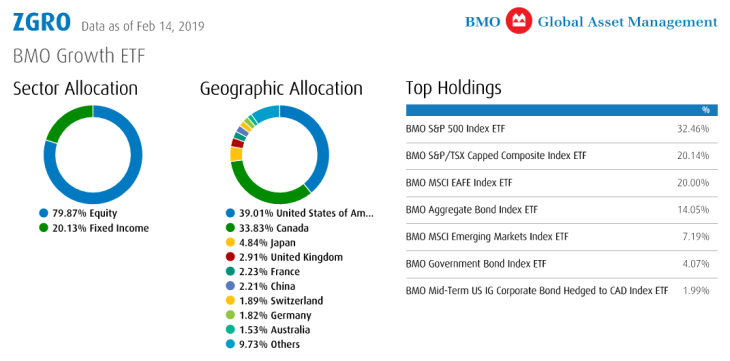

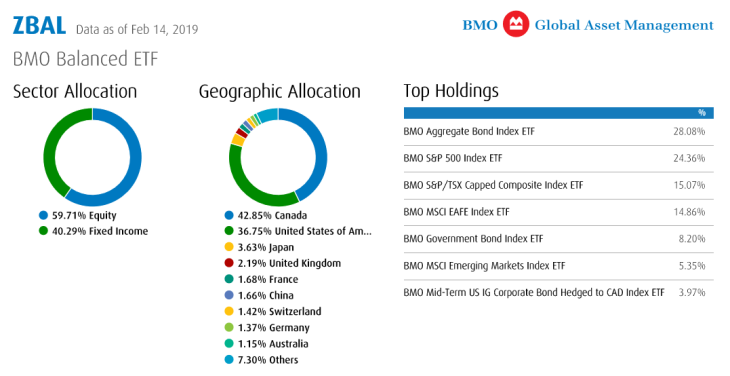

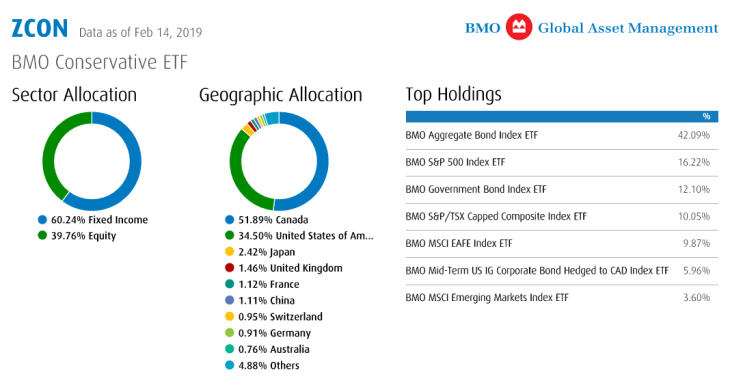

And then last week along comes one of the big banks with their own One-ticket offering. Here’s my review at the Hub: BMO keeps it simple with its One-ticket Portfolio Solutions.

The one-ticket solutions are the most cost-effective managed portfolios available in Canada. This should be the final dagger in the heart of the high fee mutual fund industry.

The one-ticket solutions are the most cost-effective managed portfolios available in Canada. This should be the final dagger in the heart of the high fee mutual fund industry.

Which One-ticket provider is best?

Let’s call it a draw. The portfolios are equally great. They include the basic and sensible asset allocation building blocks of Canadian, US and International stocks supported by a bond component. All the One-ticket providers use Canadian and foreign bonds to manage the risks.

How to select the right portfolio

Nothing is more important than investing within our risk tolerance level. We could argue it is the most important ‘part of it all.’ The Portfolios do not come with an owner’s manual for when and how to use them. Matching the appropriate portfolio to your risk tolerance level, time horizon and objective is key.

We have to invest within our risk tolerance level; bad things happen when we invest outside of our comfort level – usually permanent losses. We must be comfortable with the percentage and dollar value that the portfolio could decline.

Are you comfortable with a portfolio that could decline by 5% in a major correction, 10%, 20%, 30%, 40% or 50%?

Remember those bonds work like shock absorbers to soften the blow and smooth out the ride during periods when the stock markets tank. And tank they can; Canadian and US and International markets have declined by some 50% or more twice in the last 20 years. Continue Reading…