Based on the widespread media coverage of the 2016 Canadian census this week, Canada’s baby boomers are going to be just as much of a demographic force as ever once they enter their golden years. For the first time, our seniors now outnumber our kids, the CBC reported.

Based on the widespread media coverage of the 2016 Canadian census this week, Canada’s baby boomers are going to be just as much of a demographic force as ever once they enter their golden years. For the first time, our seniors now outnumber our kids, the CBC reported.

Not all seniors are baby boomers, of course, but sadly the reverse will soon be true: most if not all baby boomers will be seniors. For this generation retirement (or semi-retirement) is a huge looming event, as a quick browse of this site will establish. Hey, just this week I got a package from Service Canada advising me that I will be able to draw Old Age Security (OAS) when I turn 65 next April. And I intend to take it then too, as I wrote in MoneySense last August: Why I’m taking OAS right at 65.

Boomers need to face up to their own mortality

All of which suggests it’s time for Canadian boomers to start looking more seriously at their own mortality and the admittedly dreary topic of estate planning. I covered this Thursday in my latest MoneySense Retired Money column: Retirees need to start thinking ahead.

In my Financial Post article that ran on Wednesday, I looked at estate planning from a different perspective: how the original “Wealthy Boomer” — Donald Trump — is tapping his family members for senior roles in his administration and possibly for his business succession planning. Click on Donald Trump is upping the ante in the Wealth Transfer game.

One of the sources for the FP piece was business transition and valuation expert Ian Campbell, pictured. (He himself admits to his strong resemblance to investing legend Warren Buffett!). By coincidence I reached out to Ian about the Trump piece just as he had published a blog on that very topic. It ran on the Hub Wednesday under the headline Generational Business Transaction: The Apprentice. Check the links to his site for his free newsletter.

The Truth about Working in Retirement

Our best-selling (G&M, Amazon among others) book, Victory Lap Retirement, continues to get some positive reviews. Earlier this week Ellen Roseman of Toronto Star fame wrote the following review on Golden Girl Finance: The Truth about Working in Retirement. As Ellen recounts, she herself has retired from her full-time newspaper gig but continues to be fairly busy in the semi-retirement described in our book.

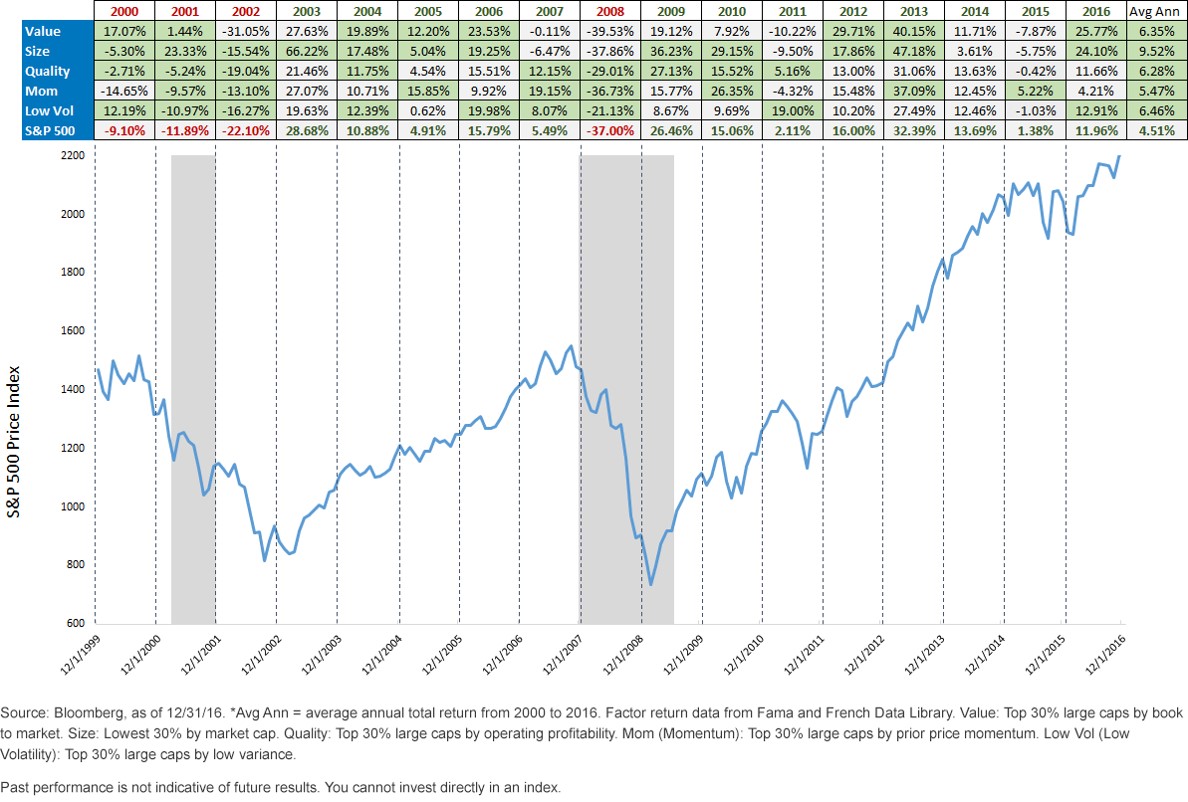

Mutual fund companies Excel Funds, Franklin Templeton enter ETF business

Finally, some big news in the asset management industry, where it was announced that two Canadian mutual fund companies — Excel Funds Management and Franklin Templeton Investments — are entering the ETF business. The Globe & Mail’s Clare O’Hara reported this on May 2nd. Click on Franklin Templeton, Excel Funds to enter Canadian ETF market.