Unfortunately, it’s rare for a startup to be successful long-term, let alone make it out of its first year alive. You’ve probably come across a lot of research that supports these claims. However, the information isn’t to scare you.

Instead, it’s to give you a realistic picture of how much it actually takes to be successful. If you don’t want your startup to be a part of the above research, you must first understand what contributes to a startup’s failure.

For many, it’s the financial challenges. Many startups don’t get enough money to cover what they need to start their businesses, they don’t manage the money well once they get it, or both. And when a startup is self-funded, it adds another layer of financial complexity that can lead to a failing operation.

Let’s discuss how you can reduce financial risk in your self-funded startup and make it past your first year in business and beyond.

Understand what it will Take to Fund your Business

Unless you’re someone with unlimited financial resources, how much money you can put into your startup is limited. You only have a certain amount to get your startup off the ground and maintain it until you turn a profit.

So, understanding what it will take to fund and run your business is critical. First, figure out what it will cost to launch and maintain your startup. Cover the following:

What are your product development costs?

Will you be renting an office space? If so, what are the associated expenses?

What are the cost of tech tools and software?

Will you have labor costs?

What will a marketing campaign for your launch and business cost?

What will your monthly expenses be?

What are your tax obligations?

Write down any other expenses unique to your startup that you’ll need to account for. Once you determine what the financial impact will be, you can create a realistic budget.

Create a Realistic Budget

To mitigate financial risk in your self-funded start up, you need to cling to your budget. Sticking with your budget ensures that you’re running your business within your means, can save some, and also afford your personal expenses.

Take the monthly business expenses you listed above and insert them into your budget. After that, input how much you’re bringing in each month. The hope is that your business pays for itself in the future. But factor in the personal money you put in to ensure your business stays afloat for now.

You’ll also want to detail how much money you’re allocating to business savings, an emergency fund, your tax account, and what you’re paying yourself.

Subtract your costs from your income and see what you have left over. If you’re in the negative, your next move is to find ways to cut costs. If you’re in the positive, consider investing the remaining amount or reinvesting it into your startup to keep growing. Continue Reading…

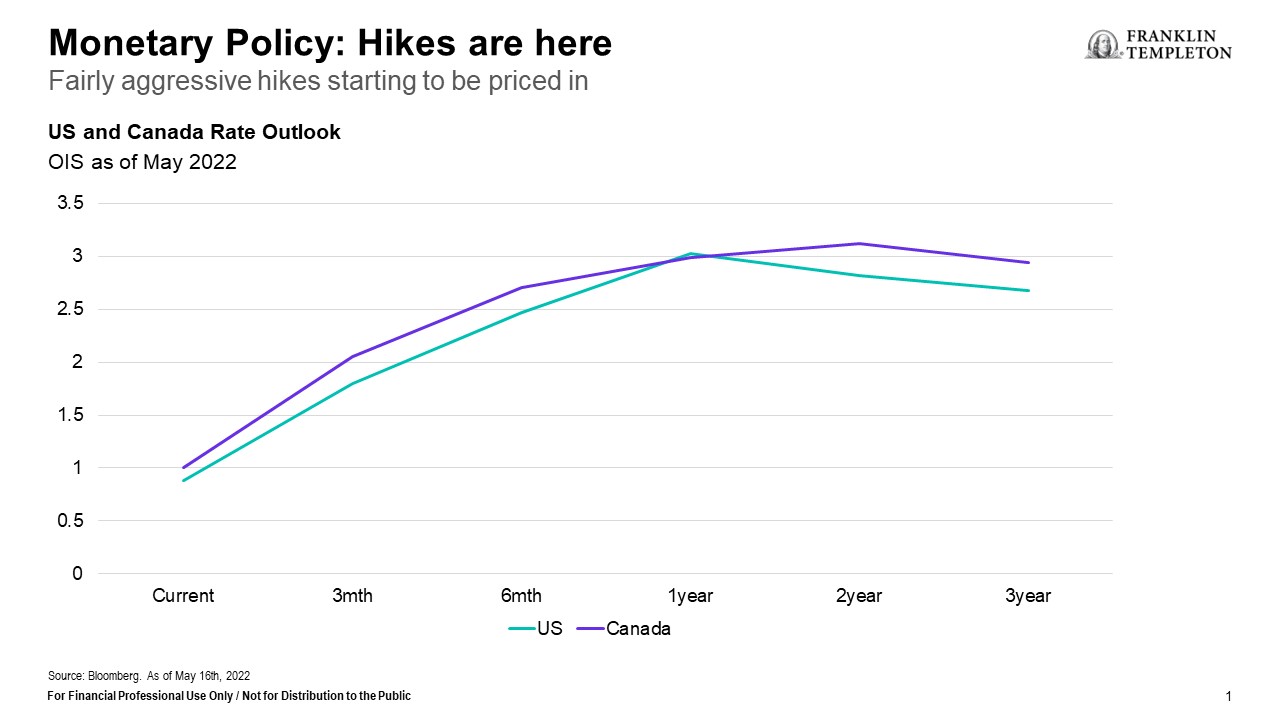

It’s been a volatile first half of the year for the world’s capital markets. In many countries, both equities and fixed income have declined, which has led to the second-worst performance for balanced portfolios in 30 years. Typically, bonds outperform stocks in down markets, but not this time. In fact, this has been the worst start to the year for fixed income in the past 40 years, thanks to higher inflation and the resultant rise in interest rates.

Supply-side inflation harder to tame

Central banks use rate hikes as a tool to curb demand for goods and services; but the current inflation is being driven more by supply-side issues stemming largely from the COVID-19 pandemic and exacerbated by the Russia/Ukraine war. Unfortunately, central banks have little influence over supply. All they can do is try to dampen demand with an aggressive interest-rate adjustment process, but they must be careful not to overshoot. Raising rates too quickly runs the risk of tipping weak economies over the edge into recession territory.

Canada’s most recent inflation imprint, released in June, showed an increase to 7.7% year-over-year. One negative consequence is that real incomes are being squeezed as inflation continues to accelerate.

Rates are rising quickly

Both the U.S. Federal Reserve (Fed) and Bank of Canada (BoC) have increased their overnight lending rates from essentially 0% prior to March of this year to 1.5%-plus in June. The Canadian futures market had priced another 75-basis point (bp) increase at BoC meeting in July, which ended up an even higher 100-bps with indications of more to come in September.

Rising interest rates are hurting several sectors of Canada’s economy, notably real estate — especially risky for the economy as housing and renovations have been leading Gross Domestic Product (GDP) growth for the past few years. A significant correction in that sector could lead to a recession.

If there is any silver lining in the current situation, it may be in the Canadian dollar versus its U.S. counterpart. Short-term rates in Canada have moved higher than in the United States. This differential, along with the direction of oil prices, affects the value of the Canadian dollar against the U.S. dollar. If the differential widens and stays higher in Canada, the loonie will likely benefit.

Recession risks are growing

The likelihood of recession is hotly debated within our investment team. Recession in North America is not our base case, but a soft landing will be very difficult. We are currently in a stagflationary environment and recession risks are increasing daily. Europe may already be in recession.

The stock market is a good leading economic indicator, and its recent decline indicates the risk of recession is rising. In addition, the yield curve is very flat, which typically portends an economic slowdown. These market signals have somewhat altered our team’s thinking. Given the current environment, we are reducing risk in our portfolios. In fact, we recently went slightly underweight equities.

Regionally, we are reducing the Europe weighting as that region is more exposed to the negative headwinds associated with war. We are slightly overweight the U.S. but acknowledge that valuations are subject to disappointment with declining earnings growth. We are overweight Canada, which continues to benefit from rising resource prices. Continue Reading…

Since the global financial crisis of 2008, markets have for the most part been a one-way train. Even the precipitous decline of the Covid-crash of early 2020 was erased so quickly that several months later it seemed like little more than a bad dream.

In such a favourable and long-lasting environment, risk management has increasingly become regarded as a four-letter word. Any attempt to mitigate risk and protect investors from large losses has been a money losing proposition. It has been a drag on returns and has done little to reduce volatility. Simply stated, risk management isn’t of much use when there has been no risk to manage.

Defining a Bubble: Like Catching Water in a Net

There is no universally accepted definition of a bubble. Identifying one is part art and part science and can only be done with certainty in hindsight once a bubble has become a matter of record.

Parabolic gains in markets in and of themselves may or may not signal a bubble. Similarly, situations where valuations stand significantly higher than their long-term historical averages cannot be conclusively classified as bubbles.

Further complicating matters, bubbles tend to be accompanied (if not caused) by a broad-based mindset among investors, which by definition is difficult, if not impossible to measure or define.

Behavioral Characteristics of Bubbles: Zero Fear & Speculative Frenzy

One of the most common and powerful characteristics of bubbles is a widespread belief that stocks can only go up. Aided and abetted by historical precedent, many investors have become emboldened by growing faith in a perpetual Fed “put,” whereby the central bank will move aggressively to support (and even reverse) any significant decline in markets.

Relatedly, this complacency has led to a surge in speculative madness during which a growing number of investors have piled into riskier assets, causing parabolic gains. One does not have to look far to see several signs of such behaviour, including:

Meme stock madness: GameStop and AMC, two companies in declining industries which respectively rocketed up 120x and 38x from their post-pandemic lows to their 2021 highs.

Crypto craziness: Dogecoin, which was originally conceived as a parody, went up nearly 300x to a market cap of $90 billion, spurred by tweets from Elon Musk.

Electric vehicle ecstasy: Hertz’s stock surged by simply announcing that it would purchase a fleet of Teslas. Similarly, Avis tripled in a day based on the mere suggestion that it might follow suit!

The Daunting and Consistent Math of Bubbles: It’s A Long Way Down

In the world of statistics, a 2 sigma event refers to something that occurs only 5% of the time. Using this framework, a market that is 2 sigmas above its long-term trend can be considered to be in bubble territory (or at the very least quite frothy). Using the same logic, a market that stands at 2 sigmas below its long-term trajectory can be thought of as mouth-wateringly cheap (or at least as somewhat of a bargain).

Founded in 1977, Boston-based Grantham Mayo Van Otterloo (GMO) is an investment management firm with roughly $75 billion in assets under management. It is well-known for its strong track record of asset allocation. The firm successfully identified and navigated both the tech bubble of the late 1990s and the real estate/financial bubble of 2006-7.

GMO analyzed the available data over financial history across all asset classes and identified more than 300 2 sigma observations. In developed equity markets, every single one of these observations over the past 100 years has fully deflated with prices falling back to their long-term trends. This pattern strongly suggests that:

The higher markets go, the lower their expected future returns.

The higher markets go, the longer and greater pain investors will have to endure to get back to trend.

Importantly, if you think that the recent decline in stock prices presents a golden opportunity to scoop up cheap assets, the fact that the S&P 500 currently stands about 40% above its long-term trend should be cause for sober second thought. This prospective downside is corroborated by Warren Buffett’s favourite valuation gauge, otherwise known as the Buffett Indicator, which is the ratio of the total value of the U.S. stock market to GDP. The indicator currently stands at 193%, which is approximately 50% above its historical average.

Make Mine a Triple

Using the 2 sigma definition of a bubble, in early 2021 it looked as if we might have a standard bubble. However, as the year progressed, the 2 sigma deviation progressed into an even rarer 3 sigma anomaly, which comes with an associated increase in potential pain.

Adding to concerns, real estate assets have arguably joined the bubble-party in stocks. Houses in the U.S. stand at the highest multiple of family incomes ever: even ahead of levels that prevailed prior to the housing bubble of 2006-2007. Alarmingly, this lofty multiple is lower than the corresponding level in other countries (Australia, the UK, China, and our very own Canada). Continue Reading…

Last month, I had the privilege of meeting legendary investor Larry Hite.

Larry was born into a lower middle-class family, had a major learning disability, did poorly in school, and was completely blind in one eye and half blind in the other. In his own words, “I was not handsome. I was not athletic. Whatever I did, I sucked at it badly.”

In 1981, after dabbling as a music promoter, actor, and screenwriter, Hite founded Mint Investments. Mint was a true pioneer, eschewing human judgment and instead basing its investment decisions on a purely systematic, rules-based approach rooted in statistical analysis.

By 1988, Mint registered average annual compounded returns of over 30%. In its best year, Mint registered a gain of 60% (1987, the year of the stock market crash), and in its worst year, it produced a gain of 13%. By 1990, Mint was the biggest hedge fund in the world, with a record-breaking $1 billion under management.

When it awarded Larry the Lifetime Achievement Award, Hedge Fund Magazine wrote:

“Larry Hite has dedicated the last 30 years of his life to the pursuit of robust statistical programs and systems capable of generating consistent, attractive risk/reward relationships across a broad spectrum of markets and environments and has inspired a generation of commodity trading advisers and systematic hedge fund managers.”

Although Hite began his investing career in the early 1980s, his philosophy of markets and approach to investing are remarkably similar to our own, which are summarized below.

Failure: A Foundation for Success

Hite maintains that his early failures were instrumental in his eventual success. He believes that accepting that failure is sometimes inevitable led him to develop an investment strategy that would limit losses.

In his book, The Rule, he wrote:

“I believe the success I’ve had arrived because I always expected to fail big. Solution? I engineered my actions so that a failure could not kill me. I won because I expected to lose. Failure became my advantage. Once you understand your potential for failure – that is, there are times you can’t win – you know when to fold your cards and move on to the next. You will do this more quickly than others who stay in the game too long, hanging on and hoping that their losing bet will turn around.”

It’s not all about Being Right

Many investors focus on being right as much as possible – on maximizing their ratio of winning vs. losing investments. On its face, this seems like a good idea – all else being equal, if you win more than 50% of the time, then over time you will make money.

Hite takes a different approach. Whereas he has no issue with trying to be right as often as possible, he is far more focused on maximizing the average magnitude of his winning positions relative to that of his unsuccessful ones, asserting that:

“Becoming wealthy and successful isn’t simply about being right all the time. It’s about how much you win when you are right as well as how much you lose when you are wrong…. The Mint trading system did not prioritize being right all the time. We prioritized not losing a lot when we lost but winning big when we won. But as a result, we were frequently wrong. We understood and expected this and taught our clients the wisdom too.”

Risk: A No Fooling Around game

Hite places a greater emphasis on risk management than on generating profits, claiming that mistakes regarding risk can lead to catastrophic results. He asserts that, “Risk is a no fooling around game; it does not allow for mistakes. If you do not manage the risk, eventually it will carry you out.”

His approach to investing clearly reflects his respect for risk. Specifically, Hite divulges that “We approach markets backwards. The first thing we ask is not what we can make, but how much we can lose. We play a defensive game.”

One of my favorite anecdotes regarding risk is Hite’s reflection on a conversation he had with one of the world’s largest coffee traders, who asked, “Larry, how can you know more about coffee than me? I am the largest trader in the world. I know where the boats are; I know the ministers.” Larry responded, “You are right. I don’t know anything about coffee. In fact, I don’t even drink it.” The coffee mogul then inquired, “How do you trade it then?”, to which Larry answered, “I just look at the risk.”

Five years later, Larry heard that this magnate lost $100 million in the coffee market. Upon reflection, Hite states, “You know something? He does know more about coffee than I do. But the point is, he didn’t look at the risk.”

Larry Hite

Market Predictions, Storytelling, & Good Copywriters

Larry is skeptical that anyone can predict markets. He in no way bases his approach to investing on making predictions, which he believes is an exercise in futility. In his own words:

“I respect the sheer intelligence and devotion of economists who have attempted to develop a unifying theory of market dynamics. But I don’t believe any such theory will hold up to scrutiny in the real world of money on the line. When you start believing you have remarkable market predicting powers, you get into trouble every single time.”

Hite is also critical of Wall Street research reports, claiming that they possess little investment value and are designed to exploit people’s natural tendencies to listen to entertaining narratives, stating:

“Stories began at the dawn of human society to entertain and instruct the next generation. We are wired to learn from well told stories. And unfortunately, Wall Street preys off our basic human weakness to want stories.”

In his typically blunt and straightforward manner, he adds, “When you start following slick reports filled with predictions, you’re just finding out who has good copywriters.”

A Computer can’t get up on the wrong side of the bed in the morning

Larry was a pioneer in his exclusive reliance on a data-driven, systematic approach, using statistical analysis of historical data to develop trading rules, which are the basis of his investment decisions. When he launched Mint Investments in 1981, his goal was “to create a scientific trading system that would remove human emotion from buying and selling decisions and rely instead on a purely statistical approach built on pre-set rules.” Continue Reading…

There may be a few ideas for anyone who, like myself, is in the “Retirement Risk Zone.” That’s the five years prior to and five years following your projected retirement date. If it’s 65, the traditional age, then the Risk Zone is between age 60 and 70. Based on the Hub’s demographic user patterns, a lot of people are in that category (although we actually have lots of millennial and Gen X traffic too on both sides of the border).

Towards the end of the blog, I talk about portfolio hedging. I have to credit my fee-for-service financial advisor for most of these concepts. He didn’t want to be named for the MoneySense blog but he is listed in the Hub’s “Guidance” section elsewhere in this site.

It took me awhile to accept that hedging — that is, using options or selling short certain ETFs representing the major indices — is as much a risk reduction strategy as it is a “risky” strategy.

Hedging means trading off some upside for downside protection

The best way I can describe it is that you’re willing to give up some upside in return for protecting the downside. Continue Reading…