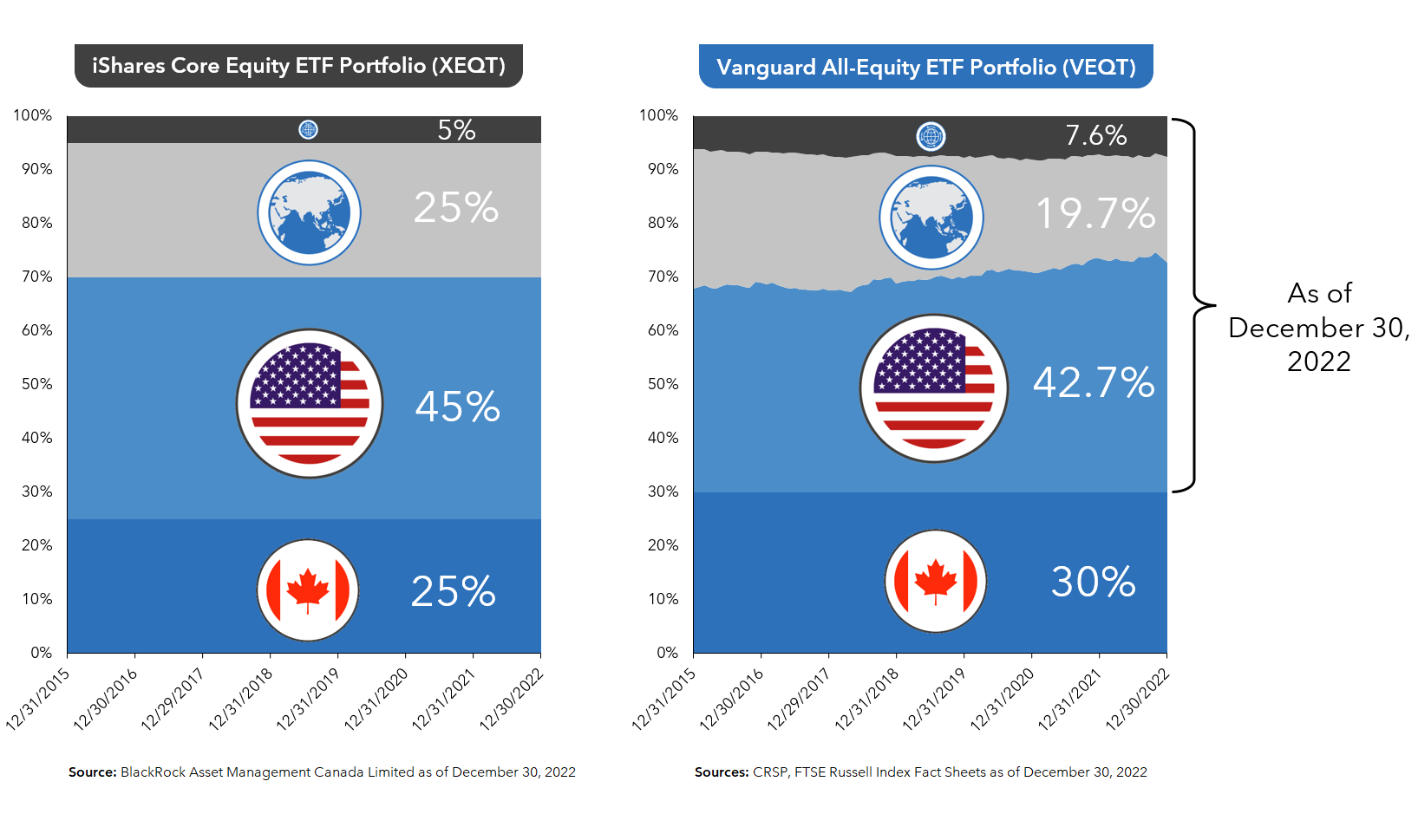

The 100% equity ETFs from iShares and Vanguard/Canadian Portfolio Manager

By Mark Seed, myownadvisor

Special to Financial Independence Hub

A reader recently asked me the following based on reading a few pages on my site:

Mark, does it make sense to have 100% of your portfolio in stocks? If so, at what age would you personally dial-back to own more cash or GICs or bonds? Thanks for your answer.

Great question. Love it. Let’s unpack that for us.

Members of Gen Z, which now includes the youngest adults able to invest (born in the late-1990s and early-2000s), represent a cohort that could be investing in the stock market for another 60 more years.

According to a chart I found on Ben Carlson’s site about stuff that might happen in 2023, over 60+ investing years in the S&P 500 (as an example) historical indexing performance would suggest you’d have a better chance of earning 20% returns or more in any given year than suffering an indexing loss. Pretty wild.

Source: A Wealth of Common Sense.

Shown another way as of early 2023:

Source: https://www.slickcharts.com

This implies younger investors, in my opinion, should at least consider going all-in on equities to take advantage of long-term stock market return power when they are younger given:

As you age, your human capital diminishes – your portfolio (beyond your home?) can become your greatest asset.

Younger investors can also benefit from asset accumulation from periodic price corrections – adding more assets in a bear market; allowing assets to further compound at lower prices when corrections or crashes occur (i.e., buying stocks on sale).

Back in March 2020 after stock markets had crashed, I expressed my disgust with the chorus of voices saying that this was the time to re-evaluate your risk tolerance. That advice was essentially telling people to sell stocks while they were low, which makes little sense. After the crash it was too late to re-evaluate your risk tolerance.

I suggested “we should record videos of ourselves saying how we feel after stocks crashed” and watch this video after the stock market recovers. Well, the stock market has long since recovered. Now is a great time to recall how you felt back in March 2020. Did you have any sleepless nights?

Now that markets are near record levels, it’s time to consider whether permanently lowering your allocation to stocks would be best for you in anticipation of future stock market crashes. Unfortunately, this isn’t how people tend to think. It’s while stock prices are low that they want to end the pain and sell, and it’s while stock prices are high that they feel most comfortable.

Michael J. Wiener runs the web site Michael James on Money, where he looks for the right answers to personal finance and investing questions. He’s retired from work as a “math guy in high tech” and has been running his website since 2007. He’s a former mutual fund investor, former stock picker, now index investor. This blog originally appeared on his site on Jan. 19, 2022 and is republished on the Hub with his permission.

By Ahmed Farooq, CFP, CIMA, Franklin Templeton Canada

(Sponsor Content)

ESG (environmental, governance and social) has become a hot topic in investment circles.

Sustainable investing is a key consideration for most asset managers nowadays, reflecting changing attitudes among investors.

Responsible or sustainable investing was once a very niche part of the market, but now accounts for US$35.3 trillion worldwide, according to recent data from The Global Sustainable Investment Alliance (GSIA).

This rise of ESG is most closely associated with equities, but this approach to investing can also be applied in the fixed income space too. Being able to minimize downside risk is a key objective for fixed income investors, and this certainly aligns with the characteristics of ESG investing.

Green Bonds evidence of ESG’s growing significance

ESG’s growing significance was displayed further earlier this year when the federal government’s 2021 budget included a plan to issue $5 billion in green bonds to support environmental infrastructure development in Canada.

Speaking at the recent Exchange Traded Forum, Brandywine Global Investment Specialist Katie Klingensmith discussed the firm’s investment philosophy and how ESG has become an important element of its strategies in recent years.

One of the specialist investment managers brought under the Franklin Templeton umbrella after its acquisition of Legg Mason in 2020, Brandywine Global has US$67 billion in assets under management globally.1

Of that total AUM, US$53 billion is in fixed income, where the investment team combines a global macro perspective with a disciplined value approach to select suitable holdings for the Brandywine funds.

A signatory of the UN-supported Principles for Responsible Investment (PRI) since 2016, approximately 99% of the firm’s assets under management now feature ESG integration.

Brandywine has built its own proprietary ESG portfolio management dashboard as a result, and will publish its first Annual Stewardship Report in 2021. Continue Reading…

Last month, I had the privilege of meeting legendary investor Larry Hite.

Larry was born into a lower middle-class family, had a major learning disability, did poorly in school, and was completely blind in one eye and half blind in the other. In his own words, “I was not handsome. I was not athletic. Whatever I did, I sucked at it badly.”

In 1981, after dabbling as a music promoter, actor, and screenwriter, Hite founded Mint Investments. Mint was a true pioneer, eschewing human judgment and instead basing its investment decisions on a purely systematic, rules-based approach rooted in statistical analysis.

By 1988, Mint registered average annual compounded returns of over 30%. In its best year, Mint registered a gain of 60% (1987, the year of the stock market crash), and in its worst year, it produced a gain of 13%. By 1990, Mint was the biggest hedge fund in the world, with a record-breaking $1 billion under management.

When it awarded Larry the Lifetime Achievement Award, Hedge Fund Magazine wrote:

“Larry Hite has dedicated the last 30 years of his life to the pursuit of robust statistical programs and systems capable of generating consistent, attractive risk/reward relationships across a broad spectrum of markets and environments and has inspired a generation of commodity trading advisers and systematic hedge fund managers.”

Although Hite began his investing career in the early 1980s, his philosophy of markets and approach to investing are remarkably similar to our own, which are summarized below.

Failure: A Foundation for Success

Hite maintains that his early failures were instrumental in his eventual success. He believes that accepting that failure is sometimes inevitable led him to develop an investment strategy that would limit losses.

In his book, The Rule, he wrote:

“I believe the success I’ve had arrived because I always expected to fail big. Solution? I engineered my actions so that a failure could not kill me. I won because I expected to lose. Failure became my advantage. Once you understand your potential for failure – that is, there are times you can’t win – you know when to fold your cards and move on to the next. You will do this more quickly than others who stay in the game too long, hanging on and hoping that their losing bet will turn around.”

It’s not all about Being Right

Many investors focus on being right as much as possible – on maximizing their ratio of winning vs. losing investments. On its face, this seems like a good idea – all else being equal, if you win more than 50% of the time, then over time you will make money.

Hite takes a different approach. Whereas he has no issue with trying to be right as often as possible, he is far more focused on maximizing the average magnitude of his winning positions relative to that of his unsuccessful ones, asserting that:

“Becoming wealthy and successful isn’t simply about being right all the time. It’s about how much you win when you are right as well as how much you lose when you are wrong…. The Mint trading system did not prioritize being right all the time. We prioritized not losing a lot when we lost but winning big when we won. But as a result, we were frequently wrong. We understood and expected this and taught our clients the wisdom too.”

Risk: A No Fooling Around game

Hite places a greater emphasis on risk management than on generating profits, claiming that mistakes regarding risk can lead to catastrophic results. He asserts that, “Risk is a no fooling around game; it does not allow for mistakes. If you do not manage the risk, eventually it will carry you out.”

His approach to investing clearly reflects his respect for risk. Specifically, Hite divulges that “We approach markets backwards. The first thing we ask is not what we can make, but how much we can lose. We play a defensive game.”

One of my favorite anecdotes regarding risk is Hite’s reflection on a conversation he had with one of the world’s largest coffee traders, who asked, “Larry, how can you know more about coffee than me? I am the largest trader in the world. I know where the boats are; I know the ministers.” Larry responded, “You are right. I don’t know anything about coffee. In fact, I don’t even drink it.” The coffee mogul then inquired, “How do you trade it then?”, to which Larry answered, “I just look at the risk.”

Five years later, Larry heard that this magnate lost $100 million in the coffee market. Upon reflection, Hite states, “You know something? He does know more about coffee than I do. But the point is, he didn’t look at the risk.”

Larry Hite

Market Predictions, Storytelling, & Good Copywriters

Larry is skeptical that anyone can predict markets. He in no way bases his approach to investing on making predictions, which he believes is an exercise in futility. In his own words:

“I respect the sheer intelligence and devotion of economists who have attempted to develop a unifying theory of market dynamics. But I don’t believe any such theory will hold up to scrutiny in the real world of money on the line. When you start believing you have remarkable market predicting powers, you get into trouble every single time.”

Hite is also critical of Wall Street research reports, claiming that they possess little investment value and are designed to exploit people’s natural tendencies to listen to entertaining narratives, stating:

“Stories began at the dawn of human society to entertain and instruct the next generation. We are wired to learn from well told stories. And unfortunately, Wall Street preys off our basic human weakness to want stories.”

In his typically blunt and straightforward manner, he adds, “When you start following slick reports filled with predictions, you’re just finding out who has good copywriters.”

A Computer can’t get up on the wrong side of the bed in the morning

Larry was a pioneer in his exclusive reliance on a data-driven, systematic approach, using statistical analysis of historical data to develop trading rules, which are the basis of his investment decisions. When he launched Mint Investments in 1981, his goal was “to create a scientific trading system that would remove human emotion from buying and selling decisions and rely instead on a purely statistical approach built on pre-set rules.” Continue Reading…

I must admit, the title of today’s post is a bit bogus. How so? Not to split hairs, but “volatility” is the variance above and below a long-term trend line. The thing is, nobody has ever asked me whether I can help them reduce their upside volatility. When equity markets are returning above-average returns, everyone’s happy.

So, I believe the actual question behind the question is how to reduce downside volatility. There are many kinds of investors, but I’ve never met anyone who enjoys seeing their investments go down, sometimes in a hurry.

From the behavioural side of things, it’s best to treat periods of downside volatility as bumps in the road, rather than turning them into permanent losses by bailing out when they occur. In that context, how do you best reduce investment volatility? There are at least two possibilities to explore.

1.) Reducing volatility through asset allocation

Understanding the role volatility plays in efficient markets circles us back to an investment strategy I’ve suggested all along: globally diversified asset allocation.

Instead of trying to manage volatility by trying to time markets or by selecting certain types of securities, I would suggest the better tool for the job – in fact the best one – is a healthy exposure to high-quality bonds. A bond allocation tempers your portfolio’s overall volatility. Once you have established that, you can then optimize your equity portfolio by tilting toward equity market factors with sources of higher expected returns (such as size, value and profitability).

2.) Reducing volatility by selecting low-volatility/low-beta stocks

Certainly, there are those who claim they can capture the returns of the broad equity markets while offering a smoother ride. The vast majority of these strategies fall into the categories of “low-volatility,” “equity minimum-risk” or “minimum variance.” They have been around for decades, and their popularity ebbs and flows with the market’s gyrations.

Gut feel would suggest that if you want to lower the volatility of your equities, it might make sense to focus on stocks that have exhibited lower volatility than the overall market (“low-beta stocks” in industry jargon). Perhaps yes, but the practical questions are whether these strategies (a) actually work, and (b) work better than asset allocation, as described above.

Before diving into the evidence, we’ve known for decades that market risks and expected rewards have been highly correlated around the world. In other words, lower risk/lower volatility stocks tend to be the same ones that deliver the lowest expected returns. So, just based on intuition, a “free lunch” of more market returns with less risk may not be so “free” or easy to obtain. It seems more likely lower volatility will simply lead to lower returns.

What the evidence tells us about low-volatility investing

Looking at an abundance of evidence, financial author Larry Swedroe has published several excellent, although highly technical articles about low-volatility/low-beta investing. In this one, he explains that researchers documented a “low-beta anomaly” decades ago. But he notes: Continue Reading…