“Many investors are wondering whether to pursue a TFSA or RRSP strategy. Quite simply, the TFSA, which started in 2009, compliments both the RRSP and RRIF.”

It need not be an either/or approach.

Wise investors embrace the Tax-free Savings Account (TFSA) in pursuit of long term goals, like retirement.

I summarize my 2017 TFSA primer:

1.) How TFSAs work

Eligibility:

• Canadian residents, age 18 or older, who have a Social Insurance Number can open a TFSA.

• One TFSA account per individual should suffice most cases. Be aware of plan fees if you own more than one.

Contributions:

• There is no deadline for making TFSA contributions as the unused contribution room is carried forward.

• A withdrawal in any calendar year increases the TFSA room in the following year.

• TFSA contributions can be made in cash or “in kind” based on the calendar year.

• Deemed disposition rules for “in kind” contributions are the same as those for RRSPs.

Over at MoneySense, my latest Retired Money column has been published, and it looks at the closely related topic of LIRAs (Locked-in Retirement Accounts, which have been termed “the RRSP’s less flexible cousin.” You can find the full column by clicking on this highlighted headline: Unlocking the Mystery of LIRAs.

In a nutshell, LIRAs are also known in some provinces as Locked-in RRSPs, which is exactly what they are. Unlike regular RRSPs, from which you can withdraw funds (and pay tax) if you need it at any time, LIRAs generally prohibit you from making any withdrawals before 55. Granted, when you’re younger that prohibition — illustrated above as a locked piggy bank — may seem frustrating but the idea is to protect our future retired selves from our current “tempted to spend it all” current selves.

As TriDelta Financial wealth advisor Matthew Ardrey told me, you’re going to see a lot more about LIRAs in the coming years. Whether you’re leaving a classic Defined Benefit pension plan or a more market-tied Defined Contribution pension plan, the job market these days is in such flux that a lot of people are going to have to start learning about what happens when you leave an employer pension plan earlier than you might once have envisaged.

LIRAs will multiply as Boomers reach Findependence

In the case of leaving an employer that provided you with a DB pension, you’ll be getting a lump sum based on the so-called “Commuted Value” of the pension at the time you leave (whether voluntarily or due to corporate layoffs or restructuring). I suggest that those who value the certainty of future DB pension payments plan eventually to annuitize such plans, likely the end of the year you turn 71. Continue Reading…

The TFSA and an expanded CPP means Millennials will depend less on RRSPs than the Boomers did

My contribution to the Financial Post’s first RRSP special report of the season can be found by clicking on this headline: For Boomers, the RRSP decision was easy but for Millennials, things are a little more complicated. The piece, which also appeared on page FP 10 of Wednesday’s print edition, recaps the three big advantages of RRSPs, articulated by regular Hub contributor Adrian Mastracci.

As baby boomers, both my wife and I have maximized contributions to our RRSPs almost from the moment we entered the workforce in the late ’70s (actually, in my case, only since 1984, when I rolled over a Defined Benefit pension into my first RRSP). And with no employer pension plan, my wife has continued to maximize her RRSP, to the point some of my sources tell me it’s time to stop, if we don’t wish to be subjected to onerous taxations and OAS clawbacks once we reach our 70s.

As for Millennials, the FP piece makes the argument that the Millennials enjoy two things the Boomers did not have for most of their investing careers: the Tax-free Savings Account (TFSAs, the Canadian equivalent of America’s Roth plans), and second, the newly expanded Canada Pension Plan or CPP.

As I noted in a Motley Fool special report in the fall, by the time the expanded CPP fully kicks in around the year 2065, someone who qualifies for maximum benefits and waits till 70 to receive them could get as much as $2,356 a month just from CPP, or $4,712 a month for a qualifying couple. Add in a giant untaxed TFSA and that might be all they’d need in retirement: assuming this high-saving couple maximized TFSA contributions at $5,500 a year (plus any inflation adjustments to come) from age 18 on.

To be sure, the eternal (well, eternal since TFSAs were introduced in 2009) question of TFSA, RRSP or both will depend on earning levels and tax brackets, which the FP article goes into in some depth. And it also bears mentioning that the TFSA advantage would be almost twice as compelling if the Liberal government had not acted to cut back on the $10,000 TFSA limit we enjoyed one year back to the current inflation-adjusted level of $5,500. So as it stands, high earners have roughly four times as much annual RRSP contribution room as they do for TFSAs, which is a pity.

My personal inclination is to maximize BOTH the RRSP and TFSAs, which certainly should be possible if you’ve eliminated all forms of consumer debt. Most dual-income couples should be able to do both, in my view, although of course if one of them is taking temporary stints outside the workforce (perhaps for child-raising), income-splitting practices like using spousal RRSPs may make sense.

Motley Fool blog on possible ban of trailer commissions

In the early part of the New Year we see, hear, and read a lot of messages regarding Registered Retirement Savings Plans (RRSPs). From every indication, they are important to have as a saving tool as we get older.

RRSP and Containers

Before getting to why it is important, a quick overview of the RRSP concept. The best way I can explain the concept of a Registered Retirement Savings Plan or RRSP, is that it is essentially a container. It can be a jar, a glass, a bathtub, anything that can hold something.

In terms of RRSP containers, I’ll keep this simple. You have several types to choose from:

Asset Specific RRSPs –can only hold a specific type of asset like a GIC or a mutual fund. You can hold multiple containers of Asset Specific RRSPs

Self-Directed RRSPs –can hold a variety of securities including individual stocks, bonds, ETFs, mutual funds, cash, GICs, Treasury Bills. They are much more flexible in terms of your options of what you want to put in your container. The banks and brokerages usually charge an annual fee for the privilege of using their containers, however if you have enough assets to put into the container or throw a lot of business there way, you can get it waived.

TFSA vs. RRSP is one of the most common questions I am asked. If you want to know for sure which is better for you, then you need a financial plan.

Many articles have been written on this topic that list pros and cons with general opinions.

The truth is that:

1.) Rather than just having an opinion, there is a precise right answer specifically for you. To the extent that you know your present and future marginal tax brackets, you can calculate a precise optimal contribution for RRSP and TFSA for each year, as well as the optimal amounts to withdraw each year after you retire.

2.) The decisive factor is your tax brackets now vs. after you retire. Most people just assume they will be in a lower tax bracket after they retire, because their income will be lower. In many cases, that is not true.

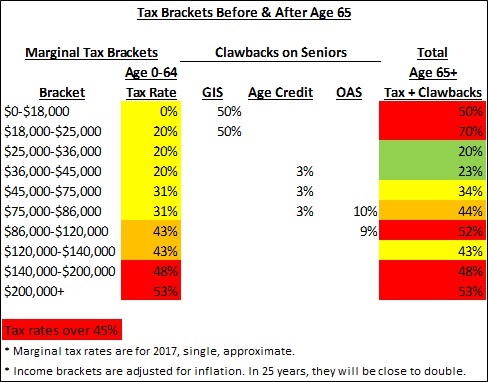

When you include the clawbacks of government income programs that affect everyone over 65, many seniors are in shockingly high tax brackets!

The clawbacks cost you actual money and are the same as a tax. The three main clawbacks are the 50% clawback on GIS for low incomes (under $20,000), 15% clawback on the age credit for middle incomes ($35,000-85,000), and the 15% clawback on OAS for higher incomes ($75,000-120,000).

The chart above shows the actual approximate tax brackets before and after age 65. Check out the tax brackets over 45% in red:

Understand the differences

You can own the same investments in your TFSA as your RRSP. The main difference is that RRSP contributions and withdrawals have tax consequences, while TFSA contributions and withdrawals don’t.

Therefore, the answer to TFSA vs. RRSP is primarily based on your marginal tax bracket today compared to when you withdraw after you retire: Continue Reading…

“Many investors are wondering whether to pursue a TFSA or RRSP strategy. Quite simply, the TFSA, which started in 2009, compliments both the RRSP and RRIF.”

“Many investors are wondering whether to pursue a TFSA or RRSP strategy. Quite simply, the TFSA, which started in 2009, compliments both the RRSP and RRIF.”