Today’s economic and job-growth landscape might have you turning to investing as a prominent option.

It takes patience and effort, but anyone can save up enough through intelligent investments.

How do you begin the Investment Process?

As of 2023, the average American makes around US$57,000 annually, which is lower for minority groups. Even if you’re careful with your spending, becoming financially independent with that salary can take a long time.

The average person from the United States only has about $5,000 in savings. Before beginning the process, you must consider how much money you can invest. The ultimate goal is financial independence [aka “Findependence” on this site], but getting there can take a while. Only put in what you’re willing to lose because things might not pan out as expected.

The formula for Findependence takes your yearly spending and divides it by your safe withdrawal rate to calculate your goal savings figure. Then, it subtracts the amount you’ve already saved and divides that amount by how much you can save each year. It’s only an estimation, but it can help you know how much your investments need to make.

What Investments should you Consider?

There are plenty of investment types. The stable ones often have lower returns and you usually need to take some risk to see a high reward quickly.

1.) Real Estate Investment Trust

A real estate investment trust (REIT) receives money from investors to purchase and manage property. Most generate revenue through rental income and pay dividends in return for the initial payment you made. It’s similar to owning by yourself, but you pool funds for the purchase and let someone else take care of the tenants. There are also other REIT types, so you have more options than rental properties.

2.) Stocks

The stock market usually requires more attention to detail because you must keep up with it. Anything from an upcoming brand deal to an overseas political event can affect this investment type. You should frequently check the stocks you hold and the businesses they belong to so you can quickly respond to changes.

The Canadian stock market differs from the United States version. Firstly, you need a brokerage account. Most brokerages charge about $5 to $10 per trade, with average commission fees of $6.95. It might seem minor, but paying to invest or shift your stocks around puts you at a loss before you begin. The flat rate cut you must pay can also make investing smaller amounts challenging because it takes a higher percentage the less you put in. Continue Reading…

BDO Affordability Index Spring 2023 (CNW Group/BDO Canada LLC)

By Jennifer McCracken, BDO

Special to Financial Independence Hub

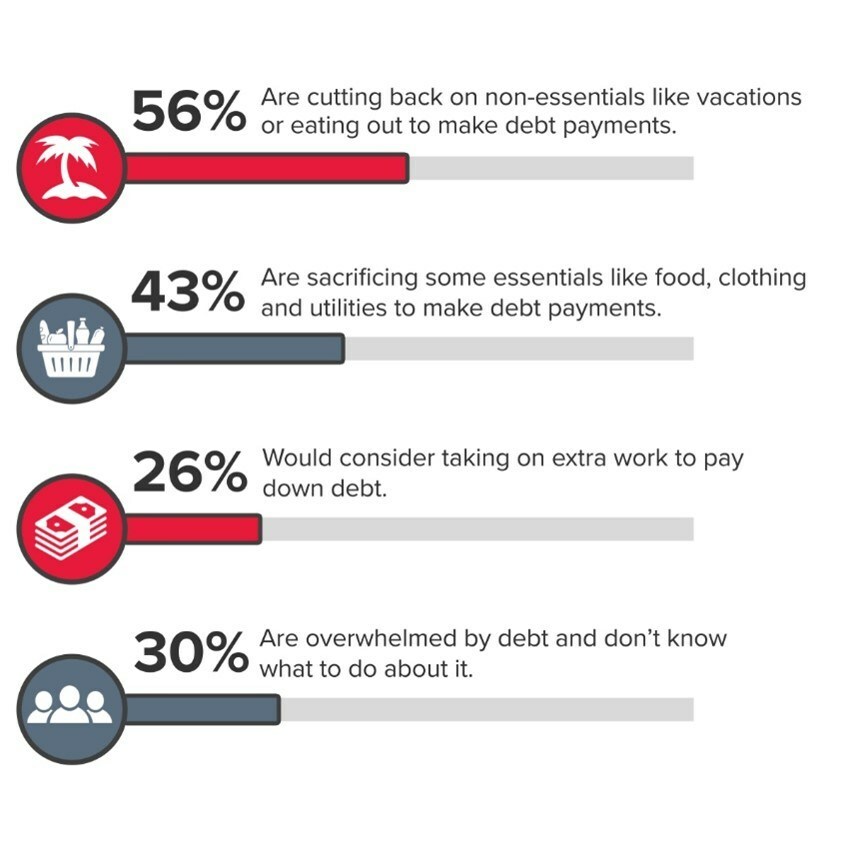

The cost of living has spiked significantly in the past year and Canadians across the country are feeling the pinch. Younger Canadians between the ages of 18 and 34 are particularly affected, having not had the chance to build up as much savings as older generations.

BDO’s newest Affordability Index shows that 45% of young Canadians say their debt load is overwhelming and they’re unsure how to tackle the problem. That’s higher than those between the ages of 35 to 54, where 39% say they’re in that situation and significantly larger than the 13% of Canadians between the ages of 55+ who feel the same.

Credit-card debt appears to be the main reason younger Millennials and Gen Z are falling behind, with 37% of 18-34 year olds saying this form of debt causes them the most stress. Mortgage debt and student debt were the next closest reasons, with 22% for the former and 21% the latter.

What are Canadians doing to cope with inflation and rising debt?

It’s not surprising then that 49% of younger Canadians say they’re reducing their living expenses to cope with inflation and the high cost of living, while 32% say they’re lowering how much they contribute to savings as well.

While younger Canadians may be struggling more than their older counterparts, they’re also more open minded when it comes to finding solutions.

The Affordability Index indicates that younger generations are much more willing to look for new streams of revenue compared to older ones. Some 24% say they are adding part-time work to keep up with inflation, compared to just 13% of 35-54-year-olds and only 5% of those 55 or older.

Young Millennials and Gen Z would also find side hustles and gig work to increase their income. Of those doing this, 35% said it was to help them pay for essentials and 27% say it’s to help them pay down debt.

It’s not just part-time and gig work that younger Canadians are using to fight inflation, they’re also looking for higher paying jobs. A total of 13% say they’ve recently found a new full-time job in response to the affordability crisis. That’s compared to just 7% of those aged between 35-54 and only 1% of those 55 and older.

However, while younger generations are keen to seek out new ways to increase their income, they’re very unfamiliar with many of the most common debt relief options available.

A lot of people just don’t know what their debt relief options are …

Only 19% of them said they were familiar with the idea of bankruptcy, 11% said they know what a debt management plan is and 9% with a debt consolidation loan. Continue Reading…

To help you create a budget and stick to it for achieving your financial goals, we’ve gathered advice from 18 professionals, including CEOs, founders, and VPs. From leveraging public accountability to reviewing and adjusting your budget regularly, these experts share their top steps to take for effective budgeting and saving.

Leverage Public Accountability

Negotiate Lower Fees

Celebrate Budgeting Successes

Automate Your Savings

Identify Cost-Cutting Opportunities

Track Expenses and Income

Eliminate Unnecessary Expenses

Create a Realistic Budget

Prioritize Necessary Expenses

Monitor Financial Metrics

Automate Savings Consistently

Use the 50/30/20 Rule

Utilize a Monthly Bill Calendar

Limit Online Shopping Access

Establish a Purpose and Set Goals

Use Cash Stuffing With Discipline

Create Organized Sub-Budgets

Review and Adjust the Budget Regularly

Leverage Public Accountability

In my personal journey toward financial wellness, one of the most effective strategies I’ve employed is leveraging public accountability to create a budget and stick to it. I started by sharing my financial goals with my circle of trusted friends and family, which made the goals feel more real and tangible.

Whenever I felt tempted to stray from my budget, the thought of explaining my overspending to them motivated me to resist. In fact, one time I was really close to buying an expensive gadget on a whim, but the idea of having to admit this unnecessary expense to my accountability partners made me rethink, and I decided against it.

Using public accountability in this way can be a powerful tool to reinforce your commitment to your financial goals, and I encourage you to try it. — Antreas Koutis, Administrative Manager, Financer

Negotiate Lower Fees

One example of a strategy not commonly undertaken when creating a budget is to negotiate lower fees on existing bills such as cable, internet, or cell phone plans.

As the market becomes increasingly competitive, companies are more likely than ever before to reduce customer bills if they know they may otherwise lose that customer’s business.

This can lead to significant savings without having to decrease spending on existing items. With the resulting saved money, you can then allocate it towards your financial goals, more easily allowing for what was once considered unattainable! — Carly Hill, Operations Manager, Virtual Holiday Party

Celebrate Budgeting Successes

Creating a budget and sticking to it, in my opinion, is difficult work. Celebrate your accomplishments along the way. In the long run, I believe that this will make it easier for you to stay on your budget and will help keep you motivated.

Treat yourself to a small reward if you reach a savings goal or pay off a debt, for example. Just make sure the prize is within your financial constraints! — Bruce Mohr, Vice-President, Fair Credit

Automate your Savings

A lot of people tell you to pay yourself first. I think a better approach is to save for yourself first. Set up automatic transfers to your various retirement and savings accounts. That way, the money isn’t just sitting in your checking account and tempting you.

This works even better when you have high-yield savings accounts and retirement funds that aren’t linked to your main bank account. Spending habits are hard to break, but it can be easier to form new ones if you automate your savings. — Temmo Kinoshita, Co-founder, Lindenwood Marketing

Identify Cost-Cutting Opportunities

Of course, the goal of budgeting is to save money, but one step you need to take in order to be successful and reach your financial goals is to look for ways to save. You can do this by reviewing your budget and pinpointing areas where you can cut costs to save money.

For example, if you find that you spend a lot of money on going out to eat, you can cut down spending here and instead cook your meals, which ultimately will be the cheaper alternative.

You may also cancel subscriptions you don’t use or negotiate your bills with your service providers to see if you can get a discount. Overall, there are multiple ways to cut down your spending and save money—you just need to figure out which areas you can negotiate or compromise! — Bill Lyons, CEO, Griffin Funding

Track Expenses and Income

You can find areas where you might be overspending or where you can reduce expenditures by keeping track of your expenses and income. Additionally, you may utilize this data to make wise decisions on future purchases and investments, ensuring that you are deploying your resources as effectively and efficiently as you can.

You may keep yourself motivated and on track to accomplish your goals by routinely evaluating your financial accounts and your progress toward them. Additionally, it can assist you in seeing future difficulties or obstacles, enabling you to modify your plan and change the route as necessary. — Michael Lees, Chief Marketing Officer, EZLease

Eliminate Unnecessary Expenses

A major problem people have when sticking to a budget is the little purchases they make along the way. Many of us are guilty of ordering takeout after a long day of work, picking up a daily Starbucks order, or wasting groceries.

While these small purchases may seem innocent enough, they quickly add up and get you off track toward reaching your financial goals. Before making a purchase, ask yourself, do I need this? Or if you need extra motivation, consider how many hours of work it takes you to purchase these daily items.

By cutting out or at least reducing some of these mundane purchases, you’ll notice your bank account feeling a little healthier and lower stress knowing you have enough money to put towards your financial goals and still pay your bills. — Brandon Brown, CEO, GRIN

Create a Realistic Budget

Often, I see people attempting to budget just for the sake of budgeting without considering its implications on their overall lifestyle. If you want to religiously follow your budget, make it realistic. Realistic financial goals will provide you with a head start in creating an achievable and sustainable budget.

Create a budget that takes into account not only your financial goals but also your lifestyle behavior and the situation you are in right now. If you regularly eat out, set aside money for that based on how much you anticipate spending and how much you are willing to spend.

Moreover, don’t make your spending plan too strict. What’s the purpose of working if you can’t occasionally treat yourself to a sumptuous meal or a new pair of boots? After all, you deserve to feel human.

If you don’t make room for the things you want, you’ll eventually give in and ruin your spending plan. Just make sure to plan ahead and remember that the ultimate goal is financial security and independence. — Jonathan Merry, Founder, Moneyzine

Prioritize Necessary Expenses

Pay all your bills before buying anything discretionary. When you’re trying to save money, it’s essential to cover all necessary expenses before you try setting money aside. This way, you have a better idea of how much money you have left for casual spending and savings.

Paying any obligations first allows you to avoid surprise expenses after you’ve already started spending, which in turn helps you avoid having to pull money out of your savings. The best way to stick to your budget is to pay what you need to first. — Max Ade, CEO, Pickleheads

Monitor Financial Metrics

Entrepreneurs should track financial metrics to monitor their success. A metric for entrepreneurs to measure is customer lifetime value, which is the total amount of revenue that one customer generates during their entire interactions with the business.

Monitoring this metric helps entrepreneurs understand how much revenue can be expected from a single customer and what marketing strategies are most effective at keeping them engaged.

Additionally, tracking customer lifetime value allows entrepreneurs to maximize their returns on investment as they can target customers who spend more money and reward existing customers who have already demonstrated loyalty and commitment. — Julia Kelly, Managing Partner, Rigits

Automate Savings Consistently

Automating savings is a surefire way to help you stick to saving money and reaching your financial goals. Too many situations can thwart your best intentions to regularly add to your savings yourself: mainly forgetfulness since an additional task is the last thing anyone needs.

If you don’t automate, you may rationalize not regularly adding to your savings account because of an extra purchase you think you need or deserve. That could snowball into a pattern of doing it less than you initially wanted or not at all.

“Out of sight, out of mind” is an advantage of automating your savings: If you don’t see that money sitting in your checking account, you won’t spend it.

Disabuse yourself of the notion that you need a large amount of money for an automatic savings plan. Start with $5, $10, or $20 at a time. You can increase that by looking for ways to decrease your expenses, such as comparison shopping for your car and home insurance or requesting lower interest rates on credit cards. — Michelle Robbins, Licensed Insurance Agent, Clearsurance.com

Use the 50/30/20 Rule

To create a budget and stick to it, prioritize your expenses and allocate your income with the 50/30/20 rule. This rule suggests that 50% of your income should go towards necessities like rent, utilities, and groceries, 30% should go towards discretionary spending such as dining out and entertainment, and 20% should go towards saving and paying off debt. Continue Reading…

As a mother, I know the importance of raising my daughter to be independent and confident. One of the most significant ways I can do this is by instilling in her the value of financial literacy. By teaching her to be financially independent, I am setting her up for a future where she can make sound decisions with money and have the freedom to achieve her dreams. I feel every mother should share this responsibility and nurture the financial skills of their children, especially when we consider the uncertainties of the current global economic climate.

Growing up and learning to manage money through lived experiences, I discovered that some of those life lessons can be painful. My immigrant parents were so focused on working hard to provide the basics for the family, financial literacy lessons weren’t really a priority for my sister and me. All we were taught was to save and keep on saving. In fact, my sister and I would sometimes skip lunch at school just to save the allowance our parents gave us. I learned the hard way that while saving is part of being financially literate, it can’t just stop there; a significant next step is to find safe, reliable methods to growing your wealth.

Not knowing better, when I was 18, one of the earliest financial mistakes I made was getting multiple credit cards, which eventually resulted in a lot of debt (because which teenage girl doesn’t like shopping?). I had to work hard to pay it off and it was a tough lesson to learn, but it was valuable because it made me realize the importance of being smart about money from a young age.

After that, I started seeking support to become more financially literate from any source I could get my hands on. The internet was my best friend and I got into the habit of listening to podcasts about investing and best financial practices. When I started working, I was lucky enough to find a trusted mentor who taught me that putting 75 per cent of my paycheque toward smart investments was smarter than spending the money on any big-ticket item immediately.

As I became better with money, I went from only knowing how to save money to growing my wealth through investing in stocks (ETFs) and real estate and having a diverse portfolio. When it comes to investments, I now know it’s important to maintain both passive and aggressive investments. Having said that, choosing between good investments and bad ones can be daunting and that’s where financial advisors come in. Engaging a trusted advisor who is experienced in investing in different asset classes can make all the difference in the world because they often have access to wealth management tools and data that make investment proposals more reliable and easier to understand.

Teaching children about saving and investing — and the mindset behind both

Although I eventually found my financial footing, others are not so lucky and many have never been able to recover once they get into debt, which can be crippling. Now that I have a family of my own, one of my top priorities is to make sure my daughter has a strong foundation in financial literacy, with all the tools she needs to make better decisions when managing money.

One of the things that we’ve started working on together is to get her to save regularly, like I did as a child. But more than teaching my daughter good saving habits, I believe what’s important is to show her the difference between the money-going-out and money-going-in concept. Very often, children are no strangers to the former because they see us making purchases daily and this makes it easy for them to learn spending (or worse, impulse spending). The latter, however, is more difficult to emulate because they rarely witness the act of saving. This is especially true now that we live in a world where most financial transactions are digital. Though this speaks to the convenience of innovation, how do we curb impulse spending in our children beyond merely saying “no” (and parents, I’m sure you’ll agree that saying “no” doesn’t always elicit the best response from children)? Continue Reading…

From opening two different savings accounts to giving your money a job, here are 12 answers to the question, “Give your best tip for how to balance the need to save and invest for the future with the desire to enjoy my life and spend money on things that are important to you?”

Open Two Different Savings Accounts

Consider Your Housing Costs

Focus on The Three Aspects of Great Personal Finances

Use Financial Aggregators to Monitor Spending

Spend Money On Your Passions; Avoid Pointless Purchases

Invest in Things That Will Last

Understand Your Cash Flow

Consider the 50-50 Rule

Create and Follow a Budget

Use Fixed Percentages for Saving /Investing

Schedule a ‘Spending Period’ in Your Life

Give Your Money a Job So It Has a Purpose

Open two different Savings Accounts

Most people have a checking account and a savings account. If you want to save for the future, open up a second savings account and put your long-term savings in that pot. Find the best interest opportunities you can find for that account and leave that money alone to the best of your ability.

For the money that you want to use in the shorter term (shopping, traveling, buying gifts), manage that money in a separate savings account. Your checking account should cover all of your expenses while your primary savings account should be your “fun-spending” money.

The third account should be your long-term savings and that should be the money that you take to your financial advisor for the best long-term investment opportunities. Let that build up for a while and then try to make smart investments with it. — Brittany Dolin, Co-founder, Pocketbook Agency

Consider your Housing Costs

If you’re struggling to save and invest for the future while also enjoying life, consider your housing costs. Housing is one of the biggest monthly expenses, so if you’re living in a home that’s too big for you, or you’re paying more than you can afford for it, you may want to consider downsizing.

Consider your needs and wants when choosing a home. Do you really need a five-bedroom home if you’re a family of two? Can you live somewhere with fewer amenities if it means you can save money on your monthly housing costs? Homeownership is an investment in yourself and your future, so it’s important to find a balance between spending on your housing and investing in the future. — Matthew Ramirez, CEO, Rephrasely

Focus on the three Aspects of Great Personal Finances

I’ve learned from my mentors that great personal finances can be broken down into three areas: Budgeting Expenses, Creating Income, and Developing Cashflow-Producing Assets.

With any money-related goal, identifying which area(s) to focus on is key. For example, getting out of debt requires stricter budgeting and increasing income. Meanwhile, retirement has to do with areas 1 and 3. This also makes it simple: budget a percentage of your income to save and invest based on your long-term goals.

Then determine your priorities. Perhaps you need to be strict with some other living expenses to be able to spend money on what’s important to you and set savings and investment goals for larger purchases while you also work to increase your income. — Eric Chow, Chief Consultant, Mashman Ventures

Use Financial Aggregators to Monitor Spending

The balance between saving and investing for the future, while also enjoying life and spending money on what matters to you, is a difficult one to achieve.

One uncommon way to reach this balance is by using financial aggregators. Financial aggregators are tools that allow you to connect all your accounts, such as investments and bank accounts, into one place in order to get a better look at where your hard-earned money is going. This makes it easier for you to budget wisely and allocate money towards satisfying both savings goals, as well as needs or wants for immediate enjoyment.

With this knowledge in hand, you’ll be more aware of how much flexibility you can have with your monthly expenses since both needs are being fulfilled simultaneously. — Carly Hill, Operations Manager, VirtualHolidayParty.com

Spend Money on your Passions; Avoid Pointless Purchases

The best way to save money and enjoy life is to spend money on your passions and cut back on everything else. For example, you might grab a Starbucks drink before work every day. But does this really add value to your life? You can make the exact same coffee at home for a fraction of the price. This is just one example, but most people are spending thousands of dollars a year on unimportant things.

Once you’ve cut expenses out of your life that don’t provide value, spend this extra money on your passions. Let’s say you’re a big fan of motorbiking. You can use this money to buy a sport bike and go to your local racetrack every weekend. Or, if you love hiking, buy quality hiking gear and hike with friends and family. This strategy allows you to cut back on unimportant expenses, save money, and spend more on things that bring happiness. — Scott Lieberman, Owner, Touchdown Money

Invest in Things that will Last

A great way to balance the need to save and invest for your future while still enjoying life is mindful spending. This means considering each purchase you make, big or small, and evaluating if it will add long-term value and benefit you; an uncommon example of this would be investing in a massage package.

Instead of splurging on something that won’t provide sustainable value, such as multiple nights out with friends, consider treating yourself to regular professional massages — which have medical benefits from managing pain to reducing stress — that promote mental health and well-being. Practicing mindful spending ensures money is not wasted frivolously but also allows for some indulgences now that can later prove beneficial. — Grace He, People and Culture Director, teambuilding.com

Understand your Cash Flow

Understanding your household cash flow is among the most important aspects of securing your financial future. In order to have more money to spend or save now, you must be acutely aware of your spending habits. Continue Reading…