It does not matter if you have $1,000 or $100,000 in your account: you probably want to make the most of the cash you have. But how, exactly, is this accomplished?

There are many strategies. The Financial Independence Hub details some of the easiest and most effective below.

Get Help

If money management is your weakest link, look for an accountant or financial consultant to help you get a better grip on your financial future. You can find experienced financial professionals through different online job boards and platforms.

Manage your Debt

There is nothing wrong with having a house or car payment. These are debts that most people expect to take on. However, credit-card debt is something that eats away at your bank account more than you might imagine. According to Business Insider, average credit card interest rates in 2020 are more than 15 per cent. And these only compound, meaning that you pay interest on interest accrued each month as your balance continues to rise. Look at it this way: For every $100 you are in debt each month, you pay an extra $15. To keep more of your money, eliminate debt as soon as possible. Pay down your lowest balances first and then add that payment each month to your high-balance cards.

Check your Bank Accounts

When it comes to bank accounts, there are two primary types of accounts you might think about: chequing and savings. What you may not realize is that each of these has different subcategories, and some pay higher interest rates than others, and you may only be getting a small interest payment each month. Consider switching to a money market, which has a higher interest rate. Continue Reading…

Cash is king during times of economic trouble. Working families need emergency savings to pay the bills in case of job loss or a reduction in wages. Retirees or near retirees need a cash cushion to avoid selling stocks at a loss. But should you park your cash in a high interest savings account or a GIC?

For a short time, not too long ago, we lived in the golden age of high interest savings. The competition was lively, as online banks and credit unions pushed interest rates well above 2 per cent (LBC Digital briefly paid 3.3 per cent).

Rising interest rates on savings deposits made GICs look less attractive. GICs paid the same rates or lower, yet savers had to lock-in their deposits for 1-5 years. Where did the liquidity premium go?

High Interest Savings Account rates

The situation quickly changed when the coronavirus pandemic forced central banks to take emergency action and cut interest rates. The Bank of Canada lowered its key interest rates by 50 basis points on two occasions. The ripple effect caused high interest savings account rates to plummet.

LBC Digital had already lowered its rate to 2.8 per cent – now it sits at a still respectable 2.25 per cent. Wealthsimple Cash had arguably the worst-timed launch when it came out with a 2.4 per cent interest rate for its chequing/savings account hybrid. That rate was quickly dropped to 1.9 per cent, and then lowered again to 1.4 per cent.

EQ Bank lowered the interest rate on its Savings Plus account to 2 per cent, while motusbank dropped its rate to 1.75 per cent. What a difference a month makes!

Here are the top high interest savings account rates today (March 25, 2020):

Bank

Interest rate

LBC Digital

2.25%

Motive Financial

2.20%

Implicity Financial

2.10%

Outlook Financial

2.10%

EQ Bank

2.00%

Oaken Financial

2.00%

As always, savers need to look beyond the big banks to maximize the interest earned on their deposits. If inflation averages 2 per cent, then you need to earn at least 2 per cent on your savings to maintain purchasing power. Even still, at best you’re treading water.

Despite the recent drop in rates, a high interest savings account is still the best place to park your emergency savings. You never know when you’ll need to access cash for an unexpected bill, or to pay for your living expenses during a period of unemployment.

A high interest savings account is also a must-have for retirees and near-retirees to stash one year’s worth of spending – the first bucket in the three-bucket approach to retirement income planning.

What this current rate crisis has highlighted is the fact that high interest savings account rates are not guaranteed. Those who eschewed GICs to chase higher yielding savings accounts now find their savings account paying 0.50 – 1.00 per cent less than it was a month ago. Not ideal.

GIC rates

One of my clients recently alerted me to an email sent by Oaken Financial advertising an increase in GIC rates. Its one-year GIC now pays 2.5 per cent, which is a full 25 basis points more than the top-paying high interest savings account. Oaken’s five-year GIC now pays 2.95 per cent interest. It looks like the liquidity premium is back.

You’ll easily find one-year GIC rates paying at or above the best high interest savings account rate.

Bank

Interest rate

Oaken Financial

2.50%

Canadian Tire Bank

2.50%

EQ Bank

2.40%

Wealth One Bank of Canada

2.40%

Peoples Trust

2.30%

Longer-term rates vary widely so be sure to shop around for promotions. Here are the top five-year GIC rates as of this writing:

Bank

Interest rate

Oaken Financial

2.95%

Wealth One Bank of Canada

2.60%

Canadian Tire Bank

2.55%

EQ Bank

2.55%

Peoples Trust

2.55%

Readers should know that GICs are typically non-redeemable, so you should be absolutely certain that you won’t need the money when you lock it in for 1-5 years.

That means GICs are ill-suited for an emergency fund, but ideal for a goal with a specific time period.

Using High Interest Savings Accounts and GICs for Retirement Income

For retirees and near-retirees, GICs are best-suited for “bucket two” in your three-bucket approach to retirement income. Bucket two is where you build a GIC ladder with three to five years of annual retirement spending. Continue Reading…

Saving can be one of the most time-consuming methods of acquiring personal wealth, but if you choose the right account for the right goal, you can make the most out of this lengthy process.

The best way to make your money work over time is by choosing the best savings account based on what you’re saving for.

Picking the best savings account in Canada can maximize your interest return and (in some cases) minimize the amount of taxes you’ll end up having to pay.

While this might seem obvious, it’s a crucial step in the financial planning process. By finding the best savings accounts based on what you’re saving for, you’ll be able to achieve your financial goals much more quickly.

The other side of the coin shows that not choosing the right account can cause roadblocks down the line and sometimes cost you money in early withdrawal fees and taxes.

For example, if your aim is saving on a down payment for your first house, but you have all of your money wrapped up in, let’s say, GICs, you won’t be able to withdraw funds early without a penalty.

But that’s not to say that savings accounts are only propped up for massive investments like homes or your retirement.

Saving up for a car, your wedding, or even a trip can have significant benefits on your interest return, but only if you pick the best savings accounts for your financial goals.

Base choice of Savings Account on what you’re saving for

If you’re unsure what it is you need to save for, consider these two questions before making any firm decisions:

What is my financial situation like right now?

Will I need to access the money I’m investing soon?

Here are a few suggestions why a TFSA, RRSP, and HISA are best suited for your short-term and long-term goals, whatever they may be.

Tax-Free Savings Account (TFSA)

A Tax-Free Savings Account (TFSA) isn’t exactly a savings account. Think of TFSAs as tax shelters. You can put cash, mutual funds, stocks, bonds, or GICs in a TFSA and shelter them from taxes, as long as you remain under your yearly TFSA contribution limit [currently $6,000.]

The contribution limit on your TFSAs depends on how much you contribute each year and the yearly contribution limit allotted by the Canadian Revenue Agency (CRA).

If you exceed your yearly TFSA contribution limit by $2,000, you will not be able to deduct the exceeded amount. Contributions that exceed the $2,000 threshold are subject to a 1% fee for every month the amount remains in your RRSPs.

A Registered Retirement Savings Plan (RRSP) might seem like a savings account exclusively for retirement planning. However, it’s also one of the best savings accounts for saving for your first home.

An RRSP is somewhat similar to a TFSA. Both shelter your contributions from tax: so long as you remain below your yearly contribution limit. Unlike a TFSA, however, an RRSP does not allow you to withdraw money tax-free. Continue Reading…

Canadians have few reasons to save these days. Cheap borrowing coupled with feeble returns on your savings deposits makes it hardly seem worthwhile to park your cash in a savings account. Some banks have decided to punish savers even further by charging fees just for moving your money around.

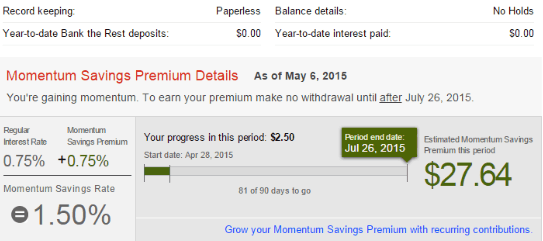

Gaining Momentum Through Inertia

But one bank has turned to the carrot rather than the stick approach to help its customers save. Scotiabank, which already boasts the best suite of rewards credit cards, in addition to its Moneyback chequing account, has raised the stakes with a new high-interest savings product called the Momentum Savings Account. Here’s how it works:

Using a unique incentive that rewards “inaction”, or our tendency to drift toward financial inertia, the Scotiabank Momentum Savings Account pays a bonus interest rate for customers who do not make a withdrawal in a 90-day period.

The account pays regular interest of 0.75 percent when you keep a balance of $5,000 or more. If you resist the temptation to withdraw from your account for 90-days, you’ll receive a 0.75 percent bonus, for a total interest rate of 1.5 percent.

Customers who open an account by June 15th, 2015 will get an additional 0.5 percent bonus, for a total of up to 2 percent until July 31st, 2015.

Momentum Savings also comes with an “Account Tracker” that customers can access online and through their mobile app. It provides a visual “countdown” to the extra interest payment, so you can see when you’ll receive the extra interest. With this tool, you can be strategic about when to withdraw from the account to ensure maximum savings.