Personal savings are just that: personal. How much, why and how you save your money should be tailored to you and your personal goals and financial circumstances.

However, many Canadians feel uncertain when it comes to how to invest their money. In fact, a new survey from TD finds many Canadians have mixed views when it comes to the choosing the best method to save for the future. While over half of Canadians surveyed (59 per cent) agree that TFSAs and RRSPs are a crucial part of their savings strategy, one in four (27 per cent) admit they don’t know the differences between the two – whether that’s the contribution limits, withdrawal considerations or impact on taxable income.

If you’re thinking of starting to save – or want to improve your current savings plan – you may want to consider an RRSP, a TFSA, or a combination of the two. Both are great tools for saving that can be used separately or together. But how you use them depends on why you’re saving money, and when and how you want to access it.

For example, if your goal is short-term, like a new vehicle or a home renovation, a TFSA will allow you to grow your money tax-free and you can access it at anytime without penalty. If your goals are long-term, like retirement, an RRSP may be the way to go. People often think that they need to pick one over the other, but that’s not the case. Most people have both short- and long-term goals, so a mix of both TFSAs and RRSPs is often the best choice.

Whether you’re planning for long-term retirement or for a goal in the near term, the important thing is to save your money where it’s going to work best for you. Financial planning doesn’t have to be intimidating and there’s no one size fits all approach when it comes to saving for your future. A financial advisor can work with you to develop a personalized plan that aligns with your time horizon, risk tolerance and personal goals, and will help you feel confident that you’re choosing the best option for your future.

Background info: Survey findings are based on an Ipsos poll conducted between December 17 and 19, 2019, on behalf of TD. A representative sample of 1,500 Canadians aged 18 and over were interviewed online. The poll is accurate to within ±2.9 percentage points.

Jennifer Diplock is Associate Vice-president, Personal Savings and Investing, TD Bank Group, based in Toronto.

The registered retirement savings plan (RRSP) contribution deadline is today!

Many Canadians may be making last-minute contributions before the deadline of midnight March 2nd in hopes of unlocking a bigger tax return [if investing online; if at a physical branch, you need to act during business hours — editor.]

In fact, a recent survey from H&R Block reveals that 32 per cent of Canadians plan to contribute to an RRSP this year, a six per cent increase from last year where only 26 per cent of Canadians reported their intentions to contribute.

While RRSPs can offer tax advantages to help you reach your savings goals, it’s also important to note that they aren’t the only option available.

RRSPs vs. TFSAs

While RRSPs – a tax-deferred retirement savings vehicle in which contributions are tax deductible – can be a great investment, you do have to pay income taxes when you withdraw money, which makes this option a bit less flexible should a sudden need to access your funds arise.

Another investment tool to consider is the tax-free savings account (TFSA). Because TFSA contributions are made from after-tax income, the TFSA is a simpler tool in that it allows your investments to grow tax-free. And, since taking money out of it has no tax consequences, it can be much more flexible.

How to decide between these two investment options

The main differences between the RRSP and TFSA are their contribution limits, withdrawal restrictions, and how and when you pay taxes. Both are investment vehicles that can shelter taxes on your investments, but depending on your circumstances, one might suit you better than the other. Continue Reading…

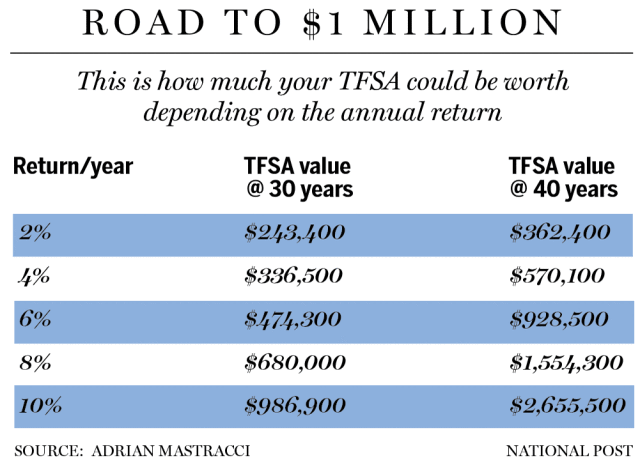

My latest Financial Post column looks at how Millennials and other young people can create a million-dollar retirement fund if they start contributing $6,000 to a Tax-free Savings Account (TFSA) the moment they turn 18. You can find the full column online by clicking on the highlighted text: The Road to the million-dollar TFSA is getting shorter for Millennials. It’s also in the print edition of Wed., Feb. 26th, under the headline “The road to saving $1 m for millennials: TFSA likely the best way to start.” (page FP3).

I’ve always been enthusiastic about the TFSA since it was first possible to contribute money to them in January 2009. My wife and I, as well as our daughter till recently have contributed the maximum to them from the get-go, always early in January to maximize the power of tax-free compounding. All three accounts have done very well. (I won’t reveal the balances but they’re consistent with heavy equity exposure through most of the bull market we appear to have been in at least until this week.)

Suffice it to say that our daughter’s TFSA has done better than ours, despite her not having contributed in the last two years because she has been working out of the country. She insisted in owning most of the FANG stocks (including Apple) and even Tesla, which was underwater until very recently but began to make headway in recent months.

It’s purely by chance that having been born in 1991, our daughter became 18 just in time for her first TFSA contribution, which naturally we funded in the early years. We viewed this as maximizing our wealth and minimizing taxes for the family as a whole.

And that’s exactly the thrust of the FP article, which cites several experts who will be familiar to most readers of the Hub: Aaron Hector of Doherty & Bryant Financial Strategies, Matthew Ardrey of TriDelta Financial, Adrian Mastracci of Lycos Asset Management. Mastracci created the chart below that appeared in the FP story:

There was also valuable input from BMO Private Wealth’s Sylvain Brisebois, who created a spreadsheet to estimate the impact of missing contributions in early years. If you can’t start until 25, a six per cent return generates $1,049,000 by age 65, $600,000 less than the $1.63 million earned with the extra $42,000 you’d have saved and compounded starting at 18. Another scenario is contributing for seven years between 18 and 25, then using it to buy a home. Assuming no more contributions the next 10 years and resuming $6,000 contributions at 36, by age 65 you’d have $829,000. Brisebois also created a scenario where you only contribute $3,000 a year, which generates $815,000.

As we experienced in our family, a long time horizon favours Millennials, who can afford to take a little more risk in return for stronger returns. That in turn translates into either a bigger nest egg 40 to 45 years from now, or it means you can get to the magic $1 million mark 5 or even 10 years ahead of schedule. Of course, if you’re even younger than a Millennial (technically they must be age 24 in 2020 to qualify) so much the better, and all these principles apply equally to Generations X, Y or Z.

For that matter, as I have often written, TFSAs are equally attractive for those already in Retirement. Unlike RRSPs, you can keep contributing to your TFSA long into old age: I had a friend who proudly told me she was still contributing after she turned 100!

Mind you, after the Coronavirus fears of the past week, who can really say? Not so good for aging Baby Boomers and retirees but of course if you’re a Millennial any young person with multi-decade time horizons, it should be viewed as good news when stocks go on sale.

The federal government kept the annual TFSA contribution limit at $6,000 for 2020 – the same annual TFSA limit that we had in 2019. It’s good news for Canadian savers and investors, who as of January 1, 2020, have a cumulative lifetime TFSA contribution limit of $69,500.

The Tax Free Savings Account (TFSA) was introduced in 2009 by the federal conservative government. The TFSA limit started at $5,000 that year: an amount that “will be indexed to inflation and rounded to the nearest $500.”

TFSA Contribution Limit Since 2009

The table below shows the year-by-year historical TFSA contribution limits since 2009.

Year

TFSA Contribution Limit

2020

$6,000

2019

$6,000

2018

$5,500

2017

$5,500

2016

$5,500

2015

$10,000

2014

$5,500

2013

$5,500

2012

$5,000

2011

$5,000

2010

$5,000

2009

$5,000

Total

$69,500

Note that the maximum lifetime TFSA limit of $69,500 applies only to those who were 18 or older on January 1, 2009. If you were born after 1991 then your lifetime TFSA contribution limit begins the year you turned 18.

You can find your TFSA contribution room information online at CRA My Account, or by calling Tax Information Phone Service (TIPS) at 1-800-267-6999.

TFSA Overview

The Tax Free Savings Account is a flexible vehicle for Canadians to save for a variety of goals. You can contribute every year as long as you’re 18 or older and have a valid social insurance number.

That means young savers can use their TFSA contribution room to establish an emergency fund or save for a down payment on a home. Long-term investors can use their TFSA to invest in ETFs, stocks, or mutual funds and save for the future. Retirees can continue to save inside their TFSA for future consumption or withdraw from their TFSA tax-free without impacting their Old Age Security or GIS.

Unlike an RRSP, any amount contributed to your TFSA is not tax deductible and so it does not reduce your net income for tax purposes.

You can contribute room is capped at your TFSA limit. Excess contributions will be taxed at 1 per cent per month

Any withdrawals will be added back to your TFSA contribution room at the start of the next calendar year

You can replace the amount of your withdrawal in the same year only if you have available TFSA contribution room

Any income earned in the account, such as interest, dividends, or capital gains is tax-free upon withdrawal

How to Open a TFSA

Any Canadian 18 or older can open a TFSA. You are allowed to have more than one TFSA account open at any given time, but the total amount you contribute to all of your TFSA accounts cannot exceed your available TFSA contribution room.

To open a TFSA you can contact any bank, credit union, insurance company, trust company or robo-advisor and provide that issuer with your social insurance number and date of birth.

The most common type of TFSA offered is a deposit account such as a high interest savings account or a GIC.

You can also open a self-directed TFSA account where you can build and manage your own savings and investments.

Qualified TFSA Investments

That’s right: you’re not just limited to savings accounts and GICs. Generally, you can put the same investments in your TFSA as you can inside your RRSP. These types of allowable investments include:

Cash

GICs

Mutual funds

Stocks

Exchange-Traded Funds (ETFs)

Bonds

You can contribute foreign currency such as USD to your TFSA. Note that your issuer will convert the funds to Canadian dollars. The total amount of your contribution, in Canadian dollars, cannot exceed your TFSA contribution room.

If you receive dividend income from a foreign country inside your TFSA, the dividend income could be subject to foreign withholding tax.

Gains inside your TFSA

Some investors may be tempted to put risky assets inside their TFSA account to try and earn tax-free capital gains. There are two advantages to this strategy:

Earn tax-free capital gains

Potentially increase your available TFSA contribution room Continue Reading…

As it stands today the Tax Free Savings Account or TFSA is true to its name. It is tax free on all counts. The interest or income or capital gains created in the account are not taxed. When you take money out of your TFSA you pay no tax. Net, net, your money grows tax free and you can spend it tax free.

But will this change in the future when Canadians have amassed considerable sums and are able to generate significant tax free income in retirement? Will the CRA eventually tax your Tax Free Savings Account? The TFSA program was launched in 2009 with a maximum of $5000 of contribution space. The contribution allowance has been increased to reflect inflation and now sits at $6000 annual.

In 2019 it’s not uncommon to see a Canadian who has maximized their TFSA contributions and who has invested their monies sitting with a six figure balance. In fact they might even approach a balance of $110,000 or more in a TFSA. For a Canadian couple that is $200,000 or more in potential tax free income.

In another 10 years that couple could easily have a combined $500,000 in TFSA monies. Of course they’ll need the cooperation of the stock markets that have been more than generous over the last 10 years, especially if you throw that roaring US stock market into the mix.

A massive TFSA gives Canadian retirees options

When Canadian retirees begin to accumulate sizable TFSA accounts they can start to execute some very opportunistic retirement strategies. And that might include accessing the government program known as the GIS or Guaranteed Income Supplement. That’s designed to help lower income seniors.

In a guest post on Cut The Crap Investing Financial Planner Graeme Hughes outlined how spending our own RRSP monies can negate potential GIS payments and that is one of the most common mistakes made by Canadian retirees. From that post …

What’s less well-known is the impact RRSPs can have on lower-income seniors, particularly those retiring with only the Canada Pension Plan (CPP) and Old Age Security (OAS) amounts for pensions. In many cases these seniors would also get the Guaranteed Income Supplement (GIS), which is an add-on benefit to the OAS. However, the GIS is an income-tested benefit and RRSP withdrawals absolutely count as income for this purpose.

So often I have seen seniors withdrawing from their modest RRSPs in retirement while not realizing that, had they not been making those withdrawals, they would have been receiving valuable GIS benefits rather than drawing down retirement savings. By better allocating their resources prior to retirement they could have greatly improved their overall retirement picture.

And that seems like fair and needed financial planning for those with modest RRSPs. That’s all within the spirit of the OAS and the GIS program that is designed for retirees with lower incomes. But Graeme goes on to outline that some retirees with greater assets can also take advantage of the GIS program by using their TFSA accounts.

Even for wealthier retirees with substantial savings but no employer pensions, it is possible to obtain 7 years of GIS benefits by drawing down TFSAs or savings between age 65 and 71 and letting the RRSPs grow until mandatory withdrawals start at age 72. Those benefits can be worth tens of thousands of dollars and should absolutely be taken into consideration when planning for retirement.

TFSA withdrawals do not show up on your tax filing as income. The CRA only keeps track of your TFSA contributions and withdrawals. And certainly make sure you understand how the program works so that you can avoid any over contribution penalties. Here’s a link to the TFSA essentials on the CRA site.

Given that, a retiree could take out $20,000 for spending from TFSA ($40,000 for a couple) and those monies do not count as income. Those retirees only source of reportable income might be CPP and OAS payments – they might qualify for GIS or reduced GIS. But these retirees are certainly lower income seniors. They may have an owned-home worth $1 million or more, each with RRSPs in the $500,000 range (or more), those six figure TFSAs and perhaps some taxable investment accounts throwing off tax efficient dividend income that qualifies for the Canadian dividend tax credit. They might have a modest amount in a savings account that is earning very little and not greatly affecting their income statement.

These retirees might have a net worth of $2,000,000 or more and yet they still qualify for that Guaranteed Income Supplement. When that occurs, it’s totally legal and within the current rules, but it’s certainly not within the spirit of the GIS program designed to help lower income seniors.

Will most Canadians be outraged?

I’m guessing that most Canadians will be up in arms when they hear or read of this opportunistic financial planning. Jonathan Chevreau asked the question on Twitter and it generated a vigorous debate. Well that is, readers were already taking issue with the potential use of GIS for those with considerable assets. Continue Reading…

Jennifer Diplock is Associate Vice-president, Personal Savings and Investing, TD Bank Group, based in Toronto.

Jennifer Diplock is Associate Vice-president, Personal Savings and Investing, TD Bank Group, based in Toronto.