By Michelle Arios

By Michelle Arios

Special to the Financial Independence Hub

There are a lot of life situations that can lead someone to retire much earlier than they had initially anticipated. It could be illness, injury, the need to move quickly, an emergency family circumstance, or even a company closing its doors. Why you’re being forced to retire isn’t nearly as important as the silver lining you need to find in your situation, and what steps you’ll take to get there.

1.) Get a great Savings plan

Your normal savings account may not be enough to carry you through. It might help to change your current savings account to one that gives you a better interest rate, particularly if you’re going to consolidate your retirement accounts. It might also help to supplement your savings with some investments that will grow with time.

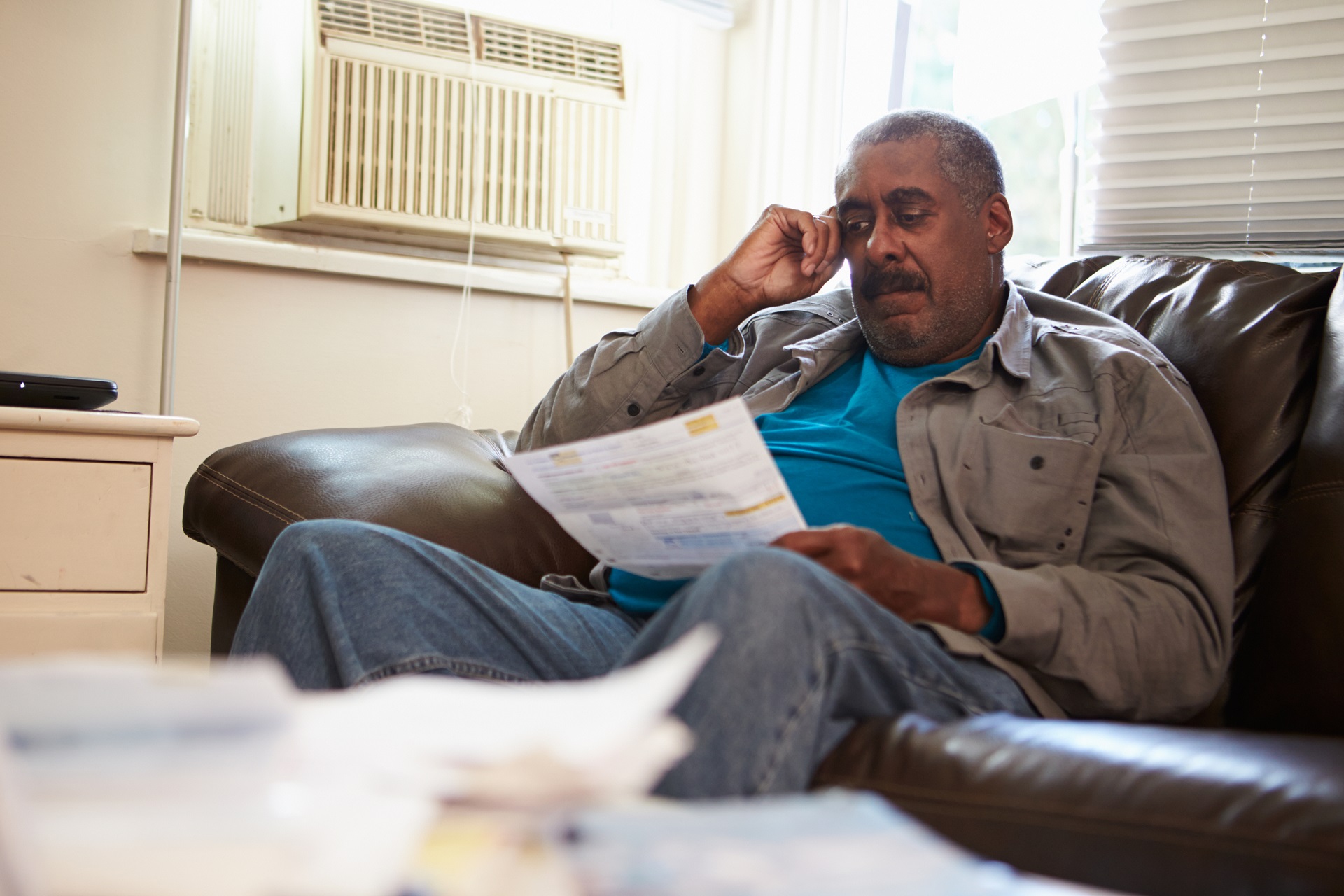

2.) Work out your new Budget

People in retirement often live on fixed incomes, especially if their spouse is also retired. You need to be sure your money can go as far as you need it to, and that might mean breaking apart your old budget and determining where and how you can best reduce costs while maintaining your quality of life. There are some easy-to-use smartphone apps that might help you do that.

3.) Downsize your Home

The expenses of maintaining a household are high. If you’re retired, you probably don’t need all the extra space anyway. Finding a roommate can help, and so can selling your previous home to purchase a smaller home that’s easier to maintain. Often times, utility bills will significantly go down on a smaller property. You’re also gaining some extra cash and a little more financial longevity.

4.) Find affordable alternatives

Monthly costs, like health insurance and cellular phone bills, can often add up to a lot of money. You might want to consider shopping around for a better deal. Continue Reading…